Back when I was an impressionable college student I was shown an asset allocation rubric. The rubric was a list of asset classes with a recommended percent of funds to be invested in each asset type. The result would be a diversified portfolio.

It was my first exposure to asset allocation and it made a lot of sense.

The allocation I was presented was very similar what I have listed below and I’ll call it “Portfolio 1”.

Asset Allocation Portfolio 1

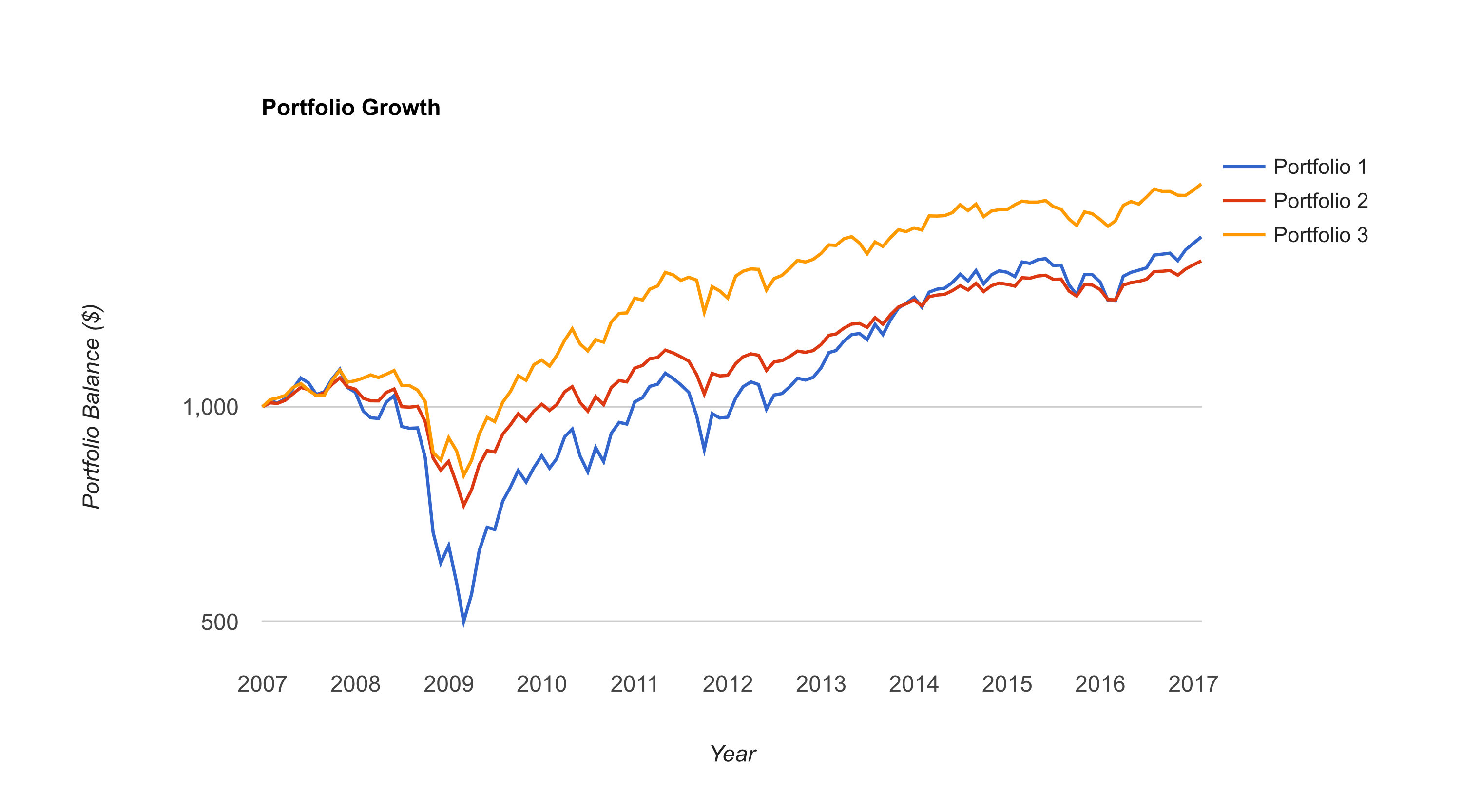

The problem with this portfolio is that is dropped over 55% in the 2008 financial crisis.

Without any bonds (or gold) this portfolio was subject to a massive drawdown.

Since January of 2007 to January of 2017 this portfolio has a compound annual growth rate (CAGR) of just 5.58%.

Plus the correlation with US stocks is .98.

In fact an investor would have been better off just buying the Vanguard Total Stock Market Index (VTSMX) and calling it a day. The “Just Buy VTSMX” strategy would have had a 7.25% CAGR with a lower maximum drawdown of around 50%.

