Peter Schiff is Chief Economist & Global Strategist at EuroPacific Capital. He is also chairman of a gold reselling company. He appears on RT and has authored several books about the collapse of the dollar. Peter is a vocal critic of the US Federal Reserve and warned loudly about the housing bubble prior to the 2008-2009 financial crisis.

I owe much of what I know about the Federal Reserve to Peter Schiff. I’ve read some of his books and used to listen to his podcast.

But I’ve come to realize that Peter Schiff is not someone you want to listen to for financial or investment advise. The following are some key areas where I think he goes wrong.

His EuroPacific Funds are Expensive and Underperform

I invested some money with his firm, EuroPacific Capital between December 2014 and December 2020.

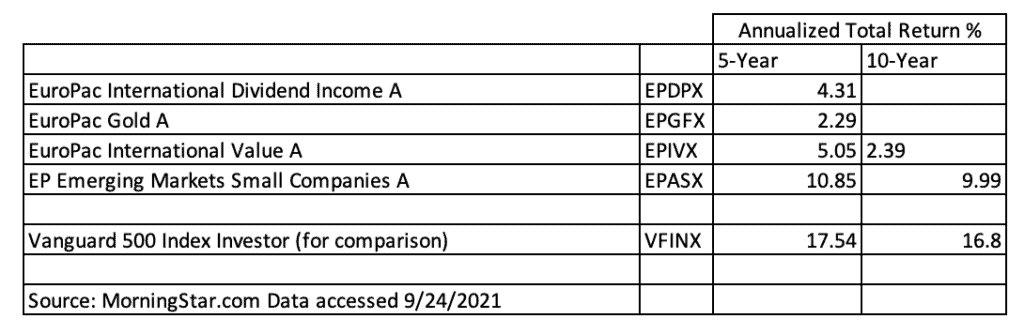

During that 6 year timeframe, my investments with EuroPacific Capital went up 20.5% (about a 3.8% annualized return) which doesn’t sound too bad until you consider the S&P 500 doubled in price during that same timeframe and provided an annualized return of nearly 15%.

Peter’s firm EuroPacific Capital, charges what I consider to be high load fees and they underperform. For someone who preached about inflation, you’d think he’d make sure his funds at least beat inflation. They don’t. Looking up his funds on MorningStar, you can see the poor 5 and 10 year returns.

The EuroPac gold fund has a 5-year annualized total return of 2.29%. Inflation has been well over that for the past five years.

His Bias for Gold and Silver Blinds Him

Some might consider me a gold bug. I believe gold and silver are an important part of a diversified portfolio. But with Peter being a gold salesman, he is overly biased towards gold, this has caused Peter to miss out on an emerging asset class (cryptocurrencies) that while more volatile, has far outperformed gold. He has unsuccessfully predicted many tops to this asset class.

Not only that, but he’s failed to predict where all the Fed money printing would go. It’s gone into real estate, stocks, cryptocurrencies. It hasn’t gone into gold, silver and foreign stocks the way he has been predicting.

He Can’t Time the Dollar Crash

Peter Schiff is the boy who cried wolf.

Sometimes there is a “wolf” and when there is, it’s is important to let other people know there is a wolf so we don’t all get eaten.

Peter did correctly cry “wolf” before the 2008-2009 “wolf” reared its head. But he’s been wrong ever since.

Peter is a big fan of extended metaphors. So here is one for him. Peter is the boy who cried wolf, no one believed him and it turned out there was a wolf and he was right. Then he cried wolf again over and over again for the next 12 years as if the wolf was just behind the bushes, even though the wolf was 500 miles away.

His rhetoric that the dollar crash is imminent might be an effective sales tactic in the short term, but he has been wrong since the 2008-2009 financial crisis. It weakens his message and erodes his credibility to the point that I don’t listen to him anymore.

He has not been able to time when the dollar will crash. I agree the US Federal Reserve is reckless, is a prime cause of market crashes and price inflation. There is no question the dollar will continue to lose value. But will it happen all at once in a huge crash, or will it continue to decline 2-6% per year like it has for over the past 100 years? I don’t know and Peter Schiff certainly doesn’t know.

He has had no ability to predict how long the powers that be (the big banks, the military industrial complex, the Federal Reserve, the US government) can keep the dollar charade going. He will talk and write about how “The Dollar Will Implode When The Markets Figure X Out” but the market consists of a lot of people who stand to benefit from the charade continuing.

