I favor gold over Bitcoin as a long-term store of value. I do think that blockchain technology is here to stay for a long time. However, I question the long-term viability of Bitcoin.

But before I get into that I want to say that if someone loves Bitcoin and hates gold they are free to own Bitcoin and no one will force them to own a single gram of gold! The opposite is also true. You can also own some combination of both!

For me, I’ve chosen to own much more Gold than Bitcoin but I still own both.

I do think having a very small percentage of my assets in crypto currency is appropriate for me but I’m leery of having too much of my net worth in cryptocurrency.

So with that in mind I present gold versus Bitcoin. This is a comparison between the two as I think of it. What you value or find important will likely be different.

That is the great thing about free markets: there doesn’t have to be one answer that is forced on everyone.

What I like about Bitcoin

International Value Transfer

I think BTC beats everything else out there for international value transfer. I’ve done international wire transfers and domestic wire transfers in traditional government fiat currency and Bitcoin is faster, easier and cheaper than anything else I’ve used.

Bitcoin has Advantages over Fiat Money

Dollars (and other fiat money) are constantly being devalued and destroyed via fractional reserve banking and central bank debt monetization and money “printing”. The total number of Bitcoins that will ever exist is set by how the bitcoin algorithm is coded.

What I don’t like about Bitcoin

It is Centrally Controlled

A disillusioned insider I came in contact with has swayed me to the opinion that Bitcoin is not decentralised. The decisions about Bitcoin are made by the Bitcoin Foundation and a few of the larger miners.

Bitcoin evangelists will tout Bitcoin as being decentralised. I’m open to new arguments and evidence supporting that Bitcoin is in fact decentralised but as of now I see Bitcoin as being centrally controlled.

It’s Direct-Use Value is Very Low

Some people argue that there is direct-use value in Bitcoin. It can be used as an experiment, political statement, etc. Others argue that Bitcoin has no direct-use value.

Even if Bitcoin is valued for direct use I think that value is very low. Dollars have some direct use value as well, for example kindling, tacky wallpaper, etc, but it is a fraction of the value dollars currently command in trade.

The reason I think this is a problem is because the direct-use value (aka non-monetary use value which is also sometimes called “intrinsic value”) provides a floor.

Government fiat currencies and Bitcoin have little (or zero) direct-use. So when these mediums of exchange fall out of favor, they can go to zero or near zero.

Bitcoin Could be Replaced by a Better Cryptocurrency

Bitcoin has some issues in my opinion. Bitcoin could be improved to overcome those issues, but it is also possible one of the myriad of alternative coins (called “altcoins”) could become more popular than Bitcoin and eventually replace what is currently the most established and largest cryptocurrency.

Delay in Confirmations

Virtually all vendors require a certain number of confirmations after Bitcoin is sent before it is confirmed and is considered successfully sent. This is to avoid the problem of double-spending.

Bitcoin takes about 10 minutes per confirmation. In the world of the internet, 10 minutes is a long time. Some vendors require 2 or 3 confirmations, which would take between 20-30 minutes. That is a really long time.

There are probably other reasons that haven’t even been invented yet that could make some new Bettercoin™ a superior choice to Bitcoin.

So while the number of Bitcoins is fixed the number of competing altcoins is not fixed.

Competing altcoins can serve to devalue Bitcoin. I like it when companies compete for my business to lower price but if I owned $1,000 worth of Bitcoin and then BetterCoin™ comes out and everyone switches to it, my $1,000 worth of Bitcoin could drop to a small fraction of a dollar in value.

The United States Commodities Futures Trading Commission (CFTC) declared Bitcoin is a commodity

Which means it’s taxable as a commodity.

Just because the government decrees that something is the case doesn’t mean that it is true.

Various elements of the US government can say that dollars are a store of value but that doesn’t mean they are.

I can disagree with the CFTC intellectually. But I obviously can’t ignore what the government says if I don’t want to get fined or go to jail.

Like most Americans I’m afraid of the Internal Revenue Service (IRS) so compliance with all appropriate tax laws is very important to me.

That means that every time I transact in Bitcoin I have to keep track of my cost basis and pay any appropriate capital gains.

Security

Mt. Gox, Bitfinex, and countless other exchanges have been hacked. You have to be kinda savvy to secure your Bitcoins. Plus, if you go the cold storage route you lose may of the benefits of Bitcoin as a medium of exchange.

