A naked short is when you sell a stock without owning it or having borrowed it first. Naked shorting stocks is supposed to be illegal in the US.

But what is shorting a stock?

Normally, if done legally, one shorts a stock by finding someone who owns, the stock, borrowing it from them (at an interest rate) selling it into the market, then if the stock goes down, one can buy it back and return the stock to the lender. In doing this the number of shares outstanding remains the same.

A naked short is when one sells a stock without first owning it or borrowing it from someone else. The the rest of the process is the same, expect one closes it out by buying the stock back.

So let’s look at a basic example I’m using simple and small numbers to highlight the concept but, if you increase the number of traders and prices and shares, the concept still applies.

Scenario A Example: Short

Acme Co. stock is trading at $1 per share and there are only 100 shares in existence. Person A owns 10 shares of Acme Co. Other people own the remaining 90 shares. They loan the 10 shares to person B so Person A now has 0 shares of Acme Co., person B pays person A interest for the duration they are borrowing the stock, and person B sells that stock into the market at a price of $1 per share to Person C. So they pocket $10 less the interest they paid. There are still 100 share in existence, 10 of which are held by Person C.

Now let’s say the price of Acme Co. stock drops to $0.90. Person B (the short seller) then buys 10 shares of Acme Co. from some other shareholder who is willing to sell for $9 in total. They give those shares back to person A to close their short. And they have just profited $1 less any interest paid.

Now some people don’t like that people can short stock because it is “betting against a company.” Now there are plenty of things I don’t care for but I don’t want to be illegal. I don’t like most of the “popular” music produced today. But I think people should be free to produce music even if I don’t like the result.

I think if I own stock, I should have the right to loan it to others to collect interest. I also think that people have the right to borrow stock from a willing lender. And if someone has borrowed stock, they should be able to sell it (provided both parties agree that the borrowed stock could be sold, and provided the shares are paid back). Since I believe in those two things it follows that people can choose to short stock.

It’s also interesting that people don’t seem to have a problem with borrowing a stock in the hopes that it goes up. Some people essentially borrow stock (using margin accounts) in the hopes that it goes up in value and they can sell it at a profit. You can’t allow people to bet on a stock going up if there isn’t someone taking the other side of the trade essentially betting it will go down.

Now, what I do think should not be allowed (because I believe it is fraud, very much akin to fractional reserve banking), is naked shorting of stock. A naked short is when you sell stock that you don’t own and didn’t borrow from someone else. This essentially introduces new shares of the stock into the financial system that never existed. A company has the right to issue stock, but a random person doesn’t have the right to issue stock in a company they don’t own or control.

So let’s look at our other example only this time it is a naked short. Again, this is illegal in the US in Europe. But it does happen through various loopholes I don’t pretend to fully understand.

Scenario B Example: Naked Short

Acme Co. stock is trading at $1 per share and there are only 100 shares in existence. Various people own the 100 shares. Person B’s broker allows person B to sell 10 shares of Acme Co. stock in exchange for a fee and/or interest. The broker does not own any shares of Acme Co.. Person B sells that stock into the market at a price of $1 per share to Person C. So they pocket $10 less the interest they paid. There are now 110 share in existence, 10 of which are held by Person C.

Now let’s say the price of Acme Co. stock drops to $0.90. Person B (the short seller) then buys 10 shares of Acme Co from some other shareholder who is willing to sell for $9 in total. By buying 10 shares, this closes out their short position. And Person B has just profited $1 less any interest paid and/or fee.

So that is my understanding of you could short a stock beyond the number of shares issues by the company, through naked shorting.

Now the actual mechanics of stock trading behind the scenes is more complex. Trades don’t settle on the same day. Once a trade is closed, it still takes a few days before the trade is settled. Brokers allow buying and selling and they don’t true up their books until later. I don’t pretend to understand all these mechanics.

Scenario C: Short Squeeze

So let’s look at scenario B, only the price of Acme Co. goes up.

The first part is the same:

Acme Co stock is trading at $1 per share and there are only 100 shares in existence. Various people own the 100 shares. Person B’s broker allows person B to sell 10 shares of Acme Co. stock in exchange for a fee and/or interest. The broker does not own any shares of Acme Co.. Person B sells that stock into the market at a price of $1 per share to Person C. So they pocket $10 less the interest they paid. There are now 110 share in existence, 10 of which are held by Person C.