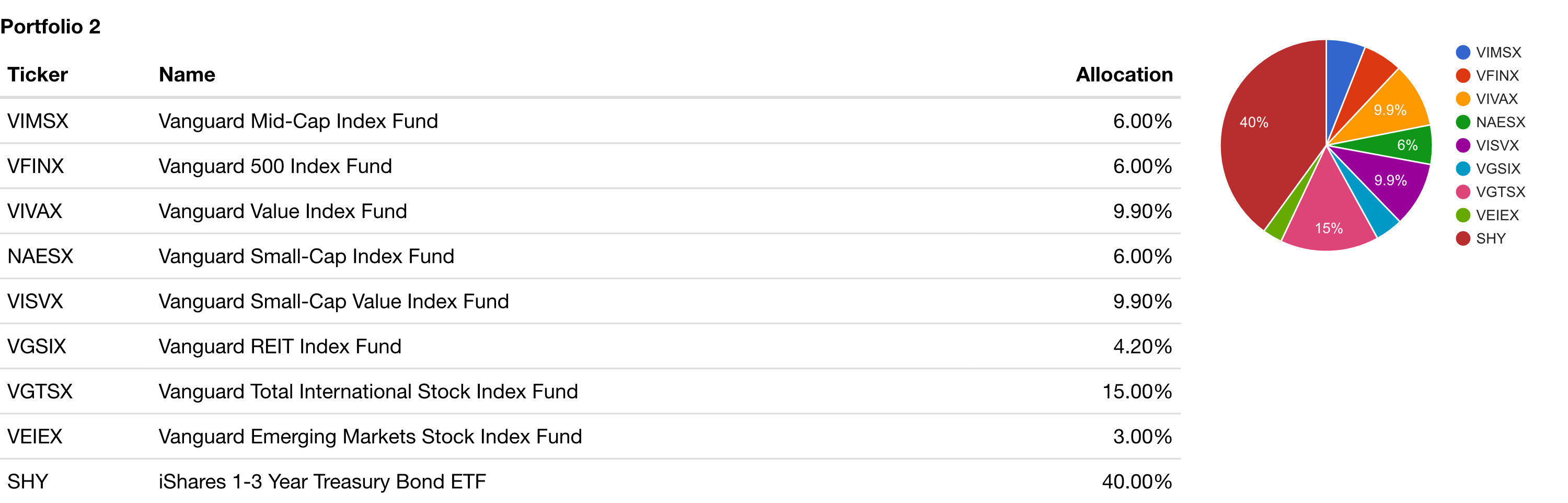

Asset Allocation: Portfolio 2 (Add Bonds)

To be fair, the allocation actually calls for a 40% allocation to short term bonds. Adding 40% bonds would have limited the maximum drawdown to a much more manageable 33.72% with a CAGR of 4.77%.

Correlation of this portfolio is still .98.

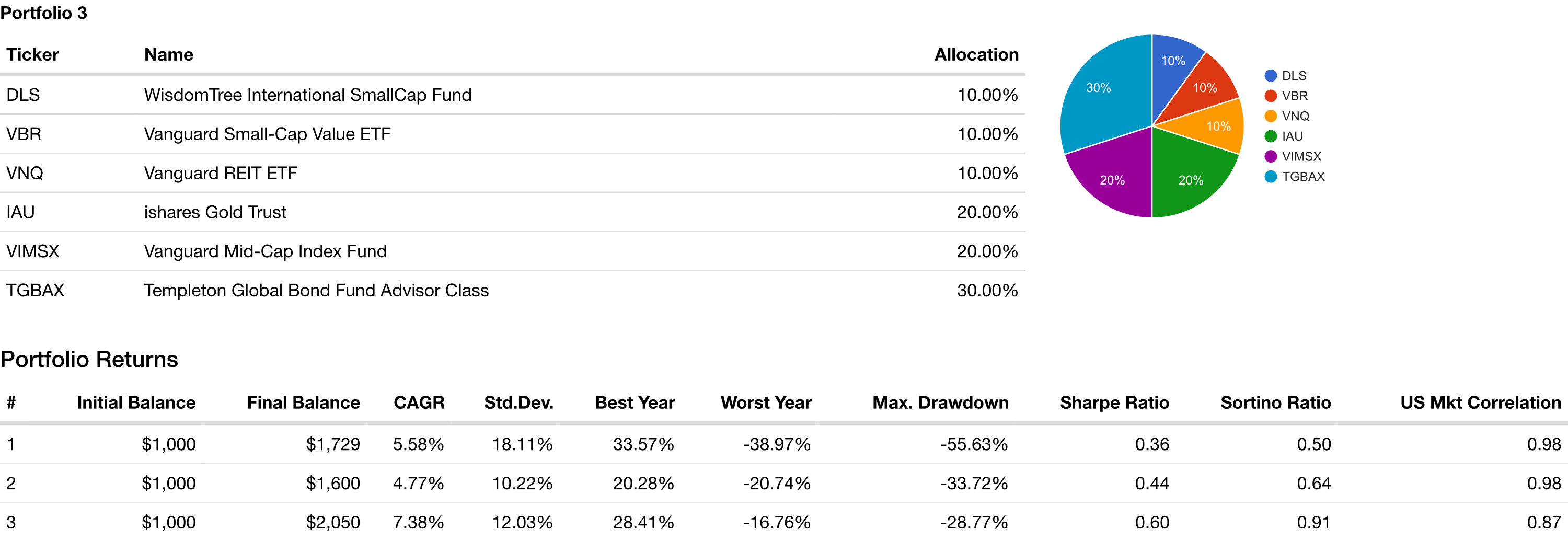

HIGMW Asset Allocation

But enduring a 33% drawdown for a a 4.77% return doesn’t seem stellar to me. So I’m been experimenting with different asset allocations using portfoliovisualizer.com.