What I don’t like about Gold

Gold isn’t used as Money or a Medium of Exchange

Few if any retailers will accept gold as payment for goods and services. One must first convert the gold into money and then spend the money.

Gold is not considered a currency and like Bitcoin does not get favorable tax treatment.

It could be Confiscated

The United States government has made gold bullion ownership illegal in the past and could do so again. Therefore any gold held in the US is susceptible to confiscation. I think it is unlikely this will happen again because not very many people own gold bullion, as compared to years past, but this is a possibility.

You Can’t use it to Buy Stuff Online

I can’t get onto Overstock.com and use physical gold in my possession to buy goods or services. What that would look like would be to mail in a shipment of gold, Overstock would wait until the gold arrives, and then ship out what I ordered.

I think the Paper Gold Markets are Manipulated

I think governments have a vested interest in keeping the price of gold down. I think the gold futures markets are manipulated down. While I think that this manipulation is not sustainable and eventually the price of gold will reflect supply and demand fundamentals, it is annoying in the short term. On the flip side, gold manipulation does provide a lot of great buying opportunities.

What I like about Gold

It’s Been Valued for 3,000 years

Despite all the changes since 1,000 B.C. gold is still valued by billions of people.

It has Significant Direct-Use Value

Gold is used in electronics, jewelry, dentistry, satellites, and decoration. Even though gold is not used as money or a medium of exchange today it is still valued by billions of people.

How many people would want US dollars if they weren’t used as money?

Gold is a Natural Element that Satisfies the Classical Requirements of Money

Gold is one of the least reactive chemical elements. Gold that has been lost on the ocean floor for hundreds of years is still in the same shape it was when the ship went down.

Gold is durable, portable, scare, divisible and uniform. Gold can act as a unit of account, a medium of exchange and a store of value.

Gold is Scarce

A new element that has all the properties of gold is unlikely to be discovered or created.

New gold can only be created in a nuclear reaction and gold can only be pulled out of the ground with significant effort and time.

Mining gold-rich asteroids would also be tremendously expensive and dangerous.

Gold can be used with Payment Technologies

Much of the below thought is from or inspired by Roy Sebag. Mr. Sebag makes a distinction between money technologies and payment technologies.

Money Technologies

Dollars and Euros are debt-based, fiat money technologies or assets that can act as a store of value (albeit poor stores). Gold is an asset that can act as a store of value. Bitcoins are an asset that can act as a store of value.

Payment Technologies

Credit card networks, Paypal, Apple Pay, Bitcoin, and Ether are examples of payment technologies. These are networks and systems that allow ownership of assets to be transferred.

Buying things online with a credit or debit card, Goldmoney, Paypal, or Bitcoin is simply ownership transfer of an asset via a payment technology.

In the case of credit cards, the credit card network is the payment technology and dollars are the money “technology” or asset being transferred.

In the case of Bitcoin, the Bitcoin blockchain is the payment technology which also has an integrated and inseparable unit of account, also called Bitcoins.

Gold can be used separately from a payment system (physically exchanged), or it could be used in conjunction with another payment system.

Goldmoney is one such service that combines physical gold ownership storage and transfer with the payment technology potential of internet based transactions.

Gold remains a fantastic store of value. I think the best of both worlds in money would be a gold-backed currency or electronic ownership transfer of Gold held at a trusted third party.

In Conclusion

Bitcoin has a very low (if any) direct-use value. That fact combined with the potential for Bitcoin to be supplanted by a superior payment technology makes me skeptical of Bitcoin as a long-term store of value.

I like gold because it has a 3,000 year history of being valued across cultures. It’s scarce and I think it’s extremely unlikely that another element will come along that will be able to replace the desired and historically valued properties of gold.

Not only that, but you can still make payments and spend gold in a way that takes advantage of the electronic payment systems that are so useful today.

Ultimately investors and consumers will make their own decisions. Gold and Bitcoin are competitors but they could also continue to exist side by side for some time.

That is just how gold and Bitcoin compare in my view. Which one do you prefer? Let me know in the comments section below!

I’m an advocate of holding gold. I think it is a key part of my portfolio but I own too much as a percentage of my other assets.

Datta Phuge

Not counting retirement-specific accounts, gold (and silver) make up 54% of my liquid net worth.

That is way too high for me!

So I decided to read what some public figures have said or written in regard to the percentage of a portfolio that should be gold (and silver).

The following is educational only and NOT SEC-investment-advice. So make up your own mind with the help of an appropriately licensed, registered, and SEC-anointed financial advisor.