But now: let’s say the price of Acme Co. stock rises to $1.10. Person B (the short seller) then buys 10 shares of Acme Co from some other shareholder who is willing to sell for $11 in total. By buying 10 shares, this closing out their short position. And Person B has just LOST $1 less any interest paid and/or fee. Now $1 isn’t a big deal and Person B in case case can come up with the money to pay it. But on a large scale this can be a big problem.

If the price of Acme Co. had risen rapidly to say $20. Short Seller Person B would need to come up with $10 to close out their short position. If instead of being short $10 worth of stock, perhaps they were short hundreds of thousands of shares and the losses are now in the millions. There is also a problem of liquidity. Maybe no one wants to sell their stock in Acme Co., they are happy to hold it and see if it goes higher. Maybe more buyers come in and are willing to buy in at $20, driving the price up even further. Person B might get into trouble because they might not be enough shares available to buy back and close their short position.

Brokers will often hike margin requirements when markets move quickly in one direction or another to protect themselves. The broker in scenario C where Acme Co. went to $20 might have said to the Short Seller Person B, “you have to deposit another $10 into your account or we will liquidate your position at the current market price.”

I was wrong in my prediction regarding the 2020 election season. I thought it was most likely the red team would retain the senate with Biden in the oval office or what I called “Scenario 3”. I wrote “Scenario 4” was second most likely and that is what happened: Biden in the White House with the blue folks in control of the Senate.

My understanding of the Senate also lacked nuance. While the blue team does have a simple majority in the Senate thanks to 50 members plus Vice President Harris breaking ties, only certain legislation can be passed without a 60 Senator majority. With a simple 51 vote majority the Senate is (somewhat) limited in what legislation it can pass to what is authorized in the budget reconciliation process.

My very superficial understanding of the reconciliation process is that it must pertain to spending and revenue and can only be used once per year. It could be used to raise or lower taxes (for the blues it would be raise) and who knows what other tomfoolery.

Taxing and Spending

But even with the blue group being somewhat limited by the reconciliation process, I can guarantee new taxes and more spending. Perhaps Wall street either likes the tax and spend approach, or the market had already priced in a Biden-Harris Administration, or perhaps it is simply the removal of the election uncertainty for the next two years, combined with vaccine optimism, regardless of how the election turned out.

In any case the S&P 500 is up nearly 9% since November 5th.

Wall Street does seem to love spending, and doesn’t seem to care about the national debt. So while I wouldn’t expect the stock market to crash because of Biden’s tax and spend approach, I do think the economy would fare better under low taxes and fiscal discipline.

Perhaps Trump will say the stock market is magically back in a big, fat, ugly bubble again now that he isn’t in power. I think the stock market has been in a bubble for a while. However, the ability of the powers that be to keep the bubble inflated has far surpassed what I believed possible.

Debt

Even though the blue team is known for spending, their tax hikes don’t cover the bill. To be fair red team doesn’t have many fiscal conservatives either. The national debt goes up regardless of who is in power.

I predicted back in January of 2017 that the US nation debt would go to $40 trillion under Trump. However, under the Trump administration, the debt only went from about $19.9 trillion to about $27.7 trillion. Granted I thought Trump would win reelection at the time I made that prediction and he would have 8 years to run up the debt by over $20 trillion.

Unless Trump runs for office again and wins, my $40 trillion prediction was wrong. However, I think the national debt will go to $40 trillion by the end of 2024.

I think over the next four years it will go from $27.7 trillion to over $40 trillion. It would mean about $3 trillion per year. In 2020 the national debt increased by $4.2 trillion. I’m sure Biden will be looking for a big spending package in 2021 to get his administration started off with a bang.

Government spending financed by debt reduces the value of dollars, so more dollars are required for later stimulus in order to have the same effect. For example in 2008, when the banks were being bailed out the debt went up by about $1 trillion. Then the next year the debt went up by $1.8 trillion.

Granted 2020 had COVID-19 and lockdown crisis, but that hasn’t gone away. In 2018 and 2019, with the economy supposedly humming along and no large-scale military engagements, the debt still increased by over $1.2 trillion each year.