The HIGMW Asset Allocation I’ve developed would have a maximum drawdown of 28.77% with a CAGR of 7.38%. Correlation with US stocks drops below the 90s down to .87, still high, but at least lower.

Now the actual investments in my allocation are listed below. I had to swap out some funds in order to get a sense of how this allocation would have performed in 2008.

However, many of the funds I like did not exist in 2008.

Yes, this allocation is 30% bonds. And yes, I think US stocks and bonds are in a bubble. And yes indeed I Don’t Own US Treasuries. But 20% of my allocation to bonds are outside the US and the other 10% are in a fund managed by Bill Gross mainly consisting of corporate bonds and only 6% in government bonds.

So my 30% allocation to these bond funds in no way contradicts my views on US debt.

I also allocated 20% to gold and 10% to real estate. I think if inflation does pick up (even more) these hard assets will add some resilience to the portfolio.

Small cap value stocks have outperformed over the last 45 year so I’m overweight small cap value. 10% is allocated to international small cap value stocks and 10% to small cap value stocks in the US. The 20% allocation to the First Trust Dorsey Wright Dynamic Focus 5 ETF is an interesting ETF in that it is somewhat trend following. Combine these three funds and 40% of this allocation is to stocks.

Gold doesn’t pay a dividend or yield. But until the central banks around the world stop acting like crazy people gold will remain a large part of my portfolio.

I don’t think I can be convinced that governments can continue to borrow, print and spend money without consequences.

Peter Schiff is Chief Economist & Global Strategist at EuroPacific Capital. He is also chairman of a gold reselling company. He appears on RT and has authored several books about the collapse of the dollar. Peter is a vocal critic of the US Federal Reserve and warned loudly about the housing bubble prior to the 2008-2009 financial crisis.

I owe much of what I know about the Federal Reserve to Peter Schiff. I’ve read some of his books and used to listen to his podcast.

But I’ve come to realize that Peter Schiff is not someone you want to listen to for financial or investment advise. The following are some key areas where I think he goes wrong.

His EuroPacific Funds are Expensive and Underperform

I invested some money with his firm, EuroPacific Capital between December 2014 and December 2020.

During that 6 year timeframe, my investments with EuroPacific Capital went up 20.5% (about a 3.8% annualized return) which doesn’t sound too bad until you consider the S&P 500 doubled in price during that same timeframe and provided an annualized return of nearly 15%.

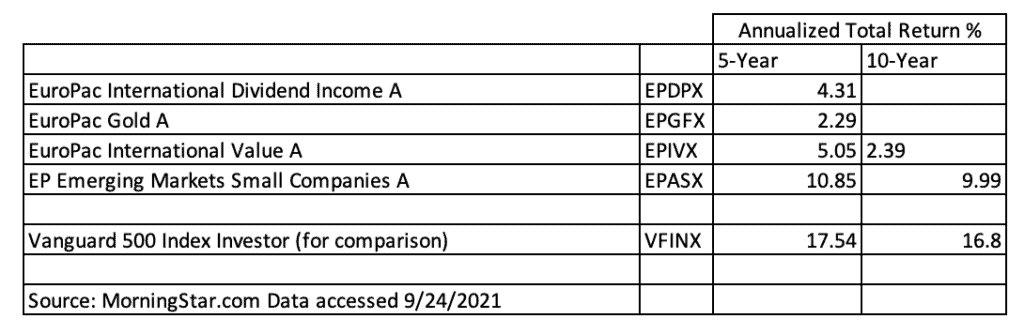

Peter’s firm EuroPacific Capital, charges what I consider to be high load fees and they underperform. For someone who preached about inflation, you’d think he’d make sure his funds at least beat inflation. They don’t. Looking up his funds on MorningStar, you can see the poor 5 and 10 year returns.

The EuroPac gold fund has a 5-year annualized total return of 2.29%. Inflation has been well over that for the past five years.

His Bias for Gold and Silver Blinds Him

Some might consider me a gold bug. I believe gold and silver are an important part of a diversified portfolio. But with Peter being a gold salesman, he is overly biased towards gold, this has caused Peter to miss out on an emerging asset class (cryptocurrencies) that while more volatile, has far outperformed gold. He has unsuccessfully predicted many tops to this asset class.

Not only that, but he’s failed to predict where all the Fed money printing would go. It’s gone into real estate, stocks, cryptocurrencies. It hasn’t gone into gold, silver and foreign stocks the way he has been predicting.

He Can’t Time the Dollar Crash

Peter Schiff is the boy who cried wolf.

Sometimes there is a “wolf” and when there is, it’s is important to let other people know there is a wolf so we don’t all get eaten.

Peter did correctly cry “wolf” before the 2008-2009 “wolf” reared its head. But he’s been wrong ever since.

Peter is a big fan of extended metaphors. So here is one for him. Peter is the boy who cried wolf, no one believed him and it turned out there was a wolf and he was right. Then he cried wolf again over and over again for the next 12 years as if the wolf was just behind the bushes, even though the wolf was 500 miles away.

