Within the past month or so online marketplace sites like eBay and Etsy started collecting sales taxes. This phenomena was a result of a flurry of states passing legislation targeting these types of sites. More states will inevitably follow.

I started noticing back in 2017 that more and more of my Amazon.com purchases have required the payment of sales taxes as well.

Source: https://en.wikipedia.org/wiki/Amazon_tax

But this recent scourge of legislation is tied to a 21 June 2018 supreme court case: South Dakota v. Wayfair, Inc. in which the court changed their mind about state’s ability to collect sales taxes on purchases from other states.

Online Sales Taxes are Bad for Consumers

These online sales taxes are just in time for the busy Christmas shopping season. Among the many benefits of online shopping was that it was normally sales-tax free. Tax savings are partially offset by having to pay for shipping. But in many cases, depending on the price, size and weight of the item being purchased, this was less than the taxes would have been.

Online sales taxes means unhappy consumers

There are fewer and fewer ways to shop online without paying sales taxes.

Online sales taxes are a regressive tax hike on the lower and middle classes who spend a higher percentage of their income on goods and services.

Sales Taxes Saps the Motivation of Producers

Never mind that the company making the sale pays taxes on their profits. Forget the buyer paying for the item is doing so with money on which they paid income taxes. These taxes aren’t enough for states that want to charge sales taxes as well.

There really is no limit to how big a slice of cake the government thinks they should get.

“Online sales taxes are a regressive tax hike on the lower and middle classes who spend a higher percentage of their income on goods and services.“

A person buying ingredients and spending time baking a cake ought to get the most benefit from that labor. At its most extreme, not being able to benefit from the fruits of one’s labor is slavery.

Most people enjoy having goods and services so it makes sense to live in a society that motivates and incentives people who produce to goods and services.

Societies that punish producers of goods and services tend not to have a lot of goods or services.

At a certain point people start to feel that the government is getting too much of the cake. A baker might decide they aren’t benefiting enough from their labor and they stop making cakes.

Bad for Small Business

One of the biggest burdens besides the consumer is the small seller. Companies like Amazon.com have entire legal and accounting teams that can navigate the myriad of state, federal, and local taxes.

Big conglomerates can afford systems that track how much is due based on the location of buyer and seller. Smaller players are less able to manage the complexity the number of tax jurisdictions an online seller would need to be responsible for.

All in all online sales taxes benefit the government and to some extent large businesses. Online sales taxes hurt smaller competitors who are less able to deal with managing tax collection on behalf of the government. It’s bad for consumers and small businesses.

Just One More Problem in the Economy

There were already numerous economic headwinds facing the United States and this is one more. While many States are essentially insolvent, Illinois being one of the worst offenders, it makes sense that they are desperate to increase money flowing into their coffers to offset the unsustainable promises they are obligated to pay out.

However, until there is real reform of government spending, increasing taxes will ultimately hurt the lower and middle class and shrink the economic pie being divided up, resulting in everyone being poorer.

One of my twitter followers “W.C. Varones” (I am one of his followers as well!) responded to my Roth versus pre-tax 401(k) article and purported a Roth 401(k) was better even if the tax rates are the same.

I initially balked at this since it defied what I’d been taught in school and even my own prior analysis.

But after crunching the numbers to disprove this argument I realized the following:

Even assuming the tax rates are the same at the time of the contributions and distributions there are more tax savings with a Roth because you aren’t getting taxed on your compounded gains.

Put another way, with a 401(k) the money is taxed after it has grown in a compound fashion. With a Roth the money is taxed before it goes through compound growth. So if you max out a Roth 401(k) you end up being able to save more compared to the same amount in a pre-tax account.

The Scenario

In 2019 if you aren’t eligible for the catch up provisions you can invest a maximum of $19,000 in a 401(k) (Roth, pre-tax or a mix of both).

Say there are three people each committed to saving $19,000 for retirement.

Person A the “Roth investor” chooses to contribute their $19,000 in a Roth 401(k). Person B the “pre-tax investor” contributes to a pre-tax 401(k). Person C the “non-retirement investor” who forgoes any tax-advantaged retirement account and saves for retirement in a brokerage account.