My $40 trillion prediction is based on the national debt going up by $4-5 trillion in 2021, followed by $2.5 trillion per year after that.

This is one reason why interest rates can’t rise. The treasury issues debt at a variety of maturity rates. But as interest rates rise, that means the government has to pay out more money on the debt. The treasury is already paying about $393 billion per year in interest at current rates.

In June of 2007 the yield on a 10 year treasury was 5%. In the wake of the 2008 financial crisis it has steadily fallen. While still stupidly low, the 10 year treasury yield has been rising. In July of 2020 it was as low as about 0.5%. Since then the yield has risen to about 1%. As I said before it is still stupid low, in contrast the 10 year treasury yield was 15% in the early 1980s.

However, the market is addicted to low interest rates. If the 10 year yield continues to rise and gets to 3 or 4% I think that would be devastating for stocks. As mentioned above it would also dramatically increase amount the treasury would need to pay in interest. For example at 0.5%, $2 trillion would cost $10 billion, but at 3% it jumps up to $60 billion. But it isn’t just the new debt, as older debt expires and the borrower gets paid back, the treasury issues new debt to pay for it, which must be issued at the new rates.

I’m sure the Federal Reserve will step in and drive the yield back down before that happens. The Washington elite definitely don’t want a stock market crash to happen when the blue team is in control of the government.

Warfare

I think the Biden-Harris administration is much more likely to increase hostilities in the world. Despite all his faults, and alienating allies of the United States, Trump didn’t start any major military engagements in the world. I believe Biden-Harris will follow the Bush II and Obama approaches to foreign policy.

More war is good news for “defense” contractors, but less positive for everyone else. The loss of human life in war is the most tragic element and the most important reason to avoid military action except as a last resort. A distant second reason for avoiding war is that bombs, drones and aircraft carriers are expensive and contribute to the national debt. Surely the military action, as it always is, will be dressed up flowery rhetoric to make it seems necessary, noble and courageous.

Wealth Management

I think a 10-20% allocation to precious metals is as important now as it ever was. Gold has been down and sideways since the new high was made in August of 2020. It seems to have support at around $1,790 per troy ounce. I think this is consolidation prior to the next leg up.

Stocks only seem to go up. Valuation and fundamentals don’t seem to matter.

While I always have some exposure to the stock market, I’ve missed out on the some of the gains of the last 8-9 years since I’ve been underweight US stocks. I’ve been waiting for a buying opportunity. I was considering buying in around March of 2020, but I expected the markets to go lower.

I was wrong.

The powers that be are able to maintain the stock market prices far beyond what makes sense to me. I’m planning on averaging into various mutual funds over time. Perhaps my capitulation is a sign that the top is near!

Despite all the challenges from higher taxes, more regulations, debt and lockdowns, there are still productive businesses out there. While I think Biden/Harris and their allies on the blue team will make things worse, there are still plenty of reasons to be optimistic. Being in a “bunker mode” for the past 8 years has cause me to miss out on a significant stock market rise. At some point I think the dollar will crash and maybe stocks will go down too, but that is what the precious metals are for.

Stocks go up when China and Trump say or do something nice to each other and then stocks fall when they leave meetings early, don’t meet, or say something mean.

It is a tiresome game that has been going on for some time. It seems like China and Trump are fundamentally at odds with each other and any real trade agreement is impossible.

I think the best thing Trump could do (if I was his campaign adviser) is declare victory, focus on and inflate some arbitrary thing he got from the trade war and then promise no more tariffs.

The United States benefits much more than China from trade between the two countries. China loans money to the US then the US buys cheap goods from China with said money. China gets pieces of paper (or the electronic equivalent) saying the US will pay them back. It is the ultimate vendor financing.

The Fed Caves to Trump

Despite low unemployment numbers, “contained” inflation the stock market near all time highs and all the other supposed reasons why the economy is the best ever, the “independent” United States Federal Reserve cut rates last week. The Fed funds rate is now back down to 1.75-2.00% because of….reasons?

This was all but assured as far as the market was concerned.

The market has been going up, up, up for the past ten years. The Fed is cutting rates when the economy is supposed to be doing well, when the next downturn hits, what is the Federal Reserve going to do?