His rhetoric that the dollar crash is imminent might be an effective sales tactic in the short term, but he has been wrong since the 2008-2009 financial crisis. It weakens his message and erodes his credibility to the point that I don’t listen to him anymore.

He has not been able to time when the dollar will crash. I agree the US Federal Reserve is reckless, is a prime cause of market crashes and price inflation. There is no question the dollar will continue to lose value. But will it happen all at once in a huge crash, or will it continue to decline 2-6% per year like it has for over the past 100 years? I don’t know and Peter Schiff certainly doesn’t know.

He has had no ability to predict how long the powers that be (the big banks, the military industrial complex, the Federal Reserve, the US government) can keep the dollar charade going. He will talk and write about how “The Dollar Will Implode When The Markets Figure X Out” but the market consists of a lot of people who stand to benefit from the charade continuing.

If you listen to Peter you will probably be correct eventually, after all, reserve currencies don’t last forever, but you might not benefit from it in your lifetime. Or you might.

What Can you Learn from Peter Schiff?

I certainly wouldn’t bet the farm on the US maintaining its reserve currency status for the next thirty years. I will remain thankful to Peter for opening eyes to some very real risks the US and the dollar face. But I will never be happy that I missed out on a 100% return if I hadn’t been invested with his firm from 2014-2020. He is not the person I will be going to to figure out how to grow and protect my wealth.

The answer is to take a more diversified approach and to keep your costs down. You can own foreign stocks through a low cost Vanguard mutual fund. Most large non-US companies are listed on US exchanges anyway. Most US companies have large foreign components for their business. When you invest in large US stocks, you are also investing in their non-US sales.

I think owning 5-10% of your liquid net worth in gold and silver is important. I think if you have some extra money to speculate on with cryptocurrencies that could also result in some outsized returns. I think owning hard assets like real estate and yes even some gold and silver is important.

But thinking there is some impending dollar collapse looming on the corner doesn’t do any good. It certainly hasn’t for the past 12 years.

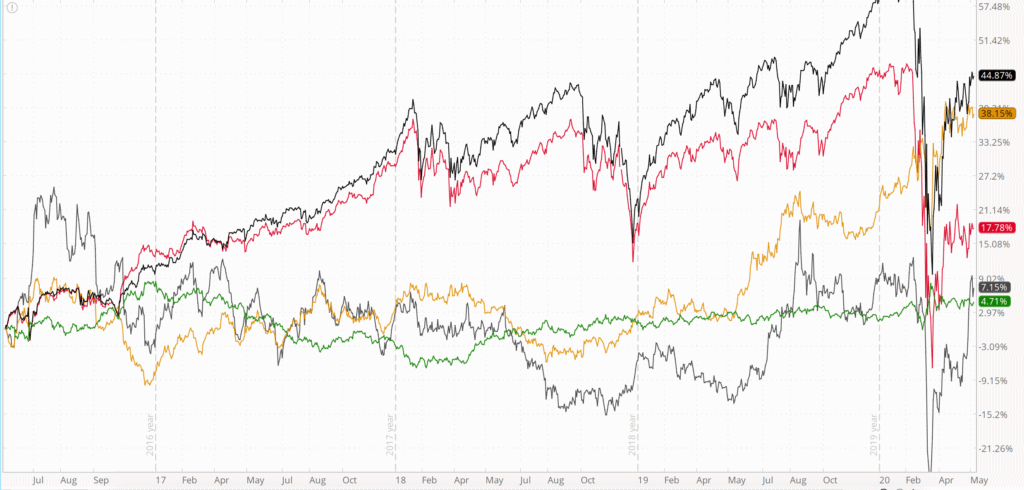

Just about four years ago I wrote the first article on HowIGrowMyWealth.com “Inflation Destroys Dollars“. I wrote about how what I do to protect against price inflation and dollar devaluation. Specifically value investing and precious metals. So in retrospect, how did those investments do?

As a control we’ll add the U.S. Dollar Index ($DXY, shown in green), which compares the dollar’s strength against a basket of other currencies. To represents “stocks” I’d added the S&P 500 Index (SPX) (shown in black).

I’m using the Vanguard Large Cap Value ETF (VTV) as a proxy for value stocks (shown in red). You can see how my current and past individual value stock picks have done here. Gold futures are in yellow and silver futures in gray.

As you can see the S&P 500 has been the place to be. To be fair gold isn’t too far behind. Gold was in fact keeping pace with and surpassing S&P 500 this past April. So while gold has been a good hedge and having exposure to stocks has continue to be important.

Value stocks have lagged the S&P 500, particularly in the aftermath of the December 2018 selloff.

Silver is only slightly outpacing the dollar index, up just 7.15%. Silver has had a few failed breakout attempts, but continues to underperform. The gold/silver ratio that some precious metal bugs talk about would suggest that silver is a better value right now.

Costs continue to rise each year as the dollar loses value. But as measured by the DXY the dollar has kept its value against other currencies.

As I wrote back in November of 2016 in “I Own Too Much Gold“, you don’t want to own too much gold as a percentage of your net worth. The performance of the S&P 500 is a good reason why. If gold ever were to take off a 10-25% allocation would be more than sufficient.

