Peter Schiff is Chief Economist & Global Strategist at EuroPacific Capital. He is also chairman of a gold reselling company. He appears on RT and has authored several books about the collapse of the dollar. Peter is a vocal critic of the US Federal Reserve and warned loudly about the housing bubble prior to the 2008-2009 financial crisis.

I owe much of what I know about the Federal Reserve to Peter Schiff. I’ve read some of his books and used to listen to his podcast.

But I’ve come to realize that Peter Schiff is not someone you want to listen to for financial or investment advise. The following are some key areas where I think he goes wrong.

His EuroPacific Funds are Expensive and Underperform

I invested some money with his firm, EuroPacific Capital between December 2014 and December 2020.

During that 6 year timeframe, my investments with EuroPacific Capital went up 20.5% (about a 3.8% annualized return) which doesn’t sound too bad until you consider the S&P 500 doubled in price during that same timeframe and provided an annualized return of nearly 15%.

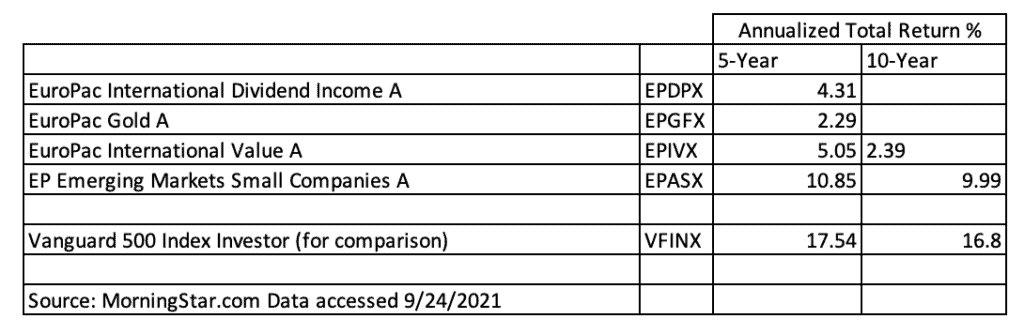

Peter’s firm EuroPacific Capital, charges what I consider to be high load fees and they underperform. For someone who preached about inflation, you’d think he’d make sure his funds at least beat inflation. They don’t. Looking up his funds on MorningStar, you can see the poor 5 and 10 year returns.

The EuroPac gold fund has a 5-year annualized total return of 2.29%. Inflation has been well over that for the past five years.

His Bias for Gold and Silver Blinds Him

Some might consider me a gold bug. I believe gold and silver are an important part of a diversified portfolio. But with Peter being a gold salesman, he is overly biased towards gold, this has caused Peter to miss out on an emerging asset class (cryptocurrencies) that while more volatile, has far outperformed gold. He has unsuccessfully predicted many tops to this asset class.

Not only that, but he’s failed to predict where all the Fed money printing would go. It’s gone into real estate, stocks, cryptocurrencies. It hasn’t gone into gold, silver and foreign stocks the way he has been predicting.

He Can’t Time the Dollar Crash

Peter Schiff is the boy who cried wolf.

Sometimes there is a “wolf” and when there is, it’s is important to let other people know there is a wolf so we don’t all get eaten.

Peter did correctly cry “wolf” before the 2008-2009 “wolf” reared its head. But he’s been wrong ever since.

Peter is a big fan of extended metaphors. So here is one for him. Peter is the boy who cried wolf, no one believed him and it turned out there was a wolf and he was right. Then he cried wolf again over and over again for the next 12 years as if the wolf was just behind the bushes, even though the wolf was 500 miles away.

His rhetoric that the dollar crash is imminent might be an effective sales tactic in the short term, but he has been wrong since the 2008-2009 financial crisis. It weakens his message and erodes his credibility to the point that I don’t listen to him anymore.

He has not been able to time when the dollar will crash. I agree the US Federal Reserve is reckless, is a prime cause of market crashes and price inflation. There is no question the dollar will continue to lose value. But will it happen all at once in a huge crash, or will it continue to decline 2-6% per year like it has for over the past 100 years? I don’t know and Peter Schiff certainly doesn’t know.

He has had no ability to predict how long the powers that be (the big banks, the military industrial complex, the Federal Reserve, the US government) can keep the dollar charade going. He will talk and write about how “The Dollar Will Implode When The Markets Figure X Out” but the market consists of a lot of people who stand to benefit from the charade continuing.

If you listen to Peter you will probably be correct eventually, after all, reserve currencies don’t last forever, but you might not benefit from it in your lifetime. Or you might.

What Can you Learn from Peter Schiff?

I certainly wouldn’t bet the farm on the US maintaining its reserve currency status for the next thirty years. I will remain thankful to Peter for opening eyes to some very real risks the US and the dollar face. But I will never be happy that I missed out on a 100% return if I hadn’t been invested with his firm from 2014-2020. He is not the person I will be going to to figure out how to grow and protect my wealth.

The answer is to take a more diversified approach and to keep your costs down. You can own foreign stocks through a low cost Vanguard mutual fund. Most large non-US companies are listed on US exchanges anyway. Most US companies have large foreign components for their business. When you invest in large US stocks, you are also investing in their non-US sales.