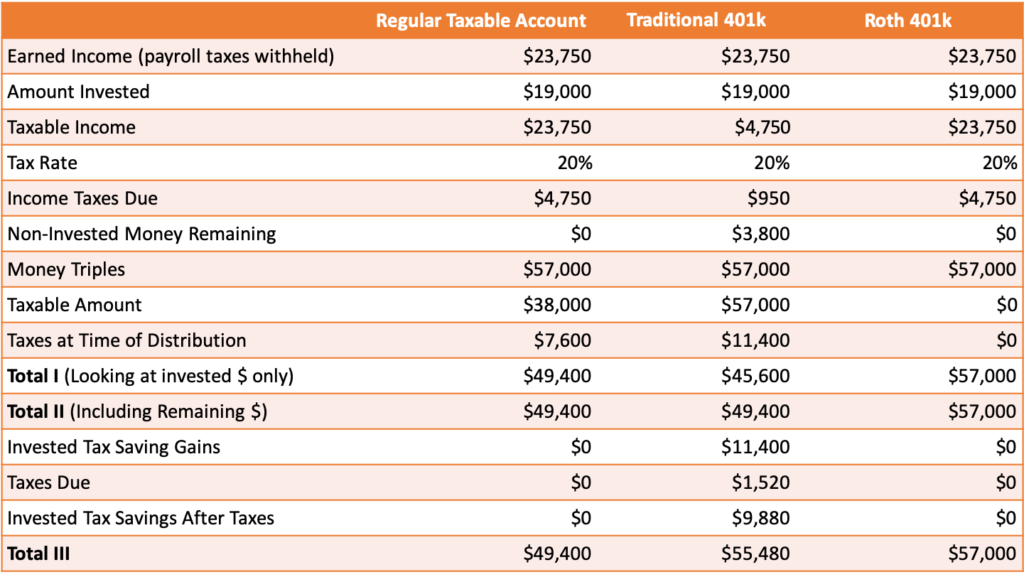

Because of taxes (we’ll assume a 20% tax bracket both now and in retirement) one needs to earn $23,750 worth of income in order to invest $19,000 .

Note: I’m excluding payroll taxes since they are always owned at the time the income is earned and add unnecessarily complexity that has no impact on the conclusion.

We’ll also assume the money triples between now and retirement. All other factors about these individuals are the same.

Total I: The Basic Scenario

Fast forward to retirement the Roth investor has $57,000 and owes uncle Sam nothing. The pre-tax investor also has $57,000 but they owe uncle Sam $11,400 in taxes, so in retirement they’d be left with just $45,600. See “Total I” below.

Interestingly the non-retirement account investor has more than the pre-tax investor ($49,400 versus $45,600). This is because they were able to count the $19,000 cost basis whereas the cost basis of a pre-tax 401(k) is zero.

So the Roth investor is the clear winner!

Total II: Accounting for pre-tax Savings

One objection is the $19,000 saved in the Roth was an additional $19,000 taxed at 20%. So the Roth investor (as well as the non-retirement account investor) paid $3,800 in taxes they don’t have today. This is true and it does make a difference.

The Pre-tax investor has $57,000 in their 401(k) minus the $11,400 they owe in taxes plus the $3,800 they saved in taxes or $49,400.

So even when we account for the additional taxes paid by the non pre-tax investors, Roth still appears to be the way to go. See “Total II” below for these numbers laid out.

However, at this point, we can see that the pre-tax 401(k) is at least as good as the non-tax advantaged account.

Total III: Investing the pre-tax 401(k) Savings

But what if pre-tax investor used that $3,800 to buy a non-dividend paying stock, and held that stock until retirement? The $3,800 triples to $11,400, they sell in retirement and have to pay 20% capital gains tax rate on $7,600 in gains so they owe $1,520 to uncle, leaving them with an additional $9,880 to enjoy in retirement.

Wearing the black gloves, Roth has landed the knock-out blow on the pre-tax 401(k): Roth wins

So at this point the pre-tax Investor effectively has $55,480, compared to the Roth Investor who has $57,000.

See “Total III” below.

Both the tax-advantaged investors did better than the non-retirement account investor who has just $49,400.

Even when we account for the pre-tax savings, and even if those savings were invested, the Roth investor still wins.