We certainly haven’t see broad hyperinflation yet in the US, but my rent, food and medical costs continue to rise each year in excess of the government measured CPI. As I have for the past four years, gold and precious metals remains an important (albeit minority) portion of one’s portfolio.

If you are just starting to buy precious metals emphasizing silver over gold (while still buying both) could be a good approach.

Real Estate is a great investment for a variety of reasons including the tremendous tax benefits. However, you might not want to be a landlord or you’re just looking for alternative investments to real estate. Below are Five Alternative Investments to Real Estate.

5. Fixed Income Investments

Fixed income investments include bonds and certificates of deposit (CDs). Bonds can be further broken down into categories: governmental and corporate. Fixed income investments are called fixed, because you know exactly the amount of income they will produce.

The rate is fixed.

For example, you might buy a corporate bond with a $1,000 face value with a 5% yield that matures in five years.

You’d get paid $50 per year and then at the end of five years you’d also be paid back the $1,000 initial investment. Governmental bonds work the same way.

Advantages to Fixed Income Investments

Consistent income–you know exactly how much income you will receive and when you’ll receive it.

Bonds and CDs, in general, are also considered very low risk.

A person who owns bonds for a company in bankruptcy will be able to get a “piece of the pie”, if there is any pie left over, after secured creditors but before some other investors, such as stockholders.

Disadvantages to Fixed Income Investments

Fixed income investments tend to have a much lower return when compared with riskier assets.

CDs do not allow you access to your money for a fixed amount of time (less than five years) without paying a penalty

While bonds are generally considered low risk, specific bonds are rated based on their likelihood of being repaid, with AAA rated bonds being those most likely to be repaid.

Of course if you buy the bonds of a company or country that is insolvent or on the verge of bankruptcy, you could still lose all your money.

Bonds are subject to interest rate risk if, for example you purchase a bond fund, rather than a bond you don’t hold to maturity. If bond rates go up, the yield on the bond you own could be lower than what is currently available. As a result, others will not buy the bond from you except at a discount, this will force you to either hold your bond to maturity or potentially sell the bond at a loss.

Fixed income investments are subject to inflation risk. If the value of the currency you are being paid in decreases, even if there is no nominal loss, you may lose significant purchasing power.

Ways to Make Fixed Income Investments

You can purchase US government bonds directly via treasurydirect.gov. Invest in a CD at your local bank or credit union. You can purchase bond funds, either private government or both via ETFs (exchange traded funds) or mutual funds. You can even buy bonds from foreign countries. Fixed income investments are just one group of alternative investments to real estate.

In addition to peer to peer lending, stocks, mutual funds, CD’s, commodities, and cryptocurrencies and other alternative investments to real estate, there is the real estate investment trust or REIT. REITs aren’t an alternative investment to real estate, but an alternative way to invest in real estate.

4. Stocks

The price of the stock (or ETF or Mutual Fund) can go up if people are willing to pay a higher price. Stocks can also pay dividends, in which holders of the stock given a portion of the companies proceeds. These dividends can either be reinvested in the company or kept, or invested in other companies.

Advantages to Investing in Stocks

Stocks tend to produce higher long term returns than do fixed income investments. Stocks will tend to do better than fixed income investments during periods of high inflation.

Disadvantages to Investing in Stocks

Stocks tend go up and down in price with more volatility than fixed income investments. A company could go bankrupt and the shareholders could lose all of their investment. If the price of a stock goes down, it may never recover in price. Buying a stock for its dividend, the company could decide to cancel the dividend, you would of course keep any dividends paid out, but not receive future dividends.

Not all companies are able to produce a profit and stay in business and if the company you own stock in files for bankruptcy stockholders are the last in line to receive any of the remaining assets of the company.

Stocks are also subject to interest rate risk, if interest rates rise, that tends to put negative pressure on the price of stocks.

How to Invest in Stocks

You can open a brokerage account at a variety of companies. I like Vanguard.com where they are known for their very low cost mutual funds.

If your employer offers a 401(k) you can invest in stocks through that program, although you will likely be limited to a small number of mutual funds.

3. Peer to Peer Lending

With technology, people don’t need to go to a bank or their rich uncle to get a loan. There is the relatively recent phenomena in which individuals lend (more) directly to other individuals via Peer to Peer (P2P) lending.

These loans made to small businesses, individuals wanting to pay off student loans, credit card consolidation, or any number of purposes. This can be considered a sub-type of fixed income investing, but it merits its own category because fo the types of loans this opens up.

Advantages to Investing in Peer to Peer Lending

You can learn more directly how the money will be used. You have more control over what kind of activity you are supporting than if you lend money to the government or a corporation.

The returns of P2P lending can be higher than other fixed income type investments. For example as of May 2019 some debt consolidation loans made to AA borrowers yield upwards of 7% for a 3 year term. A 3-year United States treasury bond, by comparison, only yields about 2.3%.

Of course the US government is considered a rock-solid borrower, so the 4.7% premium of the prosper lender reflects the fact that they are less likely to repay the loan.

