Back when I was an impressionable college student I was shown an asset allocation rubric. The rubric was a list of asset classes with a recommended percent of funds to be invested in each asset type. The result would be a diversified portfolio.

It was my first exposure to asset allocation and it made a lot of sense.

The allocation I was presented was very similar what I have listed below and I’ll call it “Portfolio 1”.

Asset Allocation Portfolio 1

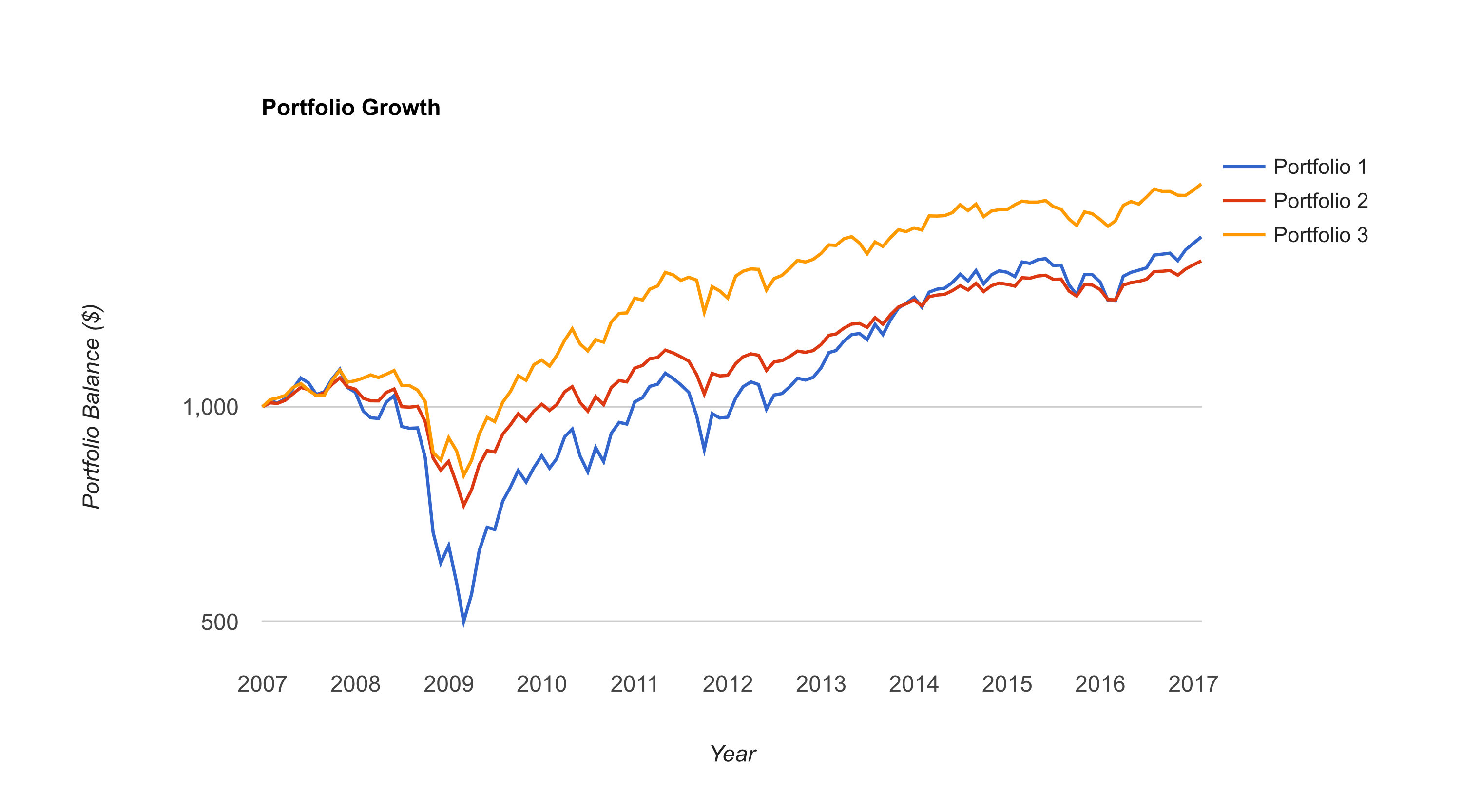

The problem with this portfolio is that is dropped over 55% in the 2008 financial crisis.

Without any bonds (or gold) this portfolio was subject to a massive drawdown.

Since January of 2007 to January of 2017 this portfolio has a compound annual growth rate (CAGR) of just 5.58%.

Plus the correlation with US stocks is .98.

In fact an investor would have been better off just buying the Vanguard Total Stock Market Index (VTSMX) and calling it a day. The “Just Buy VTSMX” strategy would have had a 7.25% CAGR with a lower maximum drawdown of around 50%.