The reason my prior analysis concluded a pre-tax 401k was equal to a Roth 401(k) is because I assumed the additional taxes reduced the amount saved in the Roth.

When you max out the Roth and save the same amount as a hypothetical pre-tax 401(k), the Roth still wins.

A Roth is Better Under a Specific Scenario

There are a lot of variables and depending on what assumptions you make the Roth could look better than a traditional pre-tax 401(k) or vice versa.

If you are in a lower tax bracket in retirement than when you were saving for retirement then a pre-tax 401(k) would be better.

But if tax rates are the same, and the return is the same, the Roth does have an advantage if you contribute the same amount. The Roth has an advantage even if you invest the tax savings of a pre-tax 401(k).

If I changed the scenario to say the 401(k) tax savings was invested in a high yield dividend paying stock with no dividend reinvestment the taxes on the invested 401(k) savings would be higher and would be due each year the dividend was paid.

Another big advantage to 401(k)s not shown here is that if you rebalance a portfolio (or own investments that pay dividends) those actions are irrelevant in a 401(k) or IRA. However, in a non-retirement account each time a stock is bought or sold, taxes will be due. When dividends are paid, taxes will be due. A retirement account allows savings to continue to grow without

A lot depends on an individual’s tax situation. Unless you are retiring today you don’t know what the tax rate is going to be when you retire. You do know how much money you make, what tax bracket you’re in based on your income and how much you can contribute to tax-advantaged retirement accounts.

$57,000 Roth is worth more than $57,000 in a pre-tax 401(k)

A car with a lien on it is worth less than a car paid in full. So $19,000 in a 401(k) is worth less than $19,000 in a Roth 401(k) because the withdrawals from the traditional 401(k) are subject to income taxes.

This is somewhat obvious but it is important to keep in mind that you owe taxes on your pre-tax retirement savings.

If you invest the tax savings from a pre-tax 401(k) it does narrow the gap but the Roth is still better.

But I doubt most people have the discipline to narrow the gap by saying, “I saved $3,800 in taxes by maxing out my 401(k) so I’m going to put it in this non-retirement account and tag it for retirement.”

In the real world people who contribute to a Roth 401(k) probably have more saved for retirement than people who save in a 401(k) because the people with a 401(k) are probably not earmarking the tax savings for retirement as well.

There are probably a lot of people who don’t even have non-retirement accounts and their employer sponsored 401(k) are their only stock market investments. In this scenario saving in a Roth 401(k) is effectively saving more for retirement for the reasons stated above.

I already preferred a Roth IRA/401(k) to a pre-tax account and now I prefer it even more! Not only does a Roth allow me to save more for retirement, but I think tax rates will be higher in the future and I like knowing how much I have saved for retirement without having to factor in how much the government will take when I make a withdrawal.

I do invest in a 401(k) if it can reduce my taxable income and get me into a lower tax bracket. Pre-tax savings also provides tax diversification which is important when I don’t know what my future tax situation will be in retirement.

Roth IRA vs 401k: who will win? Both plans enable a person to save and invest for retirement in a tax advantaged way. What does tax advantaged mean? That you pay less taxes!

I recently wrote about how costs are rising–specifically about how my healthcare costs went up by $1,000 if I were to have a very bad year. But I have a solution for rising healthcare costs, the Health Savings Account (HSA).

I expect the trend of healthcare cost increases to continue, especially as the U.S. population ages. Another factor that contributes to healthcare costs rising is that the Affordable Care Act was not repealed in full–however the individual mandate was repealed.

This means that people with pre-existing conditions will still be able to get healthcare, while healthy individuals will be able to choose not to buy health insurance. This sounds good, and I’m all for helping people who need medical care get it, however, it means that insurance companies will have more sick people and fewer healthy people, which means more people consuming medical care relative the number of people paying for it, which will put upward pressure on healthcare costs.

I think a great way to save for health expenses in the United States is a health savings account. I’m not an accountant, lawyer or financial advisors but I’ve decided that putting money away in an HSA makes a lot of sense for me. Money contributed towards an HSA reduces gross income.