The minimums tend to be lower. Some P2P marketplaces allow you to invest as little as $25. If you’re mistrustful of banks or the government you might find cutting them out of the equation desirable.

Disadvantages to Investing in Peer to Peer Lending

The loans you make could be riskier than other types of investments. If you make an un-collateralized loan to someone with a low credit score, you might not get repaid. If you decide to make a loan, but want your money back before the loan is scheduled to be repaid, there might not be another buyer who wants to purchase the loan from you or there might only be buyers who will purchase it from you at a lower price.

There is also interest rate risk just like other fixed income investments. Because you are investing in individuals, if the economy tanks and joblessness increases, the chances of being repaid are less, as compared to a governmental or corporate loan, where they tend to have more resiliency.

I think there is also some regulatory risk with P2P lending. Although they seem faired entrenched now, regulatory agencies could crack down on them in the name of “safety” or “terrorism”. When in reality it is just to force borrowers back to banks.

How to Invest via Peer to Peer Lending

There are a variety of P2P lending sites, such as prosper.com and upstart. I’ve personally used prosper.com and it works fine, but I don’t have other P2P sites with which to compare.

2. Precious Metals

Technically one does not “invest” in commodities because the purchase of gold, silver, or palladium doesn’t pay a dividend or yield (same can be said of many stocks). However, I think it is an overlooked asset class, and this is my website so I get to make up the rules.

The government of the United States is highly indebted, many huge programs such as social security and medicare are underfunded. Debt amongst individuals is high, as well as debt in States like Illinois and California. Pensions are also underfunded.

Governments invariably try to increase taxes to pay for these programs, but that won’t work. The next option will be to monetize the debt, that is create the money out of thin air and use it to bail out these programs. The results will be a reduction in the purchasing power of the dollar. Gold and Silver are a hedge for when this happens.

Advantages to buying Precious Metals

Stocks and bonds are highly correlated. Precious metals are less correlated to the stock market. You also have less to worry about in terms of bail-ins. There is no counter-party risk to physical precious metals in your possession.

Companies and currencies come and go. Gold has been valued for thousands of years and there is no reason to believe that will change.

Disadvantages to buying Precious Metals

In the Unite States at least, if your PMs go up in price and you sell, are subject to taxes, and they are taxed not at the lower capital gains rate, but as income.

There are no earnings or dividends when it comes to precious metals.

If you own physical bullion it could get lost or stolen. The United States government has in the past violated its own constitution and confiscated gold and could do so again.

How to buy Precious Metals

You can buy gold and silver through ETFs and mutuals funds. I don’t recommend this. You can also buy physical gold and silver bullion, or bullion grade jewelry. If you do buy physical gold or silver, it is important to keep it in a secure location.

Your content goes here. Edit or remove this text inline or in the module Content settings. You can also style every aspect of this content in the module Design settings and even apply custom CSS to this text in the module Advanced settings.

Over the past few weeks I’ve been writing about the faulty wiring in the United States economy that will eventually result in an Economic Conflagration.

The faulty wiring that will ultimately lead to this economic firestorm includes the fact that the real economy is weak, the economy is crushed by profligate debt and that stocks are overpriced and due for a significant crash.

One of the reasons why candidates such as Bernie Sanders and Donald Trump were popular in the last United States presidential primary and general election is because people know that the real economy is weak. They know how much debt they have and they want someone to make radical changes and do something about it.

Unfortunately government has never been particularly good at creating wealth or prosperity.

Some people might choose to rely on politicians to fix things. This website is not for those people. HowIGrowMyWealth.com is for people who want to take some common sense steps to grow and protect their wealth.

Given the faulty wiring the economy it is more important than ever to grow and protect one’s wealth. It might take a while but this faulty wiring will eventually result in a fire that will burn uncontrollably.

I realize this isn’t necessarily very cheery stuff but fear not! There is plenty of room for optimism.

I’m not a doomsday “prepper” or perma-bear and I’m sure that entrepreneurs, if free to do so, will rebuild the economy and usher in greater prosperity that will not be funneled to the politically connected.

I’m also cognizant that the stock market has gone up nearly 300% since the great recession, there hasn’t been hyperinflation in consumer prices and on the surface the crisis seems to have passed long ago. I don’t have a crystal ball and being right early sometimes looks like being wrong.

Despite the relative calm there is faulty wiring in the economy and sooner or later it will spark and ignite blaze that will, to quote Peter Schiff, “will make the financial crisis of 2008 look like a Sunday school picnic.”

The politicians, if they even realize that there are systemic problems in the economy, simply aren’t willing to endure the short term pain and inconvenience of ripping out the faulty wiring in order to fix the underlying problems. So they will continue to kick the can until the economic house burns down.

The bright side is that this will present an opportunity to rebuild the economy based on a strong foundation as opposed to what we have now, a phony economy based on debt, cheap money and consumption.

There will be winner and losers. I’m very optimistic about the future and I want to be counted amongst the winners.

So where am I putting my money?

My asset allocation falls into three main areas. Value stocks, gold and cash.

Value Stocks

Most people love buying things on sale and getting a great deal, expect when it comes to investing. When it comes to investing people want to buy expensive things and hope they go higher. Value investing takes that same common sense, buying things when they’re on sale and applies it to stocks and other asset classes.