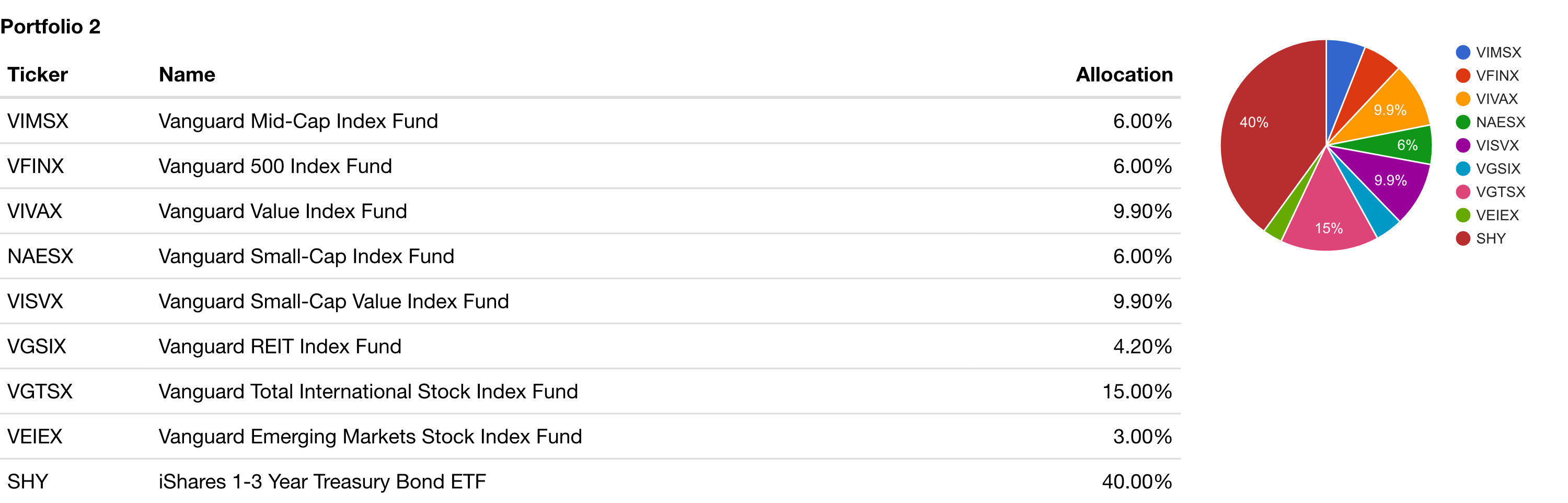

Asset Allocation: Portfolio 2 (Add Bonds)

To be fair, the allocation actually calls for a 40% allocation to short term bonds. Adding 40% bonds would have limited the maximum drawdown to a much more manageable 33.72% with a CAGR of 4.77%.

Correlation of this portfolio is still .98.

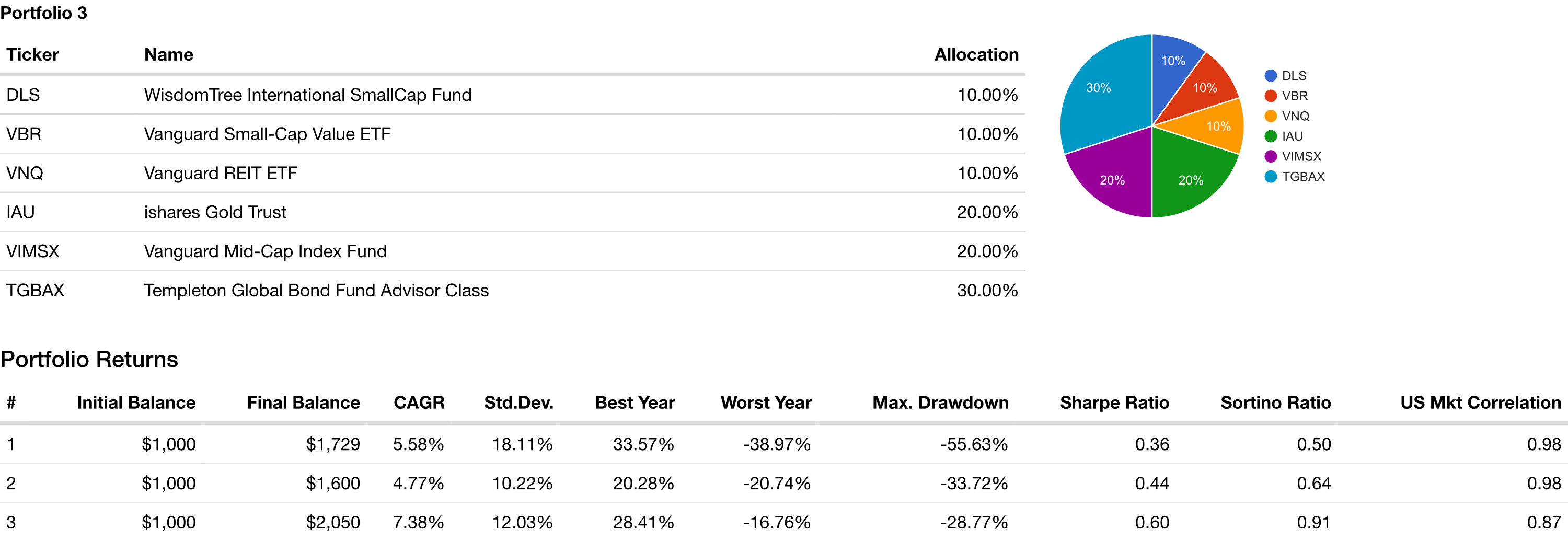

HIGMW Asset Allocation

But enduring a 33% drawdown for a a 4.77% return doesn’t seem stellar to me. So I’m been experimenting with different asset allocations using portfoliovisualizer.com.