If you listen to Peter you will probably be correct eventually, after all, reserve currencies don’t last forever, but you might not benefit from it in your lifetime. Or you might.

What Can you Learn from Peter Schiff?

I certainly wouldn’t bet the farm on the US maintaining its reserve currency status for the next thirty years. I will remain thankful to Peter for opening eyes to some very real risks the US and the dollar face. But I will never be happy that I missed out on a 100% return if I hadn’t been invested with his firm from 2014-2020. He is not the person I will be going to to figure out how to grow and protect my wealth.

The answer is to take a more diversified approach and to keep your costs down. You can own foreign stocks through a low cost Vanguard mutual fund. Most large non-US companies are listed on US exchanges anyway. Most US companies have large foreign components for their business. When you invest in large US stocks, you are also investing in their non-US sales.

I think owning 5-10% of your liquid net worth in gold and silver is important. I think if you have some extra money to speculate on with cryptocurrencies that could also result in some outsized returns. I think owning hard assets like real estate and yes even some gold and silver is important.

But thinking there is some impending dollar collapse looming on the corner doesn’t do any good. It certainly hasn’t for the past 12 years.

The most important thing about a mistake is to learn from it and move forward. That’s easier said than done and it takes a lifetime of practice.

I’ve made various investing and financial mistakes over the years. It helps to keep in mind that even the most successful people in the world make mistakes.

The seven tips below are a great start to bouncing back from a mistake.

1. Acknowledge you made a Mistake

If you don’t admit you made a mistake you can’t correct the underlying problem and bounce back. This means approaching anyone affected by the mistake and owning it.

Every minute spent denying a mistake was made is time lost in fixing the problem and moving forward.

You might also lose the trust of those around you when you don’t own up to your mistakes.

2. Stop making the Mistake

Once you realize you’ve made a mistake it is important to stop doing whatever you’re doing that caused or is causing the mistake. If you’re spending too much money stop spending too much money. If you keep putting money in losing investments stop putting money in that losing investment.

In some cases there is a temptation to double down or simply try harder when doing so will only exacerbate the situation.

Trying hard is necessary for consistent success and it isn’t sufficient. You can work very hard in the wrong environment and not be successful. You can work very hard but use the wrong tools and be left with poor results. Hard work focused on the right goals using the rights methods is a proven formula for success.

Several years ago I lost a fair amount of money trading options. I kept trying in hopes things would turn around but I kept losing money. So I decided to stop and work on education and mindset.

There is an important distinction between the insanity of doing the same thing over and over again expecting a different result and perseverance. Perseverance requires introspection on your goals and methods.

“The definition of insanity is doing the same thing over and over again and expecting a different result.” – sometimes attributed to Albert Einstein

3. Reboot

Often when I make a mistake I quickly feel some combination of panic, anxiety, shame, loss or any number of other unpleasant emotions. It’s important to reboot.

Maybe it means taking a walk in a park, talking to a trusted confident, going for a run, taking a kickboxing class, meditating or praying. Maybe it is moving to a safer or more comfortable location.

Changing your environment can help change how you’re thinking.

It’s important to reboot, avoid beating yourself up and view the mistake as an opportunity to learn.

4. Reroute

“If you always do what you’ve always done, you always get what you’ve always gotten.” – attributed to Jessie Potter

It’s okay to make a mistake and it’s important not to make a habit of it.

A lot of financial success involves doing a few things right and avoiding big mistakes. At least that is what Warren Buffett has said. I’m not a huge fan of this billionaire hypocrite but I’m still willing to learn from him:

“An investor needs to do very few things right as long as he or she avoids big mistakes.” – Warren Buffett

When you’ve made a mistake it is often a sign that you’re on the wrong path. So it’s important to reroute. If you keep losing money on your investments stop making those investments, learn more, study more, gain the skills you need to make better choices and move forward along a different path.

5. Think about Why you made the Mistake

Change negative questions like, “How could I be so stupid?” to “How was I feeling and what was my reasoning based on that led to this mistake?” “Did I put too much weight in one particular variable?” “Was I impatient?” “Was I afraid of missing out?”

Decisions made out of fear, anger, anxiety, greed, or basically any strong emotion tend result in bad decisions. Think about the emotional state you were in when you made the decision that led to the mistake.

Decisions should be made when you’re calm based on sound reasoning and facts often in conjunction with a mentor, coach or confident. Ultimately you want to have a solid decision making process. Reflecting on what it was that led to a mistake is important for refining how you make decisions.

