Peter Schiff is Chief Economist & Global Strategist at EuroPacific Capital. He is also chairman of a gold reselling company. He appears on RT and has authored several books about the collapse of the dollar. Peter is a vocal critic of the US Federal Reserve and warned loudly about the housing bubble prior to the 2008-2009 financial crisis.

I owe much of what I know about the Federal Reserve to Peter Schiff. I’ve read some of his books and used to listen to his podcast.

But I’ve come to realize that Peter Schiff is not someone you want to listen to for financial or investment advise. The following are some key areas where I think he goes wrong.

His EuroPacific Funds are Expensive and Underperform

I invested some money with his firm, EuroPacific Capital between December 2014 and December 2020.

During that 6 year timeframe, my investments with EuroPacific Capital went up 20.5% (about a 3.8% annualized return) which doesn’t sound too bad until you consider the S&P 500 doubled in price during that same timeframe and provided an annualized return of nearly 15%.

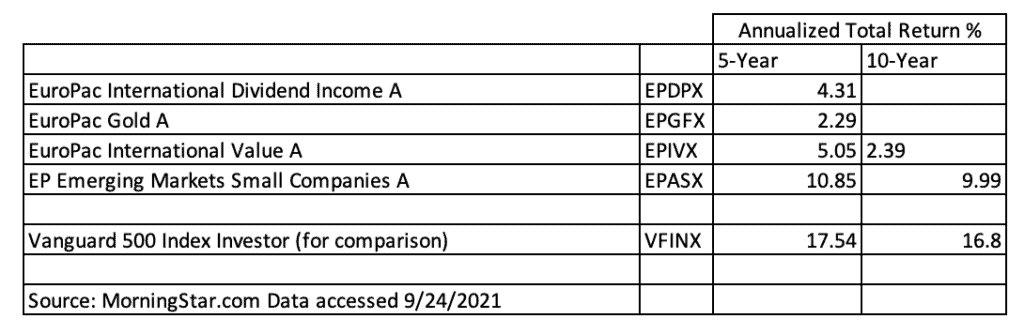

Peter’s firm EuroPacific Capital, charges what I consider to be high load fees and they underperform. For someone who preached about inflation, you’d think he’d make sure his funds at least beat inflation. They don’t. Looking up his funds on MorningStar, you can see the poor 5 and 10 year returns.

The EuroPac gold fund has a 5-year annualized total return of 2.29%. Inflation has been well over that for the past five years.

His Bias for Gold and Silver Blinds Him

Some might consider me a gold bug. I believe gold and silver are an important part of a diversified portfolio. But with Peter being a gold salesman, he is overly biased towards gold, this has caused Peter to miss out on an emerging asset class (cryptocurrencies) that while more volatile, has far outperformed gold. He has unsuccessfully predicted many tops to this asset class.

Not only that, but he’s failed to predict where all the Fed money printing would go. It’s gone into real estate, stocks, cryptocurrencies. It hasn’t gone into gold, silver and foreign stocks the way he has been predicting.

He Can’t Time the Dollar Crash

Peter Schiff is the boy who cried wolf.

Sometimes there is a “wolf” and when there is, it’s is important to let other people know there is a wolf so we don’t all get eaten.

Peter did correctly cry “wolf” before the 2008-2009 “wolf” reared its head. But he’s been wrong ever since.

Peter is a big fan of extended metaphors. So here is one for him. Peter is the boy who cried wolf, no one believed him and it turned out there was a wolf and he was right. Then he cried wolf again over and over again for the next 12 years as if the wolf was just behind the bushes, even though the wolf was 500 miles away.

His rhetoric that the dollar crash is imminent might be an effective sales tactic in the short term, but he has been wrong since the 2008-2009 financial crisis. It weakens his message and erodes his credibility to the point that I don’t listen to him anymore.

He has not been able to time when the dollar will crash. I agree the US Federal Reserve is reckless, is a prime cause of market crashes and price inflation. There is no question the dollar will continue to lose value. But will it happen all at once in a huge crash, or will it continue to decline 2-6% per year like it has for over the past 100 years? I don’t know and Peter Schiff certainly doesn’t know.

He has had no ability to predict how long the powers that be (the big banks, the military industrial complex, the Federal Reserve, the US government) can keep the dollar charade going. He will talk and write about how “The Dollar Will Implode When The Markets Figure X Out” but the market consists of a lot of people who stand to benefit from the charade continuing.

If you listen to Peter you will probably be correct eventually, after all, reserve currencies don’t last forever, but you might not benefit from it in your lifetime. Or you might.

What Can you Learn from Peter Schiff?

I certainly wouldn’t bet the farm on the US maintaining its reserve currency status for the next thirty years. I will remain thankful to Peter for opening eyes to some very real risks the US and the dollar face. But I will never be happy that I missed out on a 100% return if I hadn’t been invested with his firm from 2014-2020. He is not the person I will be going to to figure out how to grow and protect my wealth.

The answer is to take a more diversified approach and to keep your costs down. You can own foreign stocks through a low cost Vanguard mutual fund. Most large non-US companies are listed on US exchanges anyway. Most US companies have large foreign components for their business. When you invest in large US stocks, you are also investing in their non-US sales.

I think owning 5-10% of your liquid net worth in gold and silver is important. I think if you have some extra money to speculate on with cryptocurrencies that could also result in some outsized returns. I think owning hard assets like real estate and yes even some gold and silver is important.

But thinking there is some impending dollar collapse looming on the corner doesn’t do any good. It certainly hasn’t for the past 12 years.