The HIGMW Asset Allocation I’ve developed would have a maximum drawdown of 28.77% with a CAGR of 7.38%. Correlation with US stocks drops below the 90s down to .87, still high, but at least lower.

Now the actual investments in my allocation are listed below. I had to swap out some funds in order to get a sense of how this allocation would have performed in 2008.

However, many of the funds I like did not exist in 2008.

Yes, this allocation is 30% bonds. And yes, I think US stocks and bonds are in a bubble. And yes indeed I Don’t Own US Treasuries. But 20% of my allocation to bonds are outside the US and the other 10% are in a fund managed by Bill Gross mainly consisting of corporate bonds and only 6% in government bonds.

So my 30% allocation to these bond funds in no way contradicts my views on US debt.

I also allocated 20% to gold and 10% to real estate. I think if inflation does pick up (even more) these hard assets will add some resilience to the portfolio.

Small cap value stocks have outperformed over the last 45 year so I’m overweight small cap value. 10% is allocated to international small cap value stocks and 10% to small cap value stocks in the US. The 20% allocation to the First Trust Dorsey Wright Dynamic Focus 5 ETF is an interesting ETF in that it is somewhat trend following. Combine these three funds and 40% of this allocation is to stocks.

Gold doesn’t pay a dividend or yield. But until the central banks around the world stop acting like crazy people gold will remain a large part of my portfolio.

I don’t think I can be convinced that governments can continue to borrow, print and spend money without consequences.

Just about four years ago I wrote the first article on HowIGrowMyWealth.com “Inflation Destroys Dollars“. I wrote about how what I do to protect against price inflation and dollar devaluation. Specifically value investing and precious metals. So in retrospect, how did those investments do?

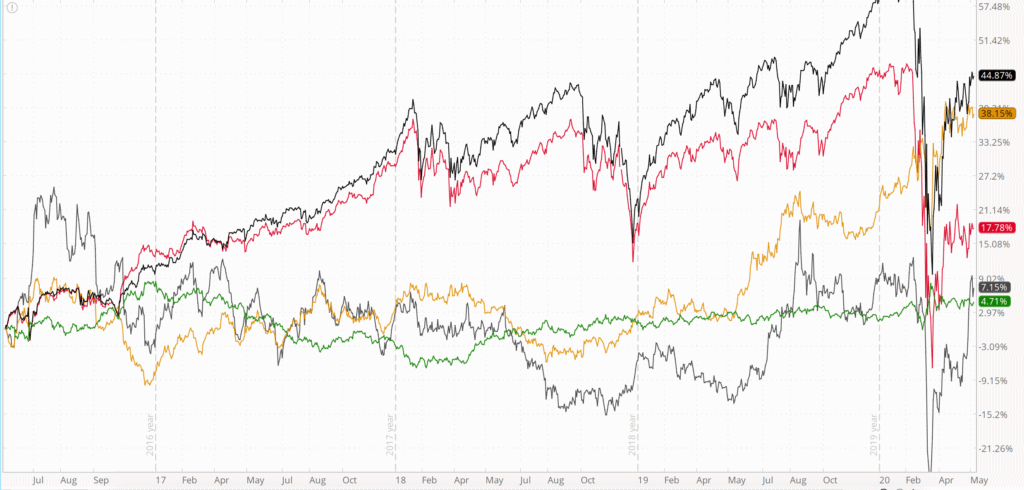

As a control we’ll add the U.S. Dollar Index ($DXY, shown in green), which compares the dollar’s strength against a basket of other currencies. To represents “stocks” I’d added the S&P 500 Index (SPX) (shown in black).

I’m using the Vanguard Large Cap Value ETF (VTV) as a proxy for value stocks (shown in red). You can see how my current and past individual value stock picks have done here. Gold futures are in yellow and silver futures in gray.

As you can see the S&P 500 has been the place to be. To be fair gold isn’t too far behind. Gold was in fact keeping pace with and surpassing S&P 500 this past April. So while gold has been a good hedge and having exposure to stocks has continue to be important.

Value stocks have lagged the S&P 500, particularly in the aftermath of the December 2018 selloff.

Silver is only slightly outpacing the dollar index, up just 7.15%. Silver has had a few failed breakout attempts, but continues to underperform. The gold/silver ratio that some precious metal bugs talk about would suggest that silver is a better value right now.

Costs continue to rise each year as the dollar loses value. But as measured by the DXY the dollar has kept its value against other currencies.