6. Look for the Silver Lining

Even in the midst of a mistake there are often positive outcomes. It’s an opportunity to grow, an opportunity to learn.

It’s been pointed out that often times we learn more from mistakes than successes.

Maybe some good came in spite of the mistake. Sometimes it is easy to slip into all or nothing thinking with mistakes when there were most likely small victories that occurred in the midst of the mistake.

Sometimes it is as simply as being grateful we didn’t make a bigger mistake.

Sharing mistakes vulnerably with another is a way to build a stronger relationship with that person. Sharing is also an antidote to any shame you might be feeling about your mistake. Having another person to hold you accountable also makes it less likely you will make that mistake again.

7. Never Give Up

“We are not retreating. We are advancing in another direction.” – Douglas MacArthur

As I mentioned before: stopping something is not the same as giving up. If your goals are noble and realistic you should not give up on them. Sometimes it does make sense to move in a different direction but never give up and keep moving towards what is good and worthwhile.

There are many paths to financial success and quitting one path does not mean giving up on the journey.

“Never, never, never give up.” – Winston Churchill

Don’t use a cloud mining calculator without keeping in mind they are static calculations. You need to remember that mining difficulty almost always goes up as time passes.

But don’t worry. If you’re thinking about cloud mining profitability I have an easy rule of thumb you can use to quickly rule out unprofitable cloud mining contracts.

You simply calculate the profitability using a static calculator and determine if you’d make back the initial amount.

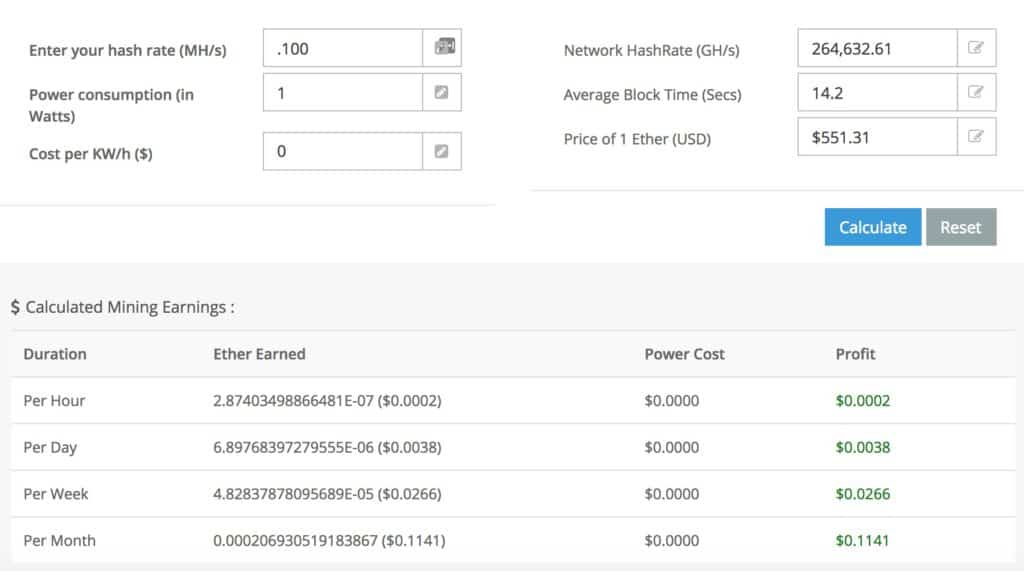

I’ll use hashflare.io as an example, as of 19 March 2018 they are selling 100 KH/s for USD$2.20.

Using a static mining profitability calculator like the one over at etherscan we can see that if network hashing power stays the same, we’ll make a whopping $0.1141 per month or $1.3692 per year. In other words you’ve spent $2.20 to get $1.3692 worth of Ether.

Not smart.

But say the number came back at $3. That would be $0.80 profit per contract. Easy money right?

No.