In order to open and contribute to an HSA you do need to have a a qualifying High Deductible Health Plan (HDHP), which in 2018 was a plan with a minimum deductible of $1,350 and a maximum deductible of $6,650 for an individual. So it makes sense for folks who are relatively healthy. And you need to be able to contribute enough money to the HSA to be able to cover your deductible.

The nice thing about an HSA is that once you have it you can draw from it to pay for eligible healthcare expenses even if you are no longer eligible to contribute to it. Like an IRA an HSA does not expire and it travels with you. However, unlike an IRA you don’t have to wait until you’re 59.5 to make withdrawals penalty free. You can spend HSA dollars on qualified medical expenses immediately.

Health Savings Account Benefits

Reduces gross income (taxable income) even if you don’t itemize your deductions

Contributions remain in your account until you use them

Interest or other earnings on the assets in the account are tax free

Distributions are tax free if used to pay for qualified medical expenses

HSA stays with you even if you change employers or leave the workforce

I have a health savings account through Further (formerly SelectAccount). When your account is up to $10,000 you have the option to activate a self-directed brokerage investment account, which you can then use to invest in mutual funds, bonds and stocks.

There are contribution limits so it might take 2-3 years to get to $10,000 even if you could write a $10,000 check.

So by having $10,000 in an HSA you can have a tax advantaged investment account where you own stocks that would do well in an inflationary environment.

I think the best way to account for healthcare expenses is to not have them. Eating healthy and exercising (something I use more of myself!). However, the human condition is such that, especially as we age, healthcare costs become a significant financial burden. A health savings account is a great way to alleviate that burden.

Taxes are a large cost when it comes to investing. In the United States long term investments (held 366 days or longer) are taxed at 15% for most people. For those in lower tax brackets long term capital gains are taxed at 0% and for those in the top tax bracket the IRS calls for a 20% cut.

So, if one has $20,000 in gains 15% would be $3,000. In another example $100,000 in gains would be $15,000 paid to the IRS. It’s not an inconsequential amount. Furthermore that amount of gains is very realistic, particularly over a long period of time, $10,000 invested over a period of 40 years with an 8% interest rate would grow to over $217,000.

Fortunately there are ways to shield long term retirement savings from these destructive taxes. One way is a 401(k) and another is an individual retirement account (IRA).

Traditional 401(k)s and IRAs

Many employers offer 401(k) plans. A 401(k) allows pre-tax money (money for which income tax hasn’t been paid) to be invested. Unfortunately the medicare and social security payroll taxes are still due. One can start taking money out of a 401(k) at age 59 and 1/2. Any distributions from a 401(k) (with some exceptions) prior to age 59 and 1/2 will result in taxes being due plus a 10% penalty.

No capital gains taxes are owed when the investments are sold and distributions are made but the money is taxed as ordinary income at the state and federal level.

The main advantage to a traditional 401(k) or IRA is that the money grows tax deferred and it is only taxed once. If one were to simply invest money from a paycheck without a retirement vehicle it would be first taxed at the Federal and State level and then any capital gains would be taxed as well.

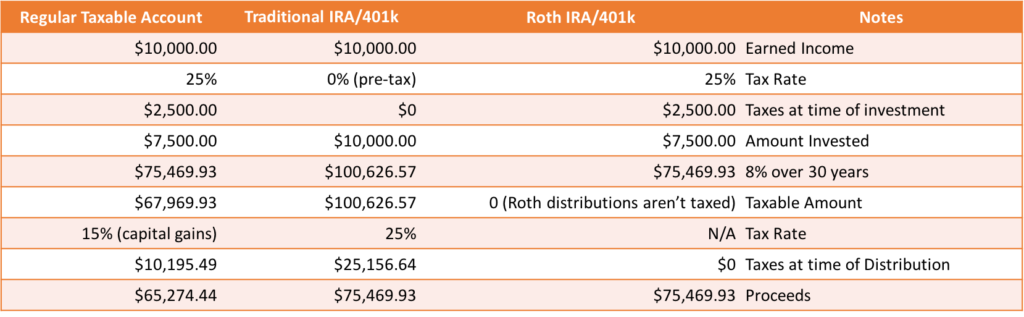

For example, if one were to allocate $10,000 from a paycheck to an IRA or 401(k) it would not be subject to any state or federal taxes. It would hopefully grow (lets say at 8% over 30 years). After 30 years it would have grown to $100,626.57 and all the money is withdrawn from the 401(k). At this point (assuming the person is over 59 and 1/2) the money would be taxed as ordinary income. Let’s assume for the purposes of this example it is taxed at the 25% tax bracket, and thus the IRS would be expecting $25,156.64. The total proceeds would be $75,469.93.