Warren Buffett doesn’t like precious metals. He has several famous quotes regarding why he doesn’t like the shiny stuff. While I wouldn’t be surprised if he actually did own some precious metals, but the way he speaks he acts like he doesn’t own any. I’m not a Buffett fan but I think you can learn from him if you carefully sift what he does from what he says or writes.

Mad Money host Jim Cramer recommends no more than 10% in gold. He recommends owning gold via an ETF unless you have enough money to buy physical in bulk.

I’m not a Jim Cramer fan, but I include him because he is a big-time stock guy and yet he still recommends holding some gold. I think there is reason to believe the ETFs don’t hold the gold they claim to so I don’t like gold bullion ETFs. I also disagree that gold is just an insurance policy. Pure insurance (such as term or homeowners) is not an asset, it’s an expense. I think gold is an asset class in and of itself.

Peter Schiff – SchiffGold and EuroPacific Capital – 5-10%

Peter Schiff recommends 5-10% in physical gold. I was actually surprised by this low number because Schiff talks about gold and silver A LOT. Schiff’s 5-10% allocation to gold and silver does NOT include mining stocks–but that is a different topic.

Mike Maloney is the most pro-precious metals person I know of. He is 100% allocated to precious metals with 90% to silver American eagles and 10% to gold American eagles.

I would like physical precious metals to be around 10-25% of my liquid, non-retirement portfolio. I don’t have an opinion on the amount of silver relative to gold. I am of the opinion that silver is more undervalued than is gold and as a result has more upside potential.

I think gold and silver are a great way to preserve wealth but they are not a great way to build wealth since they don’t pay a dividend or yield. For many readers that might be obvious but I’m still learning!

I purchased a lot of gold in 2013, on the heals of the all-time highs, so much of my gold and silver holdings are worth less in fiat than I paid for them. So I intend to reduce my gold holdings as a percentage of my portfolio by focusing my savings and investments on other asset classes going forward. By doing this I can reduce my gold and silver holdings as a percentage of my assets without selling any of my gold and silver.

On the flip side, if my portfolio did have less than 5% physical gold I would consider adding to my holdings via gold maples, silver American eagles, and foreign-stored physical gold via a Goldmoney personal account held by a trusted and low cost custodian.

I would not buy US treasuries and I don’t understand why there is even a market for them.

I know the Federal Reserve is a big part of the “market”, officially and otherwise, but surely they aren’t 100% of the “market” (yet).

If the Fed isn’t 100% of the market that means someone besides the Fed is still buying treasuries.

I would like to talk to someone who is buying US treasuries and understand WHY they are doing so.

Reward-Free Risk

US debt yields are paltry. As of today the 10 year treasury has a 1.5% coupon. That means if I buy a $100, 10 year treasury, I’ll get $1.5 per year, in two $.75 payments and after ten years I’ll have gotten $15, plus the $100 face amount of the treasury.

Ten year treasuries are trading at a discount rate of $97.89 so if I hold the treasury to maturity, I could gain $17.11 ($1.5 per year times 10, plus $2.11 (difference between the bond price and face value)).

Price from Bloomberg: http://www.bloomberg.com/markets/rates-bonds/government-bonds/us

In other words if I were to purchase a 10 year treasury I’ve loaned the government $97.89 and ten years later the government pays me back $115. While $17.11 isn’t fantastic it looks positive.

The problem is price inflation.

The 2015 consumer price index (CPI) was 1.7%. So using a handy inflation calculator (link below), I know that $115 ten years from now has the same purchasing power as $97.16 in today’s dollars.

Basically, I would have loaned the government $97.89 and in ten years they pay me back with the purchasing power of $97.16.

I’ll have lost purchasing power!

When I loan someone money (unless I really like them) I should be compensated for not having access to those funds. I certainly don’t accept being paid back with less valuable money when I make an investment.

Personally, I don’t think the CPI is accurate. I think that price inflation is at least 2%, perhaps even as high as 10% per year. So let’s say prices are rising on average 5% per year.

With a 5% annual price inflation rate, that $97.89 is worth just $70.60 ten years from now, so the ten year treasury lost over $27 in present day purchasing power.

Compound Interest

If you reinvest the bond coupon payments (the $.75 you get every six months) you would start taking advantage of compound interest and the math works out a little better.