Don’t Stop with A Static Cloud Mining Calculator

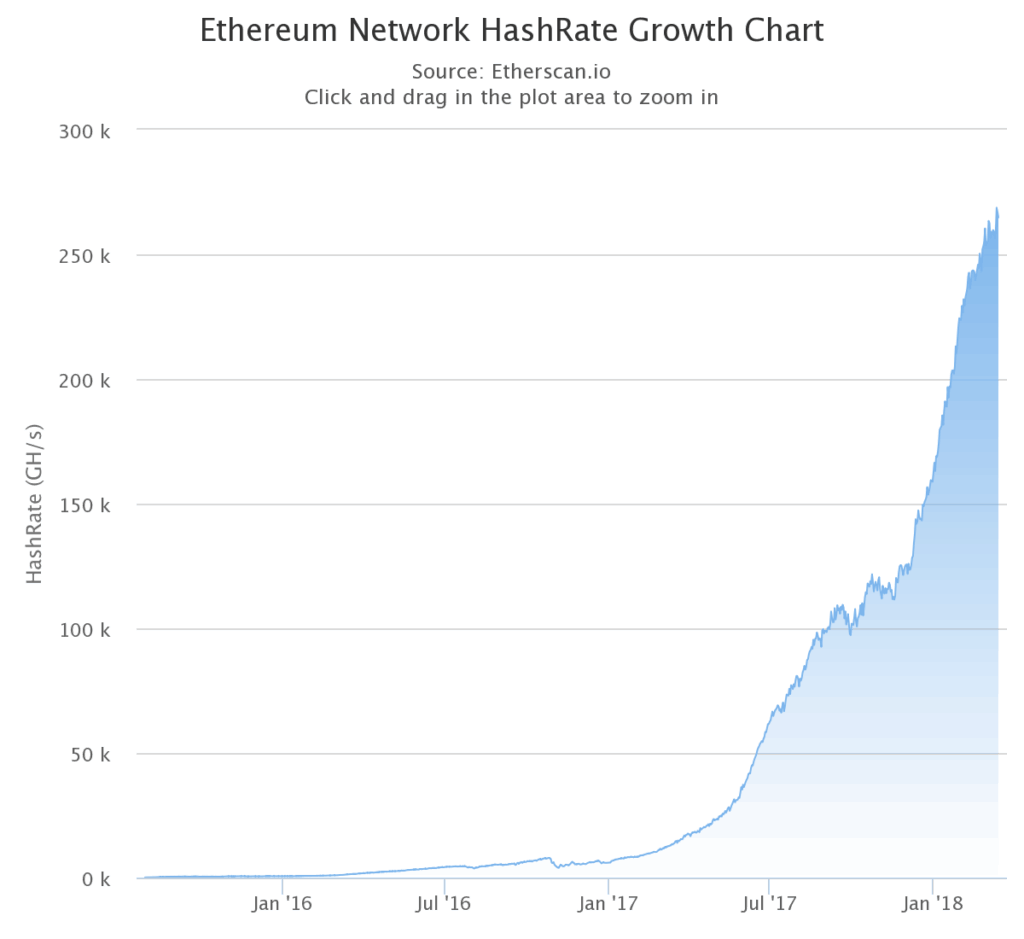

Unfortunately it gets worse, because as I previously mentioned that is using a static network hashrate calculation. As more and more people mine Ethereum the network hashrate increases meaning you’ll mine less.

For example if the network hashrate were to go up to 300000 GH/s you’d only make $0.10 per month.

Network Hashing Power Has Historically Only Gone Up

It’s vital to take into account the growing network hashrate when calculating cloud mining profitability

Is it possible the network hashrate stays the same or goes down?

Yes, but it has never gone down over an extended period of time.

So unless the hashing power of the network stops going up and drops off, there is no way that ethereum cloud mining at hashflare.io will be profitable.

You’re Probably Better Off Just Buying the Cryptocurrency

It’s possible the price of Ethereum goes up and you end up making some money, but you would have made MORE money if you bought ETH directly.

If the mining contract will yield at least the amount you pay, I go to my second rule of thumb. A 50% discount.

I would have to see a cloud mining contract at a 50% discount or more to even consider purchasing buying it. So if hashflare.io was offered 100 KH/s for say $0.65 I would consider it.

With cloud mining you are risking that the network hashrate doesn’t go up too fast and you’re risking that the price of the coin doesn’t go down. I want to be compensated for those risks so I look for a 50% discount.

However, as it stands, ethereum cloud mining at places like hashflare.io is a losing investment, and you’re much better off simply buying the cryptocurrency outright.

I’m not aware of a cloud mining service that has a chance of being profitable. If you know of one please let me know!

I find that the turning of the calendar is as good a time as any to set new goals for the coming year. I’m very much looking forward to seeing what 2018 has in store! So what are some of my goals for two thousand eighteen?

More Visitors!