The stock market as a whole is overvalued by a variety of metrics. But there are still good deals out there especially in non-US markets. I don’t doubt that value stocks will also go down in the event of a stock market crash but I think they will go down less and they will recover with more strength.

I share my value stock picks publicly. But I only share if I would buy them today or if I would hold or add to my positions with members of my free email newsletter. I will also let me email subscribers know when I buy or sell a stock first, before I publish that information to this website.

Gold

I don’t think you will get rich buying gold but it could prevent you from getting poor. Under relatively normal circumstances the demand for gold is fairly steady and the supply is fairly steady so for the most part the price of gold will rise with the level of inflation.

Gold is a way to save purchasing power. It’s a way to opt out of the financial system and wait for sanity to return.

If the dollar tanks loses it’s reserve currency status gold will still be valued.

I also think there has been significant effort to suppress the price of gold and depending on how much downward price manipulation there really has been, the price of gold could go up significantly from where it is right now.

If fiat currencies collapse that could very well induce a flight to the safe haven asset of gold that this influx of demand would be very bullish for gold.

Because of the absurd expansion in central bank balance sheets and artificially low interest rates I like gold presents a fantastic value at current prices.

What I write about gold applies to silver–another asset I think will do very well in a downturn. Silver has the added benefit of being an industrial metal that is more widely consumed.

Cash

Long term, like every other fiat currency, I think the dollar will go to zero. So why would I want to hold dollars?

First, I own a month or two of expenses in physical cash in a secure location in case there are capital controls. If there is a panic and people start withdrawing money from the banks the banks might in turn say, you can only withdraw $500 a week or something like that. Withdrawal limits could also be imposed if the US implements negative interest rates and people (very rationally) decide it is better to hold dollars in physical cash so they don’t have to pay interest to their bank for the privilege of loaning their money to the bank.

I reside in the United States and everything is priced in dollars so I need dollars to buy things. If I lived in the eurozone I would hold pounds or euros, if I lived in China I would hold Yuan. If I lived in the socialist paradise of Venezuela I would probably hold dollars (and try to get out).

Secondly, apart from physical cash I also hold dollars in a money market fund as a war chest. If stocks tank I expect there will be bargains to be had. I want to be buying stocks (if they are high quality free cashflow producing companies) when everyone is panicking and selling.

Now I fully expect the United States Federal Reserve to do what it has done in all other crises it has created–it will lower interest rates and buy assets to prop up the markets.

With interest rates already low once they cut rates to zero they will only be able to do things like Quantitative Easing and Negative rates. This is very bearish for the dollar and very bullish for gold.

But in the highly unlikely chance the US Federal Reserve does the right thing and lets the stock market collapse and lets the US government default on it’s debts this could be very bullish for the dollar. So holding some dollars is a hedge against deflation as well as a war chest to draw upon to buy undervalued stocks post crash.

What are some other possibilities?

While the bulk of my holdings are in cash, value stocks and precious metals I also dabble in some other alternative investments.

If there is a dollar crisis or collapse in the faith of central bankers then more people could turn to cryptocurrencies and could see it rise. Demand for cryptocurrencies could also rise for other reasons pushing the price upwards.

While I think blockchain technology is here to stay the value of any one specific cryptocurrency or token could very easily tank to nothing. Cryptocurrencies are very risky and 90% swings (both directions) happen.

You need to have an iron stomach but having between 1-5% of your liquid net work in cryptocurrencies isn’t the most outlandish idea in the world.

I would only speculate on cryptocurrencies with what you can afford to lose and I don’t considering buying cryptocurrencies investing in a technical sense since I am simply betting on the price going up.

I’ve shared with my readers my Group of Six cryptocurrencies that I’ve chosen to own and speculate on.

Options

Net I’ve actually lost money trading options. I traded options while unemployed and failed to remain dispassionate and objective. I was so focused on making money that I opened positions when the conditions were not ideal and took risks I should not have been taking.

I do believe if you are disciplined and follow the appropriate rules, you can do well trading options.

During a stock market crash volatility spikes and selling options could be a good strategy. When the VIX (a volatility index) spiked up in early February I sold a few options and those positions are doing well as volatility has dropped and the market has recovered. Markets don’t move straight up or down for very long so even if the February selloff portends drops to come, the market doesn’t drop as fast as people think in the midst of the drop.

Real Estate

Unlike all the other assets mentioned above I do not and never have owned any real estate.

Lots of people have made lots of money in real estate. I am working to learn more about this asset class and hope to own my own rental property at some point.

What I like about real estate is that it is easy to use leverage and the tax benefits are ridiculous. You can effectively pay no tax on investment property income and borrow a lot of the money you need to get started.

You of course need to know what you’re doing.

My goals for owning real estate involve owning a multi-family apartment building. The key for me is a cashflow positive property. I don’t have any interest in trying to buy and flip, although some people are very successful doing this. There are lots of ways to make money in real estate and I recommend biggerpockets.com to learn about them.

I think cashflow positive real estate will do okay in the event of a crash. If you’re in an area that has stable employment prospects those workers will always need a place to live and have the money to pay for it. Of course real estate won’t “always go up” and there are a lot of risks and headaches associated with managing property (if you don’t outsource property management).