As I wrote back in November of 2016 in “I Own Too Much Gold“, you don’t want to own too much gold as a percentage of your net worth. The performance of the S&P 500 is a good reason why. If gold ever were to take off a 10-25% allocation would be more than sufficient.

We certainly haven’t see broad hyperinflation yet in the US, but my rent, food and medical costs continue to rise each year in excess of the government measured CPI. As I have for the past four years, gold and precious metals remains an important (albeit minority) portion of one’s portfolio.

If you are just starting to buy precious metals emphasizing silver over gold (while still buying both) could be a good approach.

I previously wrote an article, “I Own Too Much Gold” and I’ve gotten several replies on twitter such as, “Impossible” and “No Such Thing”.

I strongly suspect (although I can’t prove it) these folks didn’t read the article. But in case they did and still aren’t convinced here are five reasons why you don’t want to own too much gold as a percentage of your asset allocation:

Reason 1: Lack of Tax Benefits

In the US, gains on physical gold are taxed as ordinary income, which could be a lot higher for you than the capital gains rate.

Even if you were an uber-gold bull and thought it was going to $100,000 per ounce would you really want to pay all your taxes on those gains as ordinary income?

Why not invest in some gold mining stocks (which would certainly go up as well if gold skyrocketed) and pay the capital gains tax rate? Why not hold some of those gold mining stocks in a Roth IRA so you pay zero capital gains taxes?

Reason 2: Diversification

Sometimes less is more

It’s important to be diversified in non-correlated assets. If I owned no gold, it would be important to own some, as gold tends to be less correlated with stocks and bonds. However, for the same reasons why you don’t want to be all in one asset class, you don’t want have too much of your assets tied up in gold.

If all you own is gold you don’t own any silver! Some speculate that silver will go up in value even higher than gold. If that’s the case you’ll want to diversity your precious metal holdings into the gray metal as well.

Reason 3: Liquidity

If you’re like most people, you need to buy food, clothing, energy, and the staples of living. You want to have some money in a more liquid format so you can pay for these things. If all your money was in gold, how are you going to pay your taxes or buy food?

Reason 4: No Cash Flow

If you invest in a business or a rental property or a dividend paying stock, there is cash-flow. If you own shares of a company, that company has employees trying to grow the business and increase shareholder value. Gold doesn’t do anything of those things. This is okay, gold doesn’t need to do those things (which come with their own set of risks), but if all your money is in gold then you are by definition missing out on opportunities to invest in cash-flow producing assets.

Reason 5: Charity

Wealth is a good servant but a terrible master. Ultimately you can’t take your gold with you and one of the great perks of having extra money (or wealth) is giving it away to those in need!

Do you want to gift your gold to a charity and have them have to deal with selling it?

If you keep some money in local currency it is easier to donate to a good cause. My favorite charitable organization is Children of Hope and Faith they help feed, clothe and educate orphans in Tanzania. I know the founder and board members personally and I know they have very low overhead which means it is efficient and there is more money going to the kids who need it. You can’t get any better than that!

Over the past few weeks I’ve been writing about the faulty wiring in the United States economy that will eventually result in an Economic Conflagration.

The faulty wiring that will ultimately lead to this economic firestorm includes the fact that the real economy is weak, the economy is crushed by profligate debt and that stocks are overpriced and due for a significant crash.

One of the reasons why candidates such as Bernie Sanders and Donald Trump were popular in the last United States presidential primary and general election is because people know that the real economy is weak. They know how much debt they have and they want someone to make radical changes and do something about it.

Unfortunately government has never been particularly good at creating wealth or prosperity.

Some people might choose to rely on politicians to fix things. This website is not for those people. HowIGrowMyWealth.com is for people who want to take some common sense steps to grow and protect their wealth.

Given the faulty wiring the economy it is more important than ever to grow and protect one’s wealth. It might take a while but this faulty wiring will eventually result in a fire that will burn uncontrollably.

I realize this isn’t necessarily very cheery stuff but fear not! There is plenty of room for optimism.

I’m not a doomsday “prepper” or perma-bear and I’m sure that entrepreneurs, if free to do so, will rebuild the economy and usher in greater prosperity that will not be funneled to the politically connected.

I’m also cognizant that the stock market has gone up nearly 300% since the great recession, there hasn’t been hyperinflation in consumer prices and on the surface the crisis seems to have passed long ago. I don’t have a crystal ball and being right early sometimes looks like being wrong.

Despite the relative calm there is faulty wiring in the economy and sooner or later it will spark and ignite blaze that will, to quote Peter Schiff, “will make the financial crisis of 2008 look like a Sunday school picnic.”

The politicians, if they even realize that there are systemic problems in the economy, simply aren’t willing to endure the short term pain and inconvenience of ripping out the faulty wiring in order to fix the underlying problems. So they will continue to kick the can until the economic house burns down.

The bright side is that this will present an opportunity to rebuild the economy based on a strong foundation as opposed to what we have now, a phony economy based on debt, cheap money and consumption.