The calculations become much more complex but if I were to reinvest the coupon payments, best I can tell is the $97.89 would grow to around $135 after ten years. With a 5% inflation rate the $135 would be less than $83 in today’s dollars so it is still a loser investment. That assumes the 10 year continues to trade at the current price and the coupon stays the same for the treasuries purchased with the reinvested coupons.

If I were to reinvest the coupons and if inflation really was 1.7%, the $135 ten years from now would be around $114 in today’s dollars, so I will have gained purchasing power.

But as I said before I don’t think inflation is that low.

Short Term Treasuries are No Good Either

The 12 month treasury pays no coupon but sells at a discount such that it yields .64% upon maturity. With inflation at 1.7% it is another situation in which a buyer is guaranteed to lose purchasing power if the treasury is held to maturity.

The only way to gain real value with a treasury would be to sell the treasury for more than the purchase price by a wide enough margin to beat the rate of price inflation or to hope that there is significant price deflation.

The Federal Reserve will fight any price deflation that might occur so I don’t think that will work. I also think that bonds are in a bubble, so while right now there might be an ample source of greater fools willing to pay more for a bond than the last person, eventually the only greater fool will be the Fed.

Again, I don’t understand why any rational investor would loan money to the US government in exchange for being paid back with dollars that are less valuable later. It’s the opposite of how the time value of money is supposed to work and it isn’t sustainable.

It’s one of the reasons I think bonds are in a bubble. I’m not the only one who thinks that. Folks much smarter and experienced than I have been saying the same thing.

The takeaway for me is don’t buy US treasuries. They are reward-free risk and there is no place for them in my portfolio.

Disclaimer: The information on this site is provided for discussion and educational purposes only and should not be misconstrued as investment advice. Under no circumstances does this information represent a recommendation to buy or sell securities.

I share how I grow and protect my wealth and one way I do that is by owning gold and silver. Gold and silver have served as money and a store of value for thousands of years and are a key component of my portfolio.

Gold

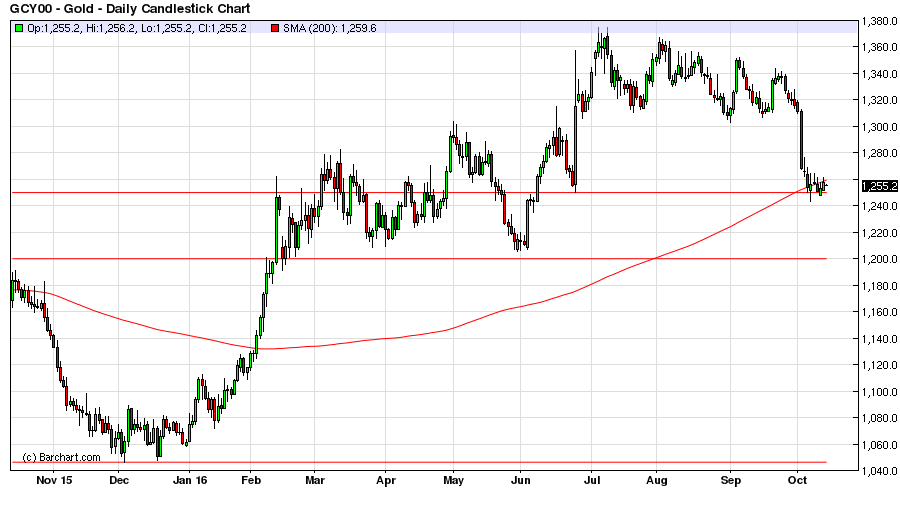

This year the yellow metal was as high as 1,370 dollars per ounce. But over the past few days the yellow metal has been pummeled and is now flitting about the mid $1,200s. It’s still up 17% on the year, having started down at $1,060.

The horizontal red lines are what I think are support levels. There was support at $1,310 but gold blew through that.

Could gold go lower? Sure could.

It’s certainly possible it goes back down to $1,200. But once the Fed does NOT raise rates in November, or even if they do and it’s only by a paltry .25%, I think gold has a lot more upside potential.

I personally think this is a golden buying opportunity. If I wasn’t already over-allocated to gold I would figure out how much free cash I have to allocate to gold. Then I would probably buy half now and then if gold does drop down to $1,200 buy the other half. If I had $3,000 to invest in gold I would buy physical bullion. With less than $3,000 I’d go with Goldmoney.

Goldmoney is a fantastic and low cost way to buy and store physical gold.