First I’d like to get 800 users to this website each month. I think I offer exceptional value on this website and I want more people to read what I have to say. In 2017 I averaged 630 users over the course of the twelvemonth and I think 800 is an achievable goal. I have you to thank for meeting my 2017 goal so thank you!

Closer Tracking of Discretionary Spending

Controlling expenses won’t make you rich, but it will prevent you from going bankrupt. It doesn’t matter how much money you make if you spend more than you make. There are countless examples of this happening. I live a fairly frugal lifestyle but I’d like to keep a closer watch on my discretionary expenses to make sure I’m not spending my hard earned money on too many frivolities.

Save $X this year

I’m not prepared to share how much my savings goals are, but I do have a specific amount of money I want to save this year. I’m going to accomplish this via direct deposit.

All the employers I’ve worked for allow me to direct deposit my paycheck into multiple accounts. So I simply set the amount required to meet my goal to go to the account where I store my savings and then forget about it. It’s important to be realistic so that you have enough money to meet your expenses but I find direct deposit is an easy and effective way for me to save money.

Twenty-Eighteen

Those are some of my goals for 2018. I share them because they might inspire you to form goals of your own. I think it’s important to write your goals down or type them up and print them off. Carry your goals with you and have an accountability partner that you check in which to share your progress. Make sure your goals are SMART and think about a WHY. Why are these goals important to you and why will you sacrifice and work to make them happen.

Since this website is about alternative investments and growing and protecting wealth I’ve shared some of my financial goals. But I also have goals for other areas of my life. After all, money is a useful (and necessary) tool but there is a lot more to life.

A year ago I communicated some of my goals for 2017. Today I’d like to review how I did with my goals from last year. In the coming days I’ll share some of my new goals for 2018.

Grow my Trading Account by 8%

This was the least successful of all my goals. I was not able to grow my trading account using the covered call strategy. A number of my value stocks don’t have options, so I wasn’t able to sell covered calls on them. And some of the covered calls I sold were too close to where the stock was trading and the covered call was exercised.

Stick to my Budget

I was rather frugal in 2017 and for the most part stuck to my budget. I would like to watch it more closely in 2018. My strategy is mainly to pay myself first (retirement, savings, investment contributions) and then as long as I’m able to pay for my rent and other expenses without going into debt I’m doing fine. I would like to keep a closer watch in 2018.

Make $1,000 Selling Coins

In previous years there have been some very much in-demand coins that I was able to sell for a goodly profit, however, none of these opportunities presented themselves in 2017 so I did not make any money (or lose any money) selling coins.

Grow HowIGrowMyWealth.com Audience to 500 Users per Month

I had an average of 630 users (as defined by google analytics) per month in 2017. My best month was December, with 816 users. Thank you! So I was able to exceed this goal by 26%!

All in all it was mixed. I exceeded my goals for increasing the audience of this website (again thank you!), however, some of my other goals fell short.

Some of those reasons were outside of my control (exchanges booting US based customers, the mint not creating rare in demand coins). However there are several things I could have done better.

More accountability and tracking

Talking about one’s goals with someone else is critical. I also think it is important to print off your goals, carry your goals with you and check on them on a regular basis. I hope to do ever better in 2018 and look forward to sharing some of my new goals in the coming days.

“With Widespread Power Failures, Puerto Rico is Cash Only” reads the title of a recent New York Times article in the wake of Hurricane Maria. This tragedy in the “Rich Port” is a sad reminder of the importance of keeping some emergency funds in physical cash.

The horrible devastation in this Caribbean territory of the Unites States is another reminder why keeping a few months worth of expenses in cash is a great idea.

It’s also a reminder to the anti-cash types that even in parts of the United States, power restoration can take weeks or months and a society without some cash is economically more vulnerable. This isn’t some abstract problem. It has a face, the face of people waiting in line, not being sure if they’ll be able to buy food or gas because they can’t access their bank account or use their debit card.

If there is a power outage I’m not going to want to spend my gold (the average cashier at the quick mart would probably stare at me dumbly even if I tried), I’m not going to be able to use a credit card, Goldmoney or bitcoin—I need cash.

If you think you’re going to be able to wait for a disaster and then go to an ATM at the same time as everyone else then at best you’re going to be faced with a long line. At worst the ATM won’t work or will be out of cash. Banks will have long lines and they could start imposing withdrawal limits to ration the cash they have available.

This isn’t my theory or some doomsday scenario, this is what happened (and is still happening as I write this) in Puerto Rico.