There will be winner and losers. I’m very optimistic about the future and I want to be counted amongst the winners.

So where am I putting my money?

My asset allocation falls into three main areas. Value stocks, gold and cash.

Value Stocks

Most people love buying things on sale and getting a great deal, expect when it comes to investing. When it comes to investing people want to buy expensive things and hope they go higher. Value investing takes that same common sense, buying things when they’re on sale and applies it to stocks and other asset classes.

The stock market as a whole is overvalued by a variety of metrics. But there are still good deals out there especially in non-US markets. I don’t doubt that value stocks will also go down in the event of a stock market crash but I think they will go down less and they will recover with more strength.

I share my value stock picks publicly. But I only share if I would buy them today or if I would hold or add to my positions with members of my free email newsletter. I will also let me email subscribers know when I buy or sell a stock first, before I publish that information to this website.

Gold

I don’t think you will get rich buying gold but it could prevent you from getting poor. Under relatively normal circumstances the demand for gold is fairly steady and the supply is fairly steady so for the most part the price of gold will rise with the level of inflation.

Gold is a way to save purchasing power. It’s a way to opt out of the financial system and wait for sanity to return.

If the dollar tanks loses it’s reserve currency status gold will still be valued.

I also think there has been significant effort to suppress the price of gold and depending on how much downward price manipulation there really has been, the price of gold could go up significantly from where it is right now.

If fiat currencies collapse that could very well induce a flight to the safe haven asset of gold that this influx of demand would be very bullish for gold.

Because of the absurd expansion in central bank balance sheets and artificially low interest rates I like gold presents a fantastic value at current prices.

What I write about gold applies to silver–another asset I think will do very well in a downturn. Silver has the added benefit of being an industrial metal that is more widely consumed.

Cash

Long term, like every other fiat currency, I think the dollar will go to zero. So why would I want to hold dollars?

First, I own a month or two of expenses in physical cash in a secure location in case there are capital controls. If there is a panic and people start withdrawing money from the banks the banks might in turn say, you can only withdraw $500 a week or something like that. Withdrawal limits could also be imposed if the US implements negative interest rates and people (very rationally) decide it is better to hold dollars in physical cash so they don’t have to pay interest to their bank for the privilege of loaning their money to the bank.

I reside in the United States and everything is priced in dollars so I need dollars to buy things. If I lived in the eurozone I would hold pounds or euros, if I lived in China I would hold Yuan. If I lived in the socialist paradise of Venezuela I would probably hold dollars (and try to get out).

Secondly, apart from physical cash I also hold dollars in a money market fund as a war chest. If stocks tank I expect there will be bargains to be had. I want to be buying stocks (if they are high quality free cashflow producing companies) when everyone is panicking and selling.

Now I fully expect the United States Federal Reserve to do what it has done in all other crises it has created–it will lower interest rates and buy assets to prop up the markets.

With interest rates already low once they cut rates to zero they will only be able to do things like Quantitative Easing and Negative rates. This is very bearish for the dollar and very bullish for gold.

But in the highly unlikely chance the US Federal Reserve does the right thing and lets the stock market collapse and lets the US government default on it’s debts this could be very bullish for the dollar. So holding some dollars is a hedge against deflation as well as a war chest to draw upon to buy undervalued stocks post crash.

What are some other possibilities?

While the bulk of my holdings are in cash, value stocks and precious metals I also dabble in some other alternative investments.

If there is a dollar crisis or collapse in the faith of central bankers then more people could turn to cryptocurrencies and could see it rise. Demand for cryptocurrencies could also rise for other reasons pushing the price upwards.

While I think blockchain technology is here to stay the value of any one specific cryptocurrency or token could very easily tank to nothing. Cryptocurrencies are very risky and 90% swings (both directions) happen.

You need to have an iron stomach but having between 1-5% of your liquid net work in cryptocurrencies isn’t the most outlandish idea in the world.

I would only speculate on cryptocurrencies with what you can afford to lose and I don’t considering buying cryptocurrencies investing in a technical sense since I am simply betting on the price going up.

I’ve shared with my readers my Group of Six cryptocurrencies that I’ve chosen to own and speculate on.

Options

Net I’ve actually lost money trading options. I traded options while unemployed and failed to remain dispassionate and objective. I was so focused on making money that I opened positions when the conditions were not ideal and took risks I should not have been taking.

I do believe if you are disciplined and follow the appropriate rules, you can do well trading options.

During a stock market crash volatility spikes and selling options could be a good strategy. When the VIX (a volatility index) spiked up in early February I sold a few options and those positions are doing well as volatility has dropped and the market has recovered. Markets don’t move straight up or down for very long so even if the February selloff portends drops to come, the market doesn’t drop as fast as people think in the midst of the drop.

Real Estate

Unlike all the other assets mentioned above I do not and never have owned any real estate.

Lots of people have made lots of money in real estate. I am working to learn more about this asset class and hope to own my own rental property at some point.