A traditional IRA would work the same way with an important caveat. Your employer isn’t aware of the IRA so you will be overpaying in your federal and state withholding taxes in each paycheck (and get a larger refund which I think is a BAD thing), because the income reduction won’t come until you file your taxes the following April. But you can compensate for this by increasing withholding allowances.

This brings up the secondary advantage of IRAs and 401(k)s: they allow you to reduce your taxable income. This can be particularly helpful if one is on the cusp of a tax bracket. For example, lets say you made $40,000 in otherwise taxable income in 2016. If you contributed $4,000 to a 401k, instead of having to pay 25% on the amount over $37,651, you’d be taxed no more than 15% on any earnings that year.

Roth 401(k)s and IRAs

Traditional 401(k)s and IRAs are not taxed initially, but are taxed when money is withdrawn. Roth IRAs and Roth 401(k)s work in reverse. You don’t get any tax benefits initially with a Roth 401(k) or Roth IRA. You use after tax money to save for retirement but you don’t have to pay any taxes on distributions.

If your tax bracket is the same when you put money in the IRA as when you withdraw the money, it doesn’t matter if you have a Roth IRA or a traditional IRA, the tax savings is going to be the same.

However, if you’re in a higher tax bracket later in life as compared to earlier in life, the Roth 401(k)/IRA is better because you can pay taxes at say 15 or 25%, invest the money, it grows tax free, then if you’re in a 35% tax bracket because you’ve made it big and you’re still working at age 59 and 1/2 you can withdraw that money and you don’t have to pay any additional taxes.

Conversely, if you’re in a lower tax bracket when you retire the traditional IRA or 401(k) is going to be better.

But because of the move towards a more socialized society and given the monstrous debt in the US I anticipate taxes will only go up in the future. So I’d rather pay them now when tax rates are lower.

The Advantage of an IRA or 401(k)

Let’s compare a Roth IRA/401(k), to a traditional IRA/401(k), to simply investing the money without a retirement savings vehicle in a regular taxable account. Let’s say you earned $10,000 of W2 income and want to invest all of it. I’m ignoring social security and medicare taxes because there is no way to avoid those on W2 income in the US, for all three scenarios they are due up front.

As you can see, if one is in the same tax bracket when the investment was made, as when the distributions are made, it doesn’t matter if one has a Roth or traditional 401k/IRA. But there is a $10,000 advantage over a non-tax advantaged brokerage account.

3 November 2019: However, this is only true when you assume that the loss of tax savings is taken out of the amount saved in a Roth IRA or 401(k). If the same amount is in both accounts the Roth IRA/401(k) is better.

Roth or Traditional?

I prefer after-tax, Roth IRAs/401(k)s in general but in specific circumstances using a pre-tax vehicle makes more sense. I like Roths because I can check the balance of my Roth IRA or Roth 401(k) and I know that is how much I would have access to when I achieve an age of 59 and 1/2. I don’t have to figure in taxes. I also hope to be making more when I’m 60 than I am now. Plus, I think taxes are going to be going up in order to pay for unfunded entitlement programs and to pay the national debt (not that I think it is repayable).

I also generally prefer IRAs versus 401(k)s of any kind because with an IRA you can choose a broker that has more investment options than the limited range of choices employer sponsored plans typically allow. Pretty much all the investment options I’ve seen for company sponsored 401(k)s are very limited and are focused in the US.

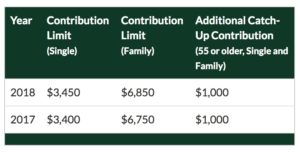

But I will use a traditional 401(k)/IRA under certain circumstances. 1) If I can use it to get to a lower tax bracket. 2) If my employer offers a 401(k) with company matching–I will contribute to the 401(k) until I’ve maxed out the employer match. 3) If I’ve already maxed out the Roth IRA contribution for the year ($5,500 for a single person under 50 years old in 2017) then I would consider contributing to a 401(k).