If people held a few months of expenses in cash then they would be in a better position to buy food, fuel, and start repairing their homes and businesses.

The dollar has lost most of it’s value since 1913. So the wealth you have in cash will be inflated away as central banks inflate the money supply.

2) Theft

Carrying around a lot of cash is generally considered risky and not without reason. Looting and a general increase in crime is an unfortunate reality in the wake of disasters. There is also the problem of civil asset forfeiture. In the United States, the “freest country in the world,” if members of the law enforcement community suspect you of a crime, they have the means to simply take your money and/or other property and it will be up to you to sue the government and prove you’re not guilty and get your property back.

Think of cash as a form of insurance against: 1) Loss of electrical power 2) Capital controls 3) Negative interest rates

And like all insurance it comes at a cost. The cost of holding cash is inflation and the opportunity to put the cash to work in other investments.

I already own various hedges against inflation, such as gold, silver, stocks, and even cryptocurrency, albeit I remain very cautious of this last one. So the fact that a few months worth of expenses in cash losing value is of little concern.

The risk of theft can be mitigated as well:

1) Keep most of your cash in a safe or hidden place

2) Keep it in various locations around your home and perhaps at other locations as well

3) Don’t carry all of your cash at any one time

4) Dress nicely and be respectful to members of the law enforcement community

If two months worth of expenses is $2,000 I’m not saying carry around two grand. Maybe you keep $900 in a safe, $500 hidden someplace else in your home, and $500 with a trusted family member or close friend and a $100 in your purse or wallet. When you go to the store or gas station only take the cash with you that you need. That way if someone uses force to take your money, they won’t get all of it.

The Upsides Makes Holding Some Cash the Smart Move

1) I can be my own ATM. I’m not reliant on a bank or ATM allowing me to withdraw my money. I hold my money. This is vital when everyone is trying to withdraw cash at the same time.

2) If there is a power outage or communication disruption I can still buy food and fuel. Whether it is an EMP, ice storm, hurricane, brownout or cyber-attack, I can still buy the basics of life until things settle down. While fiat money is weak over the long term, in a disaster cash is still king.

Holding a few months of expenses in cash is a great idea. It can also double as an emergency fund in case you have an emergency repair to your car or home, medical expenses, etc.

Smaller denomination bills make more sense. Acquire $10s and $20s not $50s and $100s. Stores are generally more suspicious of larger denomination bills.

Not only that but it allows you to provide for yourself and help others. If I don’t have to go to the ATM or bank to withdraw cash that means there is one less person in line and anyone who would have been behind me in line can get cash faster. If 20-30% of people or more are prepared for a disaster it means there are much fewer people that need to be helped and there will be more resources to help a smaller number of people who need help. Maybe you’ll be able to share some of your cash with a neighbor and help them out.

Cash isn’t an investment and yes it loses value thanks to central banks, but holding a month or two’s worth of expenses in cash is a smart idea as part of a larger wealth and financial protection strategy. My thoughts and prayers are certainly with the people of Puerto Rico and it is a sad reminder of the importance of cash.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

If you don’t admit you made a mistake you can’t correct the underlying problem and bounce back. This means approaching anyone affected by the mistake and owning it.

If you don’t admit you made a mistake you can’t correct the underlying problem and bounce back. This means approaching anyone affected by the mistake and owning it. Once you realize you’ve made a mistake it is important to stop doing whatever you’re doing that caused or is causing the mistake. If you’re spending too much money stop spending too much money. If you keep putting money in losing investments stop putting money in that losing investment.

Once you realize you’ve made a mistake it is important to stop doing whatever you’re doing that caused or is causing the mistake. If you’re spending too much money stop spending too much money. If you keep putting money in losing investments stop putting money in that losing investment. It’s okay to make a mistake and it’s important not to make a habit of it.

It’s okay to make a mistake and it’s important not to make a habit of it. Even in the midst of a mistake there are often positive outcomes. It’s an opportunity to grow, an opportunity to learn.

Even in the midst of a mistake there are often positive outcomes. It’s an opportunity to grow, an opportunity to learn. As I mentioned before: stopping something is not the same as giving up. If your goals are noble and realistic you should not give up on them. Sometimes it does make sense to move in a different direction but never give up and keep moving towards what is good and worthwhile.

As I mentioned before: stopping something is not the same as giving up. If your goals are noble and realistic you should not give up on them. Sometimes it does make sense to move in a different direction but never give up and keep moving towards what is good and worthwhile.