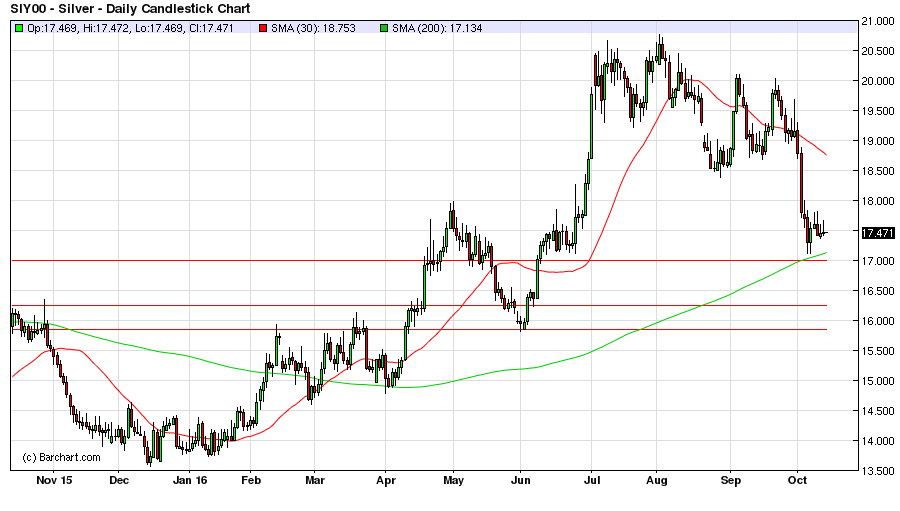

Silver

Silver is no slouch either. This metals used for electronics, industrial applications, jewelry and medicine is up over 23% year to date and the drop from the year highs of $20.75 down to $17 also presents a great buying opportunity in my opinion.

From a technical perspective $17 silver looks like a strong support level because it is the 30 day moving average and was a support (or resistance) level in April, May and June.

Waiting a few days to see if silver does break through the $17 support level or goes higher is a good idea. If silver does go down through $17 there could be support at the $16.25 level, but even stronger looking technical support appears at the $15.85 level.

The horizontal red lines are where I think the price of silver could find support. I think $17 could hold, but if not would likely retest $16.25 and/or $15.85.

Gold and silver are long term hedges against central bank recklessness and currency devaluation. I own these precious metals with a 5-10 year (or longer) outlook. I think a 10-20% allocation makes sense for my portfolio.

I’ve been wrong about gold and silver’s price moves plenty of times. I’m not encouraging anyone to go out and buy bullion without doing their own research and consulting their investment advisor.

Value investing is a way to bring intelligence back into stock selection.

Everyone loves a great deal when they’re shopping but for some reason that love does not transfer when shopping for stocks. Many retail investors tend to buy expensive stocks as they are getting more expensive.

They pile into trendy growth stocks like Twitter and Netflix.

It doesn’t make sense.

Making money in stocks can be done in just two ways:

1) buying low and selling high

2) dividends

Because many investors like to buy expensive stocks with no dividend the prevailing strategy has become “buy high, sell higher”.

This could work some of the time but if you buy stocks at all time highs (like many are now) who are you eventually going to sell them to? You’d have to find someone else who wants to buy them at an even higher price or sell them at a loss.

Buying overpriced stocks also leaves a person much more vulnerable during a stock market correction as was experienced by countless stock owners in 2000 and 2008.

An Intelligent Approach: Value Investing

Value investing takes that same desire to find a bargain while shopping and applies it to stock selection.

Value investing is purchasing the shares of quality companies trading at a discount.

In other words, you’re buying stock in a company that is undervalued. This creates a margin of safety and built-in downside protection. It’s a way of increasing the odds that you are buying a stock low so you can sell it higher later (or so you can hold it and collect the dividends).

Is Value Investing just buying Cheap Stocks?

Cheap lawn chairs tend to collapse when you’re sitting in them

If you’ve ever bought a cheap lawn chair you know first hand that you can overpay for something even when it doesn’t cost a lot of money. Stocks are no different.

Value investing isn’t buying cheap stocks. Value investing is buying high quality companies at a price below their book value.

You can find a deal on a high quality lawn chair and pay less than you would for a lower quality, more expensive lawn chair. The key to spotting a bargain is to know what to look for. Fortunately, there are a number of indicators (or metrics) one can look at to determine if a stock is both low cost and high quality.

What indicates a stock is a Great Value?

[Note from John, 5 Feb 2017: While the principles of value investing are timeless I have since started looking at Better Metrics for Value Investing.]

