I was having coffee with some new acquittances a few weeks back and mentioned I run a blog website about personal finance. I was asked a very good question which I don’t think I answered very well!

The question was: “Where do I start?”

I’ve been saving and investing for a long time and thus far this website has often focused on alternative and more aggressive investment strategies.

I can appreciate it’s hard (and likely unwise) to jump right into advanced investing so I want to write what I think are some things to consider when just getting started in the world of personal finance.

I originally wrote this as one big article. But realized it was too much! So I broke it down into three digestible parts. Today is Part I: Stabilization

Disclaimer: I don’t give financial advice. One of the reasons I don’t give investment advice here on my website is because there are exceptions to many rules and your personal situation could merit additional considerations. What is suitable for me might not be suitable for you.

Basic Principles about Personal Finance

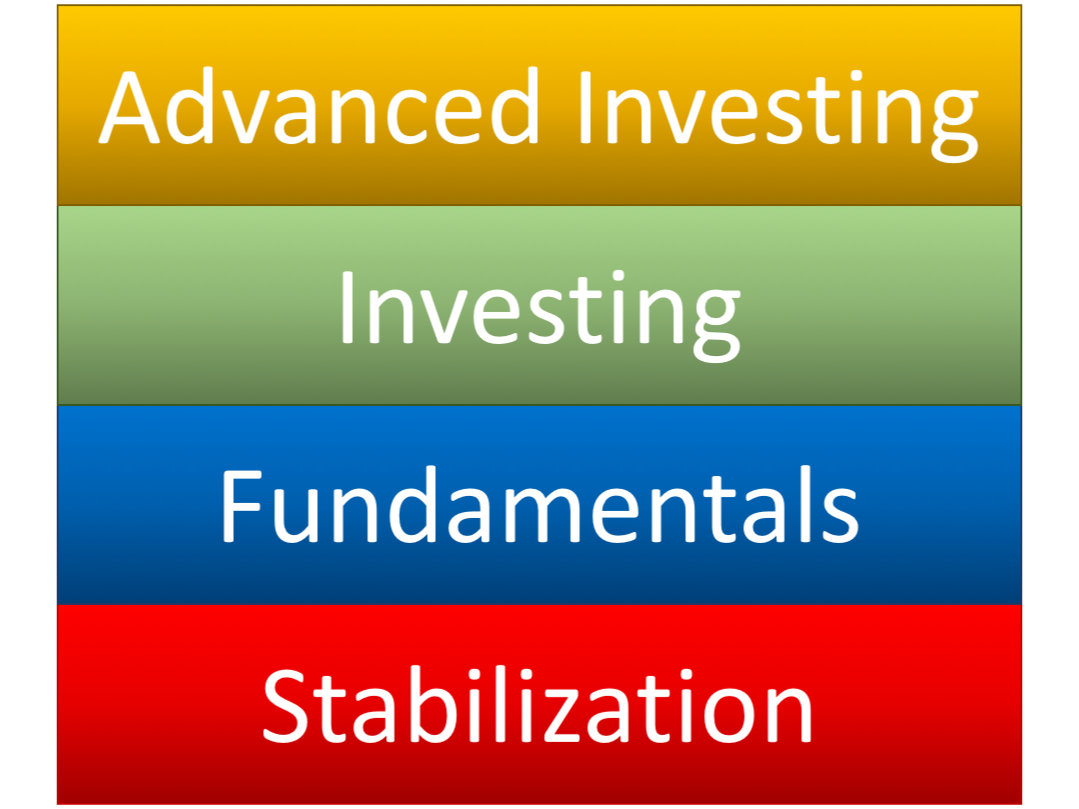

The Building Blocks of Personal Finance

I visualize these principles like building blocks. You have to have the lower levels in place before you can move to the upper levels.

Here are the basic principles:

– Debt for consumption is bad (Stabilization)

– You must produce and save more than you consume (Fundamentals)

– Have your money work for you (Investing and Advanced Investing)

The first level: Stabilization

In the health and medical field it is wise to make sure that a patient is stable and healthy before they try to fix some less pressing long term issue.

If an out of shape person is hemorrhaging blood due to an injury it would be absurd to focus on ways to improve their cardiovascular fitness until they are stable and healed from their injury.

If an out of shape person is hemorrhaging blood due to an injury it would be absurd to focus on ways to improve their cardiovascular fitness until they are stable and healed from their injury.

The first step on the path to growing your wealth is to stabilize your financial situation.

These things don’t make you rich but they stop you from getting poorer.

One of the great financial traumas to an individual’s finances is bad debt. This bad debt must be controlled before any other steps can be taken.

Stop Adding Bad Debt!

Bad debt is when you borrow money (usually at higher interest rates) to buy something that goes down in value and produces no income.

Examples of bad debt:

– Credit card debt (if you don’t pay it off every month)

– Auto loans

– Payday and title loans

Stop racking up bad debt!

$5 per day on coffee is $150 a month and $1800 per year

Stop buying things you don’t need via debt! Downgrade or cancel your cable plan. Stop buying $10 lattes. Stop eating out as much (I’m really bad at this one!).

If you live in a swanky single apartment maybe you could bring on roommates, downsize, or some combination of both.

Don’t buy a a new car every 2 years. Buy a used car you can afford.

If it doesn’t involve clothing your naked body, providing shelter, eating, or isn’t required for your job, consider cutting it out.

Yeah, this is no fun, but it pays off in the longer term.

If you don’t address your bad debt, its like having an uncontrollable bleed and wanting to start training for a marathon. You must stop the bleeding and get stabilized before you can start training for a race.

Next up Part II: Fundamentals

In Part II I discuss the importance of a budget and setting goals. Not only will this help you get and stay out of the stabilization level, but will help you save more than you spend and prepare you for level III: Investing.

Great advice! I am in the dundamentals/early investing stages – I lucked out by being naturally frugal and never racked up any bad debt – in fact I’m debt free! It allows me to live a moderately luxurious lifestyle (by many standards) on a mediocre salary, and still save every month! Thanks again 🙂

I’m glad you enjoyed the article. It sounds like you’re starting from a great foundation already. If I could go back and give myself advice about investing, I would say the first most important thing is to conserve principal (don’t lose money), second is to beat inflation, only third is growth.

You’re welcome and thanks for reading! I’ll definitely check out frugaltricks.com.