Wether you go with a Roth IRA or traditional IRA you can only contribute up to a combined total of $5,500 in 2017 if you’re under 50. If you’re 50 or over you can contribute $6,500.

For 401(k)s the 2017 contribution limit is $18,000 but goes up to $24,000 if you’re 50 or over.

So if you contribute to both a 401(k) and an IRA you could save a total of $23,500 in tax advantages funds ($30,500 if you’re 50 or older).

So in general I prefer Roth to traditional, and I prefer IRAs to 401(k)s. However, if my employer offers matching I take advantage of that.

SEPs, solo 401(k)s

There are other tax-advantaged ways to save for retirement, like a SEP or a solo 401(k). I haven’t taken advantage of these options but it is something I’m researching.

I think saving and investing for retirement is important. But there are some strong headwinds working against folks planning for retirement in the US: taxes reduce income and gains, pensions are becoming a thing of the past, Social Security is woefully underfunded, inflation ravages savings.

Tax-advantaged retirement savings vehicles like IRAs and 401(k)s provide needed advantages when it comes to investing for retirement. It’s important to understand how they work and to make use of the tax-advantaged benefits they provide when suitable.

I’m not a tax advisor, CPA, or attorney. I’m just sharing what I’ve done in the past as an individual subject to United States taxes.

This isn’t tax advice.

In my experience there are two steps to avoiding a tax refund.

Step one is to have an accurate prediction of how much tax I will owe (or get refunded) at the end of the year and (this is the key) knowing this information before the calendar year ends when I can still do something about it.

The second step is to take action to influence how much tax will be owed at the end of the year. All while being careful not to owe too much.

It’s important to know the maximum one is allowed to owe in federal taxes and the state level as it could change.

In past years it was $1,000 at the federal level. If one were to owe more than $1,000 in taxes there would be penalties.

Step One: Know How Much Tax you will Owe (or be Refunded) in Advance

Most people don’t look at their taxes until the next year.

For example, right now, most people probably haven’t even looked at their 2016 taxes yet. When they do and they realize they will be getting a $2,000 tax refund, well there is nothing they can do now, except file their taxes as soon as possible to get the refund check.

But if one were to assess his or her tax situation in June of 2016, there would still be half a year to make changes.

So how do I predict how much tax will be owed at the end of the year?

There are several ways.

Use Last Year as a Proxy

At a very basic level, one could use the past year as a proxy.

Ask yourself, did I get an income tax refund last year? If so, ask, am I going to be making the same amount next year? Will I have the same or similar capital gain/loss. Will I be making similar charitable contributions?

If one’s tax situation last year is likely to be very close to what it will be this year then it makes sense there will be a similar tax refund.

This isn’t a very sophisticated approach but it is a start.

In order to make an accurate prediction of how much income tax will be owed more a more detailed and comprehensive approach is needed.

Use Income Tax Calculators

Last year I put together a complicated spreadsheet that basically enabled me to calculate my income taxes during the year.

But rather than reinvent the wheel manually like I did–it would have been better to use the prebuilt tools and resources available to calculate taxes due.

One could experiment with the TurboTax W4 Calculator. Armed only with a copy of the most recent pay stub, as well as some other information, like charitable contributions, capital gains/losses, one can tweek allowances to avoid getting a refund.

They key is having tools available to predict how much tax one will owe (or have overpaid) during the current tax year, while a person can still make changes.

Another strategy I’ve used is to start my taxes in December. By December 2016 I had filled out most of my tax information in Turbotax.

Sure, I didn’t have 1099s, W2s or many other tax documents, but I can look at pay stubs to figure out how much my W2 will be, I can look at my brokerage statements to see gains and losses.

This allows me to make decisions when I can still influence my 2016 taxes.

Step 2: Take Steps to Avoid a Tax Refund

Once I have a good prediction of how much of a tax refund I’ll get based on income, charitable giving, capital gains, and other tax situations it’s time to do something about it.

Strategy One: Increase Allowances on the W-4 Worksheet

Increasing allowances on a W-4 reduces the amount of tax withheld from each paycheck.