The metrics I look at are as follows:

Price to book of less than 1 (can go up to a PB of 1.5)

Price to earnings less than 15

Positive Cashflow

Positive Earnings per share

Return on equity greater than 8% on average per year

Dividend Yield

I’ll break down each one below.

Price to Book

The Price to Book ratio is calculated by taking the companies’ market capitalization and dividing it by the companies’ total assets minus total liabilities. A low price to book could indicate that a stock is undervalued.

If the P/B is below 1 that means if the company’s assets were liquidated and the stockholders were paid out in cash they would get more than what they paid for the stock.

Price to Earnings

The historical average for the stock price to earnings ratio is 15. The current PE ratio for the S&P 500 is around 25. By purchasing stocks with a PE less than 15, you’re ensuring the company’s price to earnings is below the historical average. It’s another indicator of value.

Source: http://www.multpl.com/

Positive Cashflow and Earnings per Share

A low price to book by itself could indicate that a stock is undervalued or that the company is on shaky ground. Positive cashflow and positive earnings per share means that the company is making money. The higher the EPS the better all else given.

Return on Equity

A return on equity of 8% or more over a period of years indicates the company consistently produces value to shareholders. It’s another way to ensure the company is healthy and is not undervalued due to a fundamental issue with the performance of the business.

Dividend Yield

This is the second way to make money on a stock. If a company provides a yield that means the investor is being compensated for holding the stock while waiting for the undervalued equity to revert to a more fair valuation.

Does Value Investing Work?

Value investing was pioneered by Benjamin Graham. You may never have heard of Benjamin Graham but it’s likely you’ve heard of Graham’s most successful student, Warren Buffett.

The investing principles Buffett used to grow his wealth were developed and taught by Benjamin Graham, the father of value investing.

Value investing is the way Warren Buffett became one of the richest men alive.

Getting Started in Value Investing

You can look for stocks that meet the criteria I’ve discussed above and purchase them individually.

Another option is to buy a value index fund. A a passive index fund takes little research and is theoretically lower risk.

An example of such a fund is the Vanguard Value Index Fund (VIVAX). The problem I have with funds like this is that the stocks in the fund aren’t the best values. For example, the largest holding in VIVAX is Microsoft (MSFT).

MSFT has a price to book of 6.2 and a price to earnings of 27.4. The other major holdings of VIVAX like Exxon Mobil and GE follow a similar story.

Microsoft and Exxon are quality companies but at these prices they don’t represent the extremely high value stocks I’m interested in.

Value investing like all investing is not without risk. But I believe taking the time to research undervalued stocks that present exceptional value is worth it.

Intelligent Research on Value Stocks

For a passive and defensive investor, value investing through index funds is fine. However, I believe an enterprising investor willing to dive deeper can make even better returns. But not everyone has the time or resources to research stocks that meet the criteria of a quality value stock.

I maintain a list of the stocks I like, access it fr-ee here.

Find An Edge

An Edge: a quality or factor that gives superiority over close rivals or competitors.

It’s hard to make money on stocks like Apple or Microsoft that have dozens of analysts following them, where virtually everything is known about the stocks, and which are traded at high frequency by Wall Street computer algorithms.

If you don’t know what your edge is you don’t have one.

I think value investing is a way for a smaller investor to gain an edge in what is sometimes a rigged game.

I also think that there are exceptional values outside of the standard US stock exchanges.

I’m particularly fond of the Australian Securities Exchange because it is outside the Wall Street bubble but still a stable jurisdiction. My free report lists two brokers that will allow you to trade stocks in the land down under.

Wisdom from Benjamin Graham

I close this article with a quote from the Father of Value Investing:

“…the real money in investment will have to be made–as most of it has been in the past–not out of buying and selling but of owning and holding securities, receiving interest and dividends and increases in value.” – Benjamin Graham from The Intelligent Investor