Between the trade wars and the federal reserve, can we please stop pretending that the United States is a free market economy? Please?

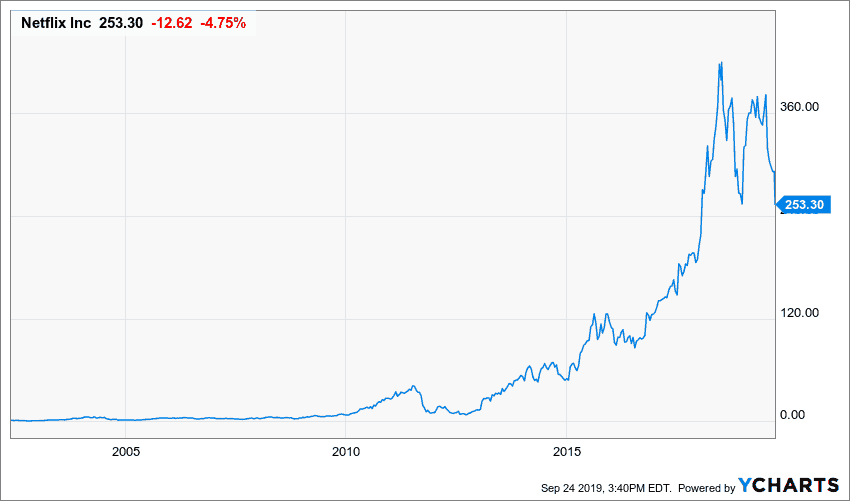

Netflix Tanks

Netflix (NFLX) has been getting pounded.

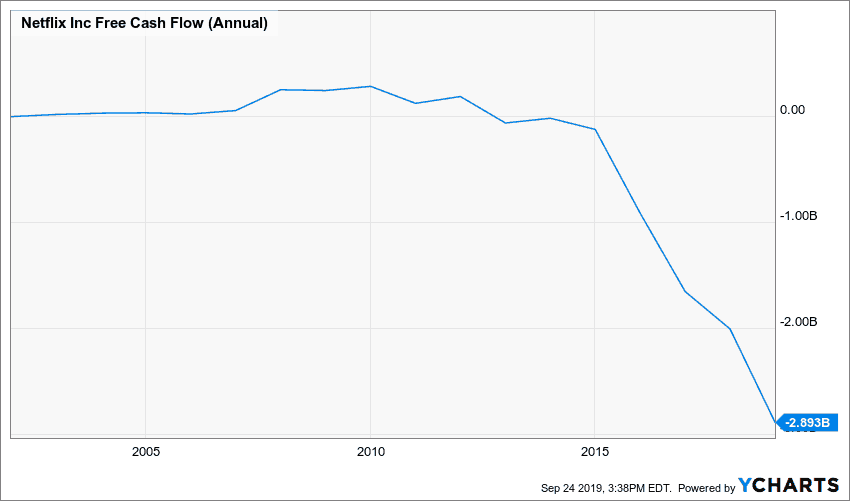

Netflix doesn’t make money. Since 2011 they have lost money each year and they have to keep borrowing more money just to keep making content.

One of my key metrics in evaluation stock is free cash flow. It’s like earnings only harder for accountants to monkey with. Netflix has not had positive free cash flow since 2011.

Looking back three years free cash flow at Netflix was a negative $1.66 billion in in 2016, negative $2.01 billion in free cash flow in 2017, negative $2.89 billion in free cash flow in 2018 and are on track to lose over $3 billion this year.

Netflix is a classic example of great product, lousy business. It looks like the market is finally waking up to the fact that Netflix is not a good investment.

With more competition from the likes of Apple and Disney, I don’t expect this show to have a happy ending for Netflix.

What is John Doing?

I’m well positioned for what the market has been doing. Of course I missed out on some of the meteoric rise over the past 10 years, but it is good to finally see my positioning pay off.

I’ve been raising cash all year and sitting on gold holdings. I am in the market some, but I’m certainly overweight cash. I did start shorting Netflix when it was about $325.

I still like gold (and silver), gold stocks and value-oriented international stocks. I still think it’s important to be invested in the US some, but not a lot.