What I like about real estate is that it is easy to use leverage and the tax benefits are ridiculous. You can effectively pay no tax on investment property income and borrow a lot of the money you need to get started.

You of course need to know what you’re doing.

My goals for owning real estate involve owning a multi-family apartment building. The key for me is a cashflow positive property. I don’t have any interest in trying to buy and flip, although some people are very successful doing this. There are lots of ways to make money in real estate and I recommend biggerpockets.com to learn about them.

I think cashflow positive real estate will do okay in the event of a crash. If you’re in an area that has stable employment prospects those workers will always need a place to live and have the money to pay for it. Of course real estate won’t “always go up” and there are a lot of risks and headaches associated with managing property (if you don’t outsource property management).

This is part 5 of 5 of what I’ve decided to term The Economic Conflagration series where I discuss the faulty wiring pervasive the global economy:

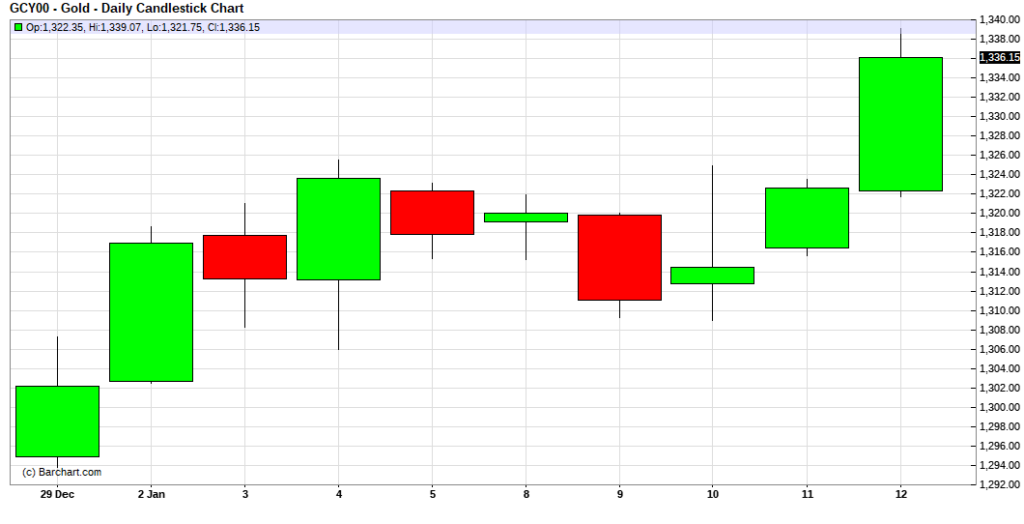

A 2.6% rise in the price of gold doesn’t seem like a lot given the tremendous volatility of cryptocurrencies like Bitcoin which can go up or down 30% in a day. Twenty eighteen has started off strong for the yellow metal. While gold has lost some if it’s shine in the eyes of many since the drop from it’s highs in 2011 it remains the standard in wealth preservation as far as I’m concerned. I am as bullish on gold today as I ever have been. Perhaps not in the medium term, but in the short and long term I think gold will be rising in USD price.

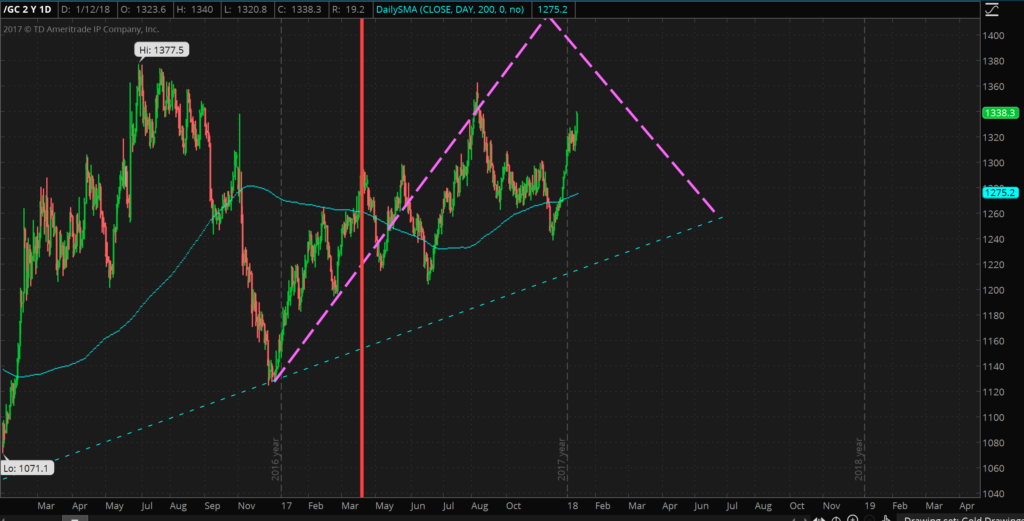

I posited back in April 2017 that 2016 was the start of a new bull market in gold and that trend has continued.

The dashed purple line indicates my prediction/guess as to the price movement of gold. This prediction was made back in the middle of April, 2017 (indicated by the vertical red line).