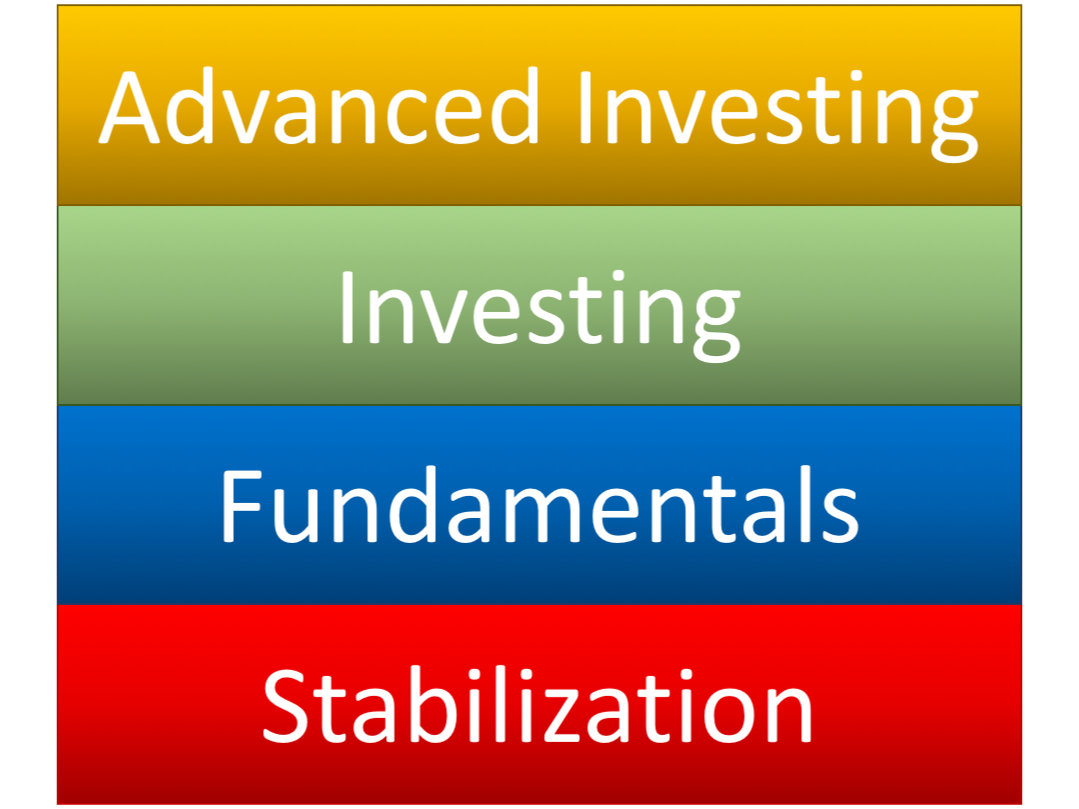

This article is Part III of my three part series of getting started in personal finance. Part I is Stabilization. Part II is Fundamentals. In Part III I discuss investing and advanced investing.

If you haven’t already read parts I and II start there!

I visualize personal finance as building blocks stacked on top of each other (shown to the right).

You must master the lower levels before you can get to the upper levels.

Level 3: Basic Investing

I consider basic investing saving for retirement in a 401k and Individual Retirement Account (IRA) via mutual funds and bonds, and general savings in mutual funds.

Both the 401k and IRA are ways to invest for retirement and get some tax benefits. 401ks are through an employer, and IRAs can be setup through a company like Vanguard, Fidelity, TD Ameritrade, or any number of other firms that act as the “custodian”. I talk about them in a little more detail in my article Five Tax Strategies to Keep More Income under strategies one and two.

Employer Matching 401k

Some employers will match your 401k contributions. As an example lets say your employer matches your contributions up to 5% of your salary. If you make $50,000, and you save $2,500 in your 401k, your employer will add an additional $2,500 to your 401k. I put money in my 401k up to but not beyond the point where I’ve maxed out the match.

I prefer Roth 401ks to 401ks because I believe tax rates are going up in the future. Roth 401ks are more rare but I have had employers who offer them.

The vast majority of the investment options offered by the employers I’ve been at are VERY limited. The easiest option is to go with a target retirement fund. Target retirement funds are basically funds on autopilot, they automatically adjust their asset mixes to become more conservative as investors approach the target retirement date.

If there are more options I avoid bonds and favor international funds but investments depend on your risk tolerance and goals.

Individual Retirement Accounts

IRA’s come in the Roth and Traditional flavor. It all depends if you’d rather pay taxes now, or in retirement. I prefer to pay the taxes up front.

I would open up a Roth IRA and try to max it out ($5,500 in 2016). Another neat trick is that you can contribute to a traditional IRA and then convert contributes to a Roth (you do of course have to pay the taxes though), so if you want to save more than $5,500 in after tax income, that is an option.

One of the things I like about IRAs is that the investment options are much, much more flexible. I think part of the reason employer sponsored 401ks have such limited investment options is because employers are afraid of being sued if an employee makes poor decisions and loses a lot of money, so employers only offer with the most conservative investment options.