I think Netflix is still overvalued even after the large selloff and I think it will go down to the $150 range (or lower) over the coming couple of years. I only short with money I can afford to lose because it is risky and tough.

Shorting is harder than going long because you have to get both the direction and timing correct. If you’re long you only have to get the direction right (although timing is nice here too).

I don’t recommend shorting Netflix or any other stock.

I’m not worrying. Economic downturns don’t happen immediately. They are gradual, the market springs back even in the midst of selloffs. Take some prudent steps to diversify outside of mainstream investments and don’t worry about it. Build up an emergency fund, live within your means and live your life.

Electric car company Tesla has a market capitalization over $40 billion. Over the past few months the stock (TSLA) has lost nearly a third of it’s value dropping from $360 per share down as low as $244.

Bonds issued by this electric car company are yielding higher than that of Ukraine (indicating higher risk) and recently the autopilot on one of their cars resulted in a death.

Tesla as a company is not exactly in great shape. The stock was already trading down to the year lows.

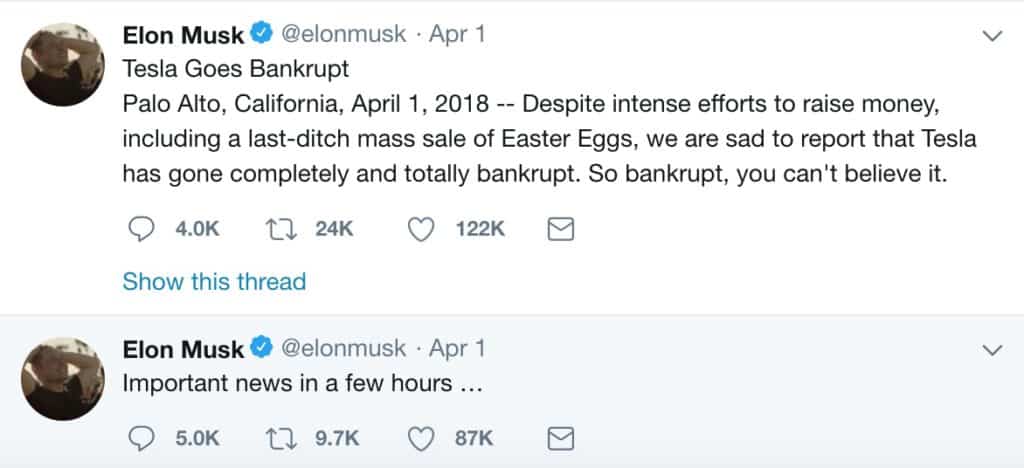

Now it’s 1 April–what does CEO Elon Musk decide to do?

Elon decided it would be hilarious to tweet about his company going bankrupt.

CEO Elon Musk tweeted out some “jokes” about his company filing for bankruptcy

Now if Tesla was humming along nicely this would be little more than a sophomoric prank by an eccentric billionaire.

However Elon’s company is performing extremely poorly.

In terms of free cash flow Tesla has consistently “generated” negative free cash flow in the billions since 2014. It’s free cash flow has been negative as far back as I can find data (2008).

Many other metrics are similarly dismal.

Negative margins, $.51 worth of liquid assets for every dollar of current liabilities, negative return on assets and a negative return on equity.

If you just looked at the balance sheet and didn’t know what company it was for you’d have a hard time finding anything positive to say.

This is all in spite of receiving billions in subsidies from the government.

Elon was probably onto something and it does seem likely that his company will eventually file for bankruptcy.

Tesla is an example of an overvalued stock that is ripe for crashing (even further). What are the fundamentals that justify such a high valuation of a company that destroys cash?

Why can’t genius businessman Elon Musk turn a profit despite massive government subsidies?

Tesla (TSLA) and Netflix (NFLX) are two examples of darlings that are propped up by hope and cheap money.

Investors can continue to hold stocks like this but eventually profits and fundamentals will matter again.

Normally you’d have to pay a lot of money for the type of in depth analysis I’m providing here on Royal Dutch Shell. Take a moment to sign up to my zero-cost-to-you spam-free email newsletter for future analysis on stocks, financial markets and alternative investments.

Overview of Royal Dutch Shell

Royal Dutch Shell (RDSb London Stock Exchange, RDS.B NYSE) is in my opinion a fantastic stock that is undervalued. It’s been profitable even in years in which oil prices were plummeting.