While this prediction looked fairly close up through August 2017, gold has since diverged quite a bit. Because gold hasn’t been able to take out the previous high of $1377.5 made back in July 2016, this bull market is looking fairly weak from a technical perspective, especially compared to the 2008-2011 bull market. This is why I think gold looks weak in the medium term (say 6 months to a year). In the short term gold is looking good, as previously mentioned gold is up over 2.5% this year.

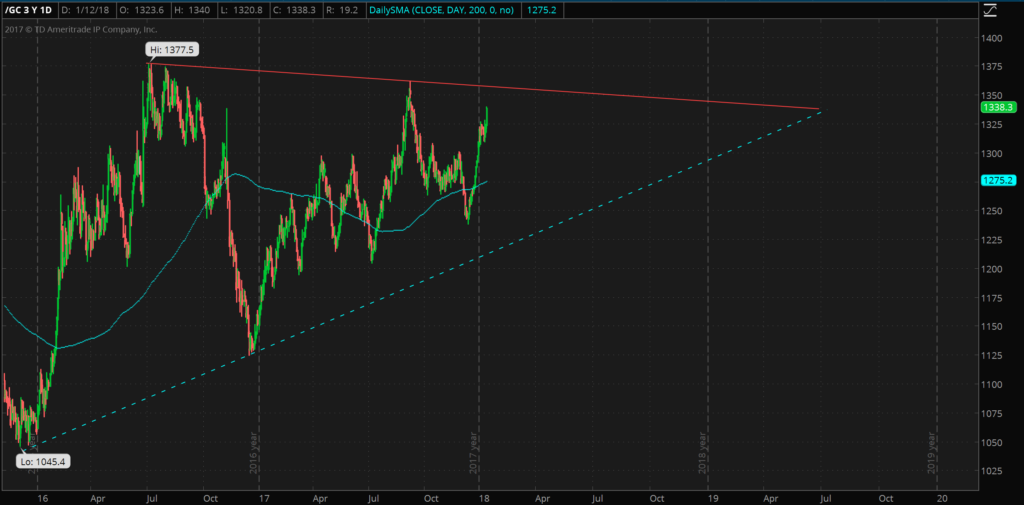

But even if the technicals of gold look weak the fundamentals of gold are still extremely strong. I think there is little chance that we will see gold available at a price of 1045 USD ever again and I think gold will eventually make new highs in excess of $2,000. I do think gold is in a bull market, albeit a weak one. A US War with North Korea, a Trump impeachment, another large scale terrorist attack, or any number of other catalysts could easily send gold upwards.

While we might have to wait until 2019, it will be interesting to see if gold breaks through the resistance (solid red line) and if so if it makes a new high above 1377.5, or if it goes back to test the longer term support levels drawn in a dashed blue line. Of course it could even do both if we see a lot of volatility.

I feel confident that gold will be above $1300. Regardless I think holding between 10%-25% of one’s assets in physical precious metals is a wise move. Go closer to 10% if you have faith in the US.gov and legacy financial system and closer towards 25% if you are a little more bearish on the US governments ability to handle the national debt, pension, social security and medicare funding crises. Of course all of these precious metal allocation percentages are just opinions and don’t take into account your age, goals and risk tolerance. If I had a lot of money in cashflow positive real estate or a successful and recession resistant business then I probably wouldn’t put as much into gold.

But if my income came from stocks and my job I would want to have 10-25% of my assets in precious metals and I would want to have some money in foreign stocks. I don’t think betting on the dollar is wise, it hasn’t been since 1913 and I think the dollar will only continue to weaken and at an accelerated pace.

While there is no substitute for physical precious metals like gold and silver held in a secure location one controls I think Goldmoney is a fast, easy and secure way to own physical precious metals. When you sign up for a Goldmoney holding account be sure to use my referral code: howigrowmywealth. A Goldmoney holding account allows you to store physical gold throughout the world in secure jurisdictions like Singapore and Switzerland. I personally own over $1,000 worth of gold through Goldmoney.

I like value investing and value stocks. It’s not some aesthetic or subjective reason. As an asset class US value stocks have a history of outperforming other US stock classes.

I like picking individual stocks but I appreciate that is not suitable for everyone. For some folks a passive index asset allocation strategy could be better.