I think owning 5-10% of your liquid net worth in gold and silver is important. I think if you have some extra money to speculate on with cryptocurrencies that could also result in some outsized returns. I think owning hard assets like real estate and yes even some gold and silver is important.

But thinking there is some impending dollar collapse looming on the corner doesn’t do any good. It certainly hasn’t for the past 12 years.

I want to give credit to Bitfinex. They paid back all their IOUs by redeeming 100% of all BFX tokens.

These BFX tokens were issued as a placeholder for Bitfinex account holders who received a haircut of 36% when 119,756 BTC was stolen from Bitfinex on 2 August 2016.

Back in January I sold my remaining BFX tokens for .55 USD per token. If I had held onto them today I would have gotten 1 USD per token.

With the benefit of hindsight that was not the best call.

However, it’s pointless to evaluate a decision based on information that wasn’t available at the time. I don’t think I could have known that Bitfinex was going to aggressively redeem the IOUs at such an accelerated pace.

With that in mind I made the best decision I could with the information available to me at the time.

On August 2 Coindesk reported a hacker stole some $60 million worth of Bitcoin from the Bitfinex exchange. Altcoins such as ETH, ETC, LTC on Bitfinex were not stolen by the hacker.

Bitfinex decided to “socialize” the losses in what they claim would be similar to a bankruptcy liquidation.

All account holders on Bitfinex at the time of the hack received the newly created BFX tokens equal to roughly 36% of their pre-hack balance in place of the losses.

The tokens were issued at a one token to dollar parity. For crypto currency balances the value was based on prices announced by Bitfinex.

Interestingly before trading was live the ticker already priced BFX at .80 per token–a 20% discount.

As of writing tokens are trading down around $.36.

But this low price creates an opportunity for the exchange Bitfinex. They could buy their own tokens back at a huge discount and then forgive their own debt.

Debt Buyback: An Example

Let’s say you borrow $100 from your friend Robert. You give Robert a piece of paper promising to pay him back (an “IOU”).

You fall on hard times and Robert is convinced you won’t make good on your promise to pay him back so he decides to cut his losses.

He sells the IOU to Susan for $25. Robert figures $25 is better than $0.

Susan holds the IOU for a little while but then decides she wants the money. She offers to sell the IOU for $30.

You could buy your own IOU back for just $30 and then forgive the debt to yourself.

In other words you’ve just gotten $100 for $30.

See where I’m going with this?

While no one voluntarily loaned money to Bitfinex in exchange for the BFX tokens my hypothetical example above is very similar to the position Bitfinex finds itself.

Bitfinex public relations man Zane Tackett claims they do not buy their own debt on the exchange.

The best people like me who were assigned the token can hope for is Bitfinex will pay the face value back in full as soon as possible.

I don’t see how the BFX tokens will ever be worth $1 or more via trade. If Bitfinex releases a legally binding repayment plan I could see the token value approach $1. For example, if Bitfinex announced BFX tokens would be repaid on 8/14/2016, they might trade up to $.99 per token leading up to the payout for people to make .01 per token in one day.

Why is that the case? Because a rational investor will not voluntarily buy an instrument today for the promise of the same (or less) amount in the future. A rational investor wants to be compensated for the time value of money.

Plus there is a lot of risk that the amount will never be repaid. The BFX tokens are reward-free risk for anyone assigned the token.

It beats just taking the full 36% loss, but falls far short of my hopes for interest, equity, tradability (for US clients) and a set maturity.

Presumably the tokens could be held to “maturity” at which point Bitfinex would buy them back at face value but if maturity is 1 or 100 years from now, tomorrow or never, no one knows.

That could be a long time with no interest which is a big fat loss both in terms of lost opportunities to invest the money elsewhere and purchasing power lost due to price inflation.

BFX Token Winners

As mentioned earlier in this article, if Bitfinex were to buy back their own debt at current token prices they would be saving 64% on their outstanding debt.

Other winners could be risk loving speculators. With the token trading at just $.36 speculators who believe that Bitfinex will buy the tokens at face value could buy BFX tokens at a huge discount.

For example if I could buy BFX tokens for $.36 each and I knew I’d get a dollar for them in a year it’d be a no brainer investment.

Roulette or BFX Token: Which is riskier?

But since their isn’t any interest, no set maturity, and no guarantee if the tokens will ever be repaid, the BFX tokens are little better than putting your money on red at the roulette table.

What is a Bitfinex Client to do?

If you were assigned BFX tokens at face value and you’re a US resident you’ve only got two options. The first is sell the BFX tokens to cut your losses. The second is to hold onto them and hope they go up in value or are repaid.

If you’re not in the US you could double down and buy BFX tokens to decrease your BFX token cost basis, but I think this is super high risk.

I’m still sitting on my BFX tokens to see what happens. At some point I may cut my losses and sell them but I haven’t made a decision yet.

If you feel like gambling and you’re not a US resident you could buy BFX tokens and hope Bitfinex pays them off. But with no set maturity, no guarantee of repayment and no interest it’s certainly not investing.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.