In an environment where traditionally safe investments are risk free reward Shell stock provides an attractive 5.86% yield. While I don’t provide personalized investment that is suitable for an individual’s unique situation I have determined that owning stock in Royal Dutch Shell makes a lot of sense for me.

When I value a stock there are a number of metrics I look at when evaluating a security:

1) Enterprise Value to Market Capitalization (EV/Market Cap)

2) Enterprise Value to Free Cash Flow (EV/FCF)

3) Enterprise Value to Earnings Before Interest and Tax (EV/EBIT)

4) Enterprise Value to Owners’ Cash Profits (OCP)

5) Operating Margin

6) Dividend Yield

7) Return on Equity (ROE)

Energy production is very capital intensive so I’ve compared Royal Dutch Shell (RDSb) to similar companies: Exxon Mobil (XOM), Total (TOT), and Chevron (CVX).

Data is from Morningstar.com as of 13 March 2018 (with the exception of EV/Owner’s Cash Profits) which is from yCharts.com as of 16 March 2018.

So how does RDS compare to other oil companies of a similar size?

1) EV/Market Cap

I like to see an EV/Market Cap below 1. Of these four energy companies none meets this criteria and RDSb is actually the highest. Total is the lowest just edging out Exxon Mobil by what amounts to a rounding error.

RDSb – 1.242

XOM – 1.134 TOT – 1.129

CVX – 1.154

Winner: Total (TOT)

2) Enterprise Value to Free Cash Flow (EV/FCF)

EV/FCF is where RDSb really shines compared to it’s peers. EV/FCF is in my view a more accurate measure than Price to Earnings (PE). The lower the Enterprise Value compared to Free Cash Flow means you’re paying less for an earnings stream.

RDSb – 19.55

XOM – 24.42

TOT – 28.99

CVX – 36.15

Winner: Royal Dutch Shell (RDSb)

3) Enterprise Value to Earnings Before Interest and Tax (EV/EBIT)

Another metric which I think is superior to Price to Earnings where a lower is better.

RDSb – 18.31

XOM – 18.57 TOT – 14.68

CVX – 26.98

Winner: Total (TOT)

4) Enterprise Value to Owners’ Cash Profits (OCP)

16 March 2018 Update:

EV to Owners’ Cash Profits is yet another metric that I believe is more accurate than price to earnings.

Shell has a payout ratio of 144.6% which means that the dividend might be unsustainable.

However, Royal Dutch Shell’s payout ratio has been below 100% from 2008 up through 2014 and I think that the payout ratio will drop to a sustainable level in the next year or two.

The return on equity for shell has also been lower than I’d like but they are also in stronger financial shape (based on the current ratio and quick ratio) than ROE king Exxon.

Another Valuation Metric for Royal Dutch Shell

One way to calculate a margin of safety is by determining what multiple of the EBIT the stock is trading at. I could write an entire article on how this is calculated (shout out to Jason Rivera who I learned this technique from).

Using the number 14 in the equation might seem somewhat arbitrary but it isn’t. The reason I chose that is because if you plug in 13.5 you get the current share price of Shell. In other words Shell is trading at EBIT x 13.5 + Cash Equivalents.

Using this metric (using a multiple of 14) we find a “fair” share price of each of these four stocks would be as follows:

RDSb – $65.9

XOM – $64.1

TOT – $75.8

CVX – $72.7

And if we compare the actual share price to these values we get the following “margin of safety” for each stock:

Using this technique we can see that Royal Dutch Shell is trading at about a 3.5% discount to 14xEBIT + Cash. Exxon is trading at a 16.27% premium, Total is trading at a generous 23.91% discount and Chevron is overvalued by a large 60.12%.

Royal Dutch Shell Class A or Class B Shares?

I used to own RDSa in a Roth IRA. The RDSa shares are subject to a 15% withholding to the Dutch government. Because of this RDSa trades at a discount to RDSb, which does not have this withholding.

At one point you could get around the 15% withholding through Shell’s scrip program (which they have discontinued twice) and get a lower price and higher yield. So it made sense to own RDSa.