If you want to save money and not think about, you’re asking for trouble, but one option is to open up an account at a low cost company like Vanguard (my favorite) or Fidelity. Setup auto-deposit and buy a balanced fund like the Vanguard STAR fund (VGSTX).

You can also buy additional index funds, like the S&P 500 index fund, Nasdaq, large and small cap US funds, etc. These index mutual funds are setup to track the gains and losses of the index they are based on. Again, I think it is good to have money in the emerging markets as well.

Vanguard has investment professionals that will help you decide how to allocate money to different mutuals funds. (Disclosure: I have been a vanguard client for years, but gain no benefit from listing them as an option).

By setting up auto-deposit and auto-invest into Vanguard (or your IRA custodian of choice) from your paycheck you’re dollar cost averaging into the fund and not trying to time the market.

Over time this is a good, conservative strategy, and one discussed by Benjamin Graham in his seminal work “The Intelligent Investor”. Ben Graham was a mentor to Warren Buffet, who you may have heard of, and has done decently well as an investor.

Conventional wisdom is often something like a 40% bonds and 60% stocks (mutual funds) as a conservative approach. Unless you’re retired and relying on your savings for monthly income, I would not buy bonds, but a portfolio that does not include bonds is considered more risky.

You can follow these same investing principles to buy non-retirement mutual funds.

Now I do think that US stocks and bonds are in a bubble. But if the Federal Reserve responds to the bubble bursting as I think they will, stocks and bonds will still go up. I just think there are other asset classes that will go up faster.

Consider Physical Gold

While this could be considered more advanced, I think it is very important to have somewhere around 10% of one’s assets in physical gold and silver bullion. While I don’t give investment recommendations I think that even some of the more conservative and traditional investment advisors would admit this is not a bad idea. I gain no benefit from mentioning them, but I buy bullion from Scotsman Auction house in Saint Louis. They have been in business a long time and have great pricing. I don’t buy numismatics or “rare” coins as an investment. I’m partial to Silver American Eagles and Gold Canadian Maples, but that is just personal preference.

There are lots of gold bullion companies but I would not want to pay more than around 2% over spot price for gold. I avoid numismatics unless they can be acquired at bullion prices.

Level 4: Advanced Investing

Advanced Investing techniques are what I’m most passionate about. Examples of what I consider advanced investments are: Investing in individual company stocks, gold mining stocks, peer to peer lending, real estate investments, private equity, foreign stocks, offshore brokerage accounts, options, cryptocurrencies, physical precious metals like gold and silver, and physical gold stored remotely through a Goldmoney personal account.

These techniques are generally considered more risky, although I think that buying US stocks at all time highs and negative yielding bonds is much more risky, even though conventional foolishness wisdom says these are the safe bets.

Get Started!

To get started figure out where you stand in the four phases. Master that phase and work towards the next.

It’s an iterative process once you’re out of stabilization and focusing on the fundamentals and investing. I’m often re-evaluating my fundamentals such as my budget and my goals. I work on my basic investing like maxing out my 401k company match and Roth IRA.

Which phase are you in and what are your savings and investment goals?

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

Even if Bitcoin is valued for direct use I think that value is very low. Dollars have some direct use value as well, for example kindling, tacky wallpaper, etc, but it is a fraction of the value dollars currently command in trade.

Even if Bitcoin is valued for direct use I think that value is very low. Dollars have some direct use value as well, for example kindling, tacky wallpaper, etc, but it is a fraction of the value dollars currently command in trade.

Some employers will match your 401k contributions. As an example lets say your employer matches your contributions up to 5% of your salary. If you make $50,000, and you save $2,500 in your 401k, your employer will add an additional $2,500 to your 401k. I put money in my 401k up to but not beyond the point where I’ve maxed out the match.

Some employers will match your 401k contributions. As an example lets say your employer matches your contributions up to 5% of your salary. If you make $50,000, and you save $2,500 in your 401k, your employer will add an additional $2,500 to your 401k. I put money in my 401k up to but not beyond the point where I’ve maxed out the match.  Consider Physical Gold

Consider Physical Gold Advanced Investing techniques are what I’m most passionate about. Examples of what I consider advanced investments are: Investing in individual company stocks, gold mining stocks, peer to peer lending,

Advanced Investing techniques are what I’m most passionate about. Examples of what I consider advanced investments are: Investing in individual company stocks, gold mining stocks, peer to peer lending,