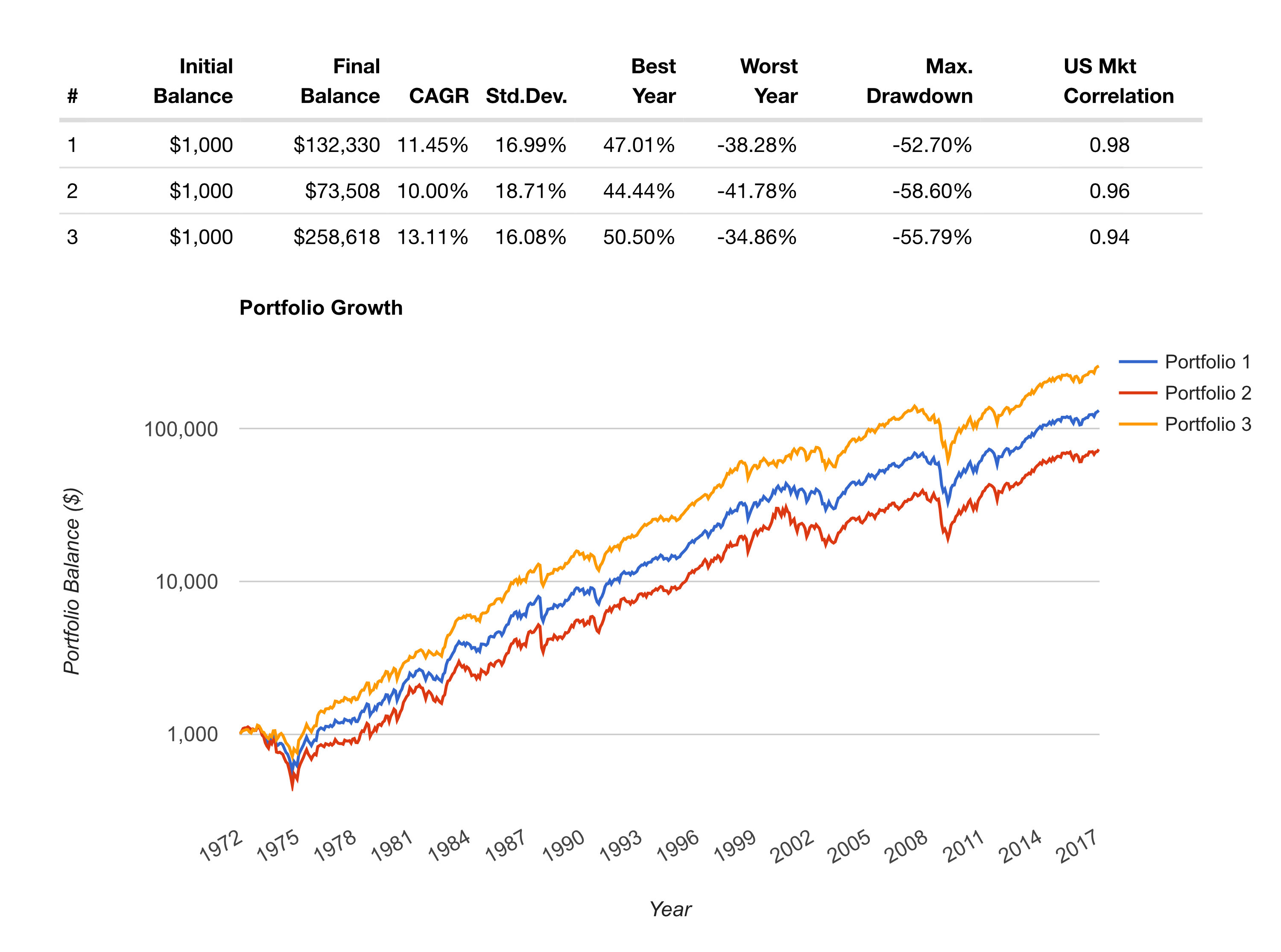

Equally Weighted Large, Mid, and Small Cap Portfolio Performance Since 1972

If one were to have invested $1,000 in the a portfolio consisting of roughly equal allocations of large market capitalization (“Large Cap”) stocks, mid-cap and small cap stocks in January of 1972, it would have grown to $132,330 by January of 2017. The compound annual growth rate (CAGR) of this portfolio was 11.45%. The maximum drawdown around the 2008 financial crisis was 52.70% (stressful).

During this same time, if one were to invest $1,000 in “US Stocks” the CAGR would have been 10.21%, balance on January 2017 would have been $80,008, and the maximum drawdown would have been 50.89%.

Source: portfoliovisualizer.com

What about Growth Stocks?

A portfolio with 1/3 large, 1/3 mid and 1/3 small cap growth stocks would have done even worse than the allocation above. The CAGR since 1972 has been 10%, the maximum drawdown was 58.6% (wow!), and $1,000 would have grown to $73,508.

So growth stocks performed worse.

Source: portfoliovisualizer.com

US Value Stocks have Outperformed

US value stocks have outperformed growth stocks. A portfolio mixed with 1/3 large cap value, 1/3 mid cap value and 1/3 small cap value would have a CAGR of 13.11%.

A $1,000 investment in 1972 would have grown to $258,618. The maximum drawdown would have been slightly higher than straight market cap stocks, at 55.79% (still stressful) but less than the growth stock portfolio.

Source: portfoliovisualizer.com

What it All Means

There are two main takeaways.

Value stocks outperform other stocks classes

A small increase in the CAGR has a large impact if the time horizon is long enough

US value stocks had a lower maximum drawdown than growth stocks

US value stocks have higher maximum drawdown than stocks in general

Source: portfoliovisualizer.com

For more details on this data see the portfoliovisualizer.com FAQ.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.