The tools referenced above enable one to tweek withholding allowances to make sure some money will be owed at the end of the year.

If the max I’m allowed to owe at the end of the year was $1,000, I would try to owe around $500 or so.

This provides some wiggle-room, because despite best efforts, the tax situation could change and I’m only able to estimate what I think my taxes will be Maybe I’ll decide to give a big $1,000 check to the charity in December, or maybe I’ll suffer a large realized stock loss I wasn’t anticipating.

These are things that a taxpayer might not realize are going to happen until later in the year.

Strategy Two: Convert IRA Money to a Roth IRA

I think taxes will be higher in the future than they are now.

So when it comes to retirement accounts I prefer paying taxes upfront (when I think they’ll be lower) and then having that money grow tax free over the course of 40-50 years, and then be able to withdraw it tax free.

Thus I prefer a Roth IRA over a traditional IRA (and Roth 401ks over 401ks).

But employer’s tend to do company matching to a 401k which is pre-tax money. I’ve been in several jobs that had a 401k and upon leaving those employers I’ve rolled my 401k money into an IRA.

So if I know I’ve overpaid my taxes I will convert some of my IRA money to a Roth in late December.

This increases taxable income, but one can opt NOT to have taxes withheld during the conversion.

This tax is still owed of course, but the payment can be delayed until later in April.

So if I know I’ll be getting a refund I can use that as an opportunity to convert some of my IRA money to a Roth.

I did this last year. I was working a W2 job for a half a year, and then when my contract was up I had no job. So I’d been overpaying withholding taxes.

So I decided to convert a large portion of IRA funds to a Roth IRA to avoid getting a refund. If I had known I was only going to be working for half a year I would have increased my withholding allowances.

Strategy Three: Realize Some Capital Gains

You want to be smart about this.

I wouldn’t sell a winning investment just to avoid a tax refund, but if you’ve been thinking about getting out of a winning position anyway, doing so will increase your taxable income.

In the US short term gains are currently taxed as ordinary income.

Strategy Four: Give Money to Charity

This strategy doesn’t help avoid a tax refund, but it is invaluable if you have underpaid your taxes too much, because it is a way to avoid penalties (see page 51).

If I realize that I owe more than the penalty-free amount on my taxes, I’ll give some money to charity or make some additional donations or put some money in a Health Savings Account.

These contributions reduce taxable income and can be useful when avoiding penalties that can be assessed if too much tax is owed at the end of the year.

Similar to strategy one, you can also reduce your withholding allowances to have more tax withheld each paycheck, if you realize that you’ll wind up owing too much at the end of the year.

I Hate Tax Refunds

I hate tax refunds because they are an interest free loan to the government and I have better use for my hard earned money than the IRS does.

It’s vitally important to legally pay all taxes due and remain in compliance with all applicable tax laws. It’s just not worth trying to cheat the IRS.

But there are legal ways to reduce your taxable income and avoid getting a tax refund.

Avoiding a tax refund has nothing to do with cheating the IRS or evading taxes.

It’s simply a way to make sure you aren’t paying more than you’re legally required.

It’s also a way to make sure that you don’t pay the taxes you owe earlier than you’re legally required to do so.

The above strategies are merely things I’ve done in the past to manage my tax burden and isn’t advice.

But these ideas could spark some conversation when you speak to your licensed tax advisor and as you make your own tax decisions based on your own unique situation.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

I recently wrote about how costs are rising–specifically about how

I recently wrote about how costs are rising–specifically about how  In order to open and contribute to an HSA you do need to have a a qualifying High Deductible Health Plan (HDHP), which in 2018 was a plan with a minimum deductible of $1,350 and a maximum deductible of $6,650 for an individual. So it makes sense for folks who are relatively healthy. And you need to be able to contribute enough money to the HSA to be able to cover your deductible.

In order to open and contribute to an HSA you do need to have a a qualifying High Deductible Health Plan (HDHP), which in 2018 was a plan with a minimum deductible of $1,350 and a maximum deductible of $6,650 for an individual. So it makes sense for folks who are relatively healthy. And you need to be able to contribute enough money to the HSA to be able to cover your deductible.