But given that the scrip program has been discontinued I choose to own RDSb. I prefer to own it on the London Stock Exchange and I also own it in US markets in a Roth IRA.

Royal Dutch Shell is an Excellent Value

Shell is a great value, a cash flow machine, and pays with a strong dividend. Total is an excellent value as well although it has thin operating margins and has struggled to generate free cash flow with the same consistency as Shell and so for those reasons I prefer Royal Dutch Shell.

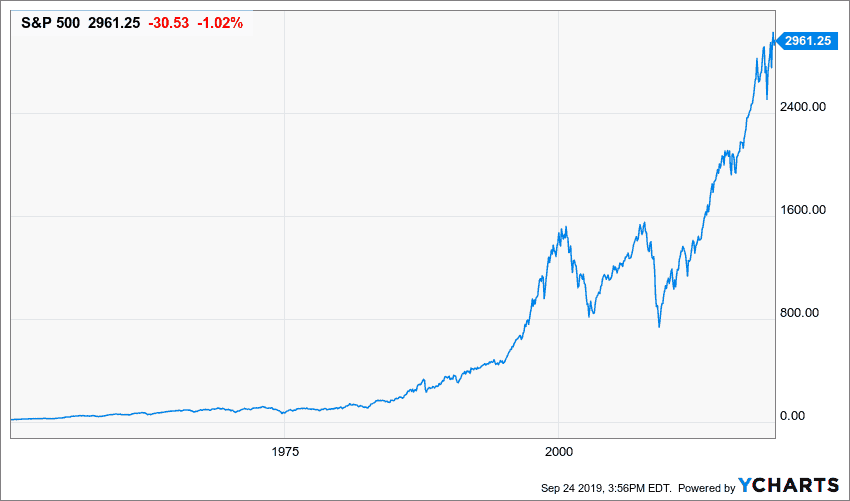

The S&P 500 was down nearly 10% from it’s January high after another significant selloff on Friday. Eight out of the last ten trading days had been negative. At Friday’s close S&P 500 was down almost 4% in 2018. The NASDAQ was flat in 2018, down 10% from the highs. The Dow Jones was down 5% on the year and 11.6% from the highs.

S&P 500 down nearly 10% from the high at the close on Friday

Gold has looked relatively stronger. The yellow metal was up a modest 2.14% on the year.

With gold holding it’s value and US equity markets in correction territory I was asking myself over the weekend, “is this the start of something bigger?”

Since the lows in 2009 the S&P 500 has made some large drops. From high to low the S&P 500 dropped 17% in 2010. It went down 22% between April and September in 2011. From July of 2015 to February 2016 the S&P dropped 15%. There have also been 10% drops like in the spring of 2012 and fall of 2014.

A 10% correction in and of itself is not a big deal.

But I think when combined with trade war brewing with China, rising interest rates (at least nominally), a $1.3 trillion spending bill and simply being 9 years into a bull market–this could make for the start of a larger selloff into a new bear market.

From a technical perspective this correction has been more violent than previous ones. In the first 18 days of trading in 2018 all but 14 were positive and the S&P 500 rose 7% from 2,682 up to 2,872 only to reverse and over 10 days (only 2 of which were positive) drop down 11.8% to 2,532.

I think it is fair to say that is one of if not the most violent rise and reversal since the 2009 lows.

The 2008-2009 crisis saw a 57% stock market crash. A similar drop from the new high would result wipe out 7 years of gains.

I don’t think the US Federal Reserve will let the markets drop 57%. I think they will cry uncle if there is a 40-50% drop, they will freeze all rate hikes and may even start lower rates again.

Gold and emerging markets should do very well in this environment.

Monday Market Rally

The S&P 500 opened up at 2601 this morning and went up to 2661 and closed near the highs at 2658.

Gold did not sell off however, it actually rose to near the highs of the year.

We’ll see if gold can breech the resistance that has thwarted a larger rally for the yellow metal this year.

As previously mentioned the S&P 500 has dropped like this before. It hasn’t been this rapid before. But given additional negative factors, perhaps most significantly rising interest rates. I believe this could be the start of a larger correction.

I certainly don’t know for sure, if I had a crystal ball I’d be much richer than I am now. But it is important to be diversified in non-correlated alternative investments.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.