This is part 5 of 5 of what I’ve decided to term The Economic Conflagration series where I discuss the faulty wiring pervasive the global economy:

Whatever vestigial link between US dollars and gold ended after Bretton Woods was terminated on 15 August 1971. The classic gold standard was abolished long before in 1933 when the despotic executive order of United States President Franklin D. Roosevelt that made it illegal for citizens in the land of the free to own gold.

There are periodic calls to return to a gold standard as a way to reign in government spending. The return to a pre-1933 gold standard would be a huge step in the right direction.

A true gold standard uses gold as money. A true gold standard in the US would redefine dollars as a quantity of gold. A true gold standard is NOT saying that gold is worth $35 per ounce as was the case in Bretton Woods.

This is explained in fantastic detail by Mises Institute Senior Fellow Joseph T. Salerno in his lecture Gold Standards: True and False.

A Return to the Gold Standard in the US?

It sounds click-baity to me too, but Jim Rickards is predicting $10,000 gold as the result of a currency reboot. The link above is to a sales page (which I get zero benefit from and considered not linking to) that explains in his own words why Rickards thinks Trump will return the US to a “gold standard”.

James G. Rickards is a New York Times bestselling author who appears on networks like RT, CNBC and Bloomberg. He’s testified in front of congress, he’s done some consulting on currency for the CIA and Pentagon. So there are some reasons to listen to what he says and at least evaluate his rationale and his arguments.

If I can quickly summarize his argument it’s that the US is deeply in debt, debt has crushed the middle class, a gold standard is one of the keys to “Making America Great Again” and so President Trump going to move the US back onto a gold standard. Rickards also claims he has some inside information that gives him additional reason to believe a return to such a gold standard is likely.

I agree the US is deeply in debt. I also agree the economy is broken and stacked against the middle class in favor of the super-wealthy. I also agree that a return to a classic gold standard similar to what existed pre-1933 would help America.

There is also some evidence that Trump is receptive to the gold standard.

Would Trump Support a Gold Standard?

Trump hasstated to GQ: “Bringing back the gold standard would be very hard to do, but boy would it be wonderful. We’d have a standard on which to base our money.” In the same montage of questions he also stated that Justin Bieber shouldn’t be deported and that he’s not a fan of Man Buns.

Trump has also tweeted this:

Remember the golden rule of negotiating: He who has the gold makes the rules.

As far as I can tell Donald Trump is not a systematic thinker. He doesn’t have a set of principles with which he evaluates problems and situations. I think Trump’s “philosophy” is basically “I’m a smart guy with good business sense. So I’m going to use my gut and my experience to make ad hoc judgments about what to do.”

Although he probably wouldn’t use the term ad hoc.

So could Trump be in favor of a gold standard? Who knows? Even if he was in some way at some point in the past who knows what he would decide today. Just look at his 180 turn on the war in Afghanistan as one example of his fickleness.

Where does Rickards get $10,000?

Rickards uses a fairly basic calculation based on what he thinks the world money supply will be, how much gold there is and a 40% backing to get $10,000 gold.

Rickards writes that the US government would keep the price at this level by simply conducting some “open market operations” in gold:

The Federal Reserve will be a gold buyer if the price hits $9,950 per ounce or less and a gold seller if the price hits $10,050 per ounce or higher

And this is really the rub. Such a price peg is not a return to a true gold standard. It would not change the US government’s fiat monetary system in any meaningful way.

Dollar to Gold Price Pegs are not a True Gold Standard

The plan Rickards describes is essentially the same as a bill that was proposed in 2013. Mises Institute fellow Joseph T. Salerno explains how such a fake gold standard would not help at all. A true gold standard defines dollars (or other currency) as a certain weight of gold. For example, the definition of a dollar used to be 1/20th of an ounce of gold (roughly). A $20 bill was not the money per se but a claim to one ounce of gold.

The “gold standard” Rickards speaks of is simply fixing the price of gold in dollars.

I Would Like Gold at $10,000

All else equal I would like gold at $10,000. Sure, if I wanted to add to my holdings it would be cost prohibitive, but since I already own some gold a price increase to $10,000 via Federal Reserve open market operations would be of benefit to me.

However, if the dollar collapsed and a loaf of bread costs $10,000 I’m probably not better off. After all no sane person would want to be a millionaire in Zimbabwean dollars in 2008.

This fake gold standard Rickards is predicting certainly wouldn’t help the US economy at large. As I mentioned above, it would not be any significant change to the fiat monetary system. A price peg of gold in terms of dollars is NOT a gold standard. If anything I think it would be horrible optics for the US government and shake the world’s confidence in the dollar. It would effectively be a revaluation down of the dollar, at least relative to gold, and the Fed’s balance would very likely have to massively expand in order to bid gold up to $10,000.

A Return to the Gold Standard Seems Unlikely

A return of the United States to a true gold standard seems very unlikely. A fake gold standard as described by Rickards is more likely than a return to a true gold standard–but still a long shot. I do believe gold is a fantastic long term investment but I also believe it will take the market waking up to the problems of the global financial system and not an act of government.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.