by John | Aug 21, 2016 | Geopolitical Risk Protection, Preservation of Purchasing Power, Wealth Protection

The United States dollar has the privilege of being a widely used currency even outside the US. However, over a hundred years of failed policy, bad laws, and poor decisions have primed the downfall of the US dollar.

The World Reserve Currency

The US dollar is often referred to as the “world reserve currency”. For example, if a company in Canada were to buy something from China, it would not be uncommon for the exchange to be priced in dollars.

Oil is priced in dollars and despite efforts to move to renewable energy the world economy is (and will continue to be for some time) very reliant on fossil fuels.

This dollar dominance has given the United States a great advantage.

The global demand for dollars has helped keep the value of greenbacks up despite unprecedented US central bank manipulation in the form of trillions of new dollars being created.

Normally the creation of new dollars (inflation) would cause a great deal of upward pressure on consumer prices once these newly created dollars find their way into the real economy.

But because of the global demand for US dollars and US government debt these newly created dollars are exported throughout the world lessening the impact of inflation.

The Dollar Doesn’t have the Fundamentals it once did

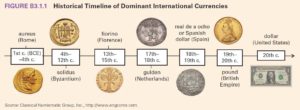

There are a variety of historical reasons why the United States dollar was made the “world reserve currency”.

There are a variety of historical reasons why the United States dollar was made the “world reserve currency”.

The 5,000 foot view is that at the end of World War II the United States had the most productive and largest economy in the world and US dollars were backed by gold.

I would venture to say that none of these reasons apply anymore.

The United States defaulted when President Richard Nixon took the gold backing from the dollar.

The United States effectively defaulted when it went off the gold standard in 1971 in what is known as the “Nixon Shock”.

Depending on what metrics you look at China has surpassed the United States as the largest economy in the world.

Dollars are not a good store of value and the US banking system is a pain to deal with. As an example, French bank BNP Paribas was fined $9 billion for violating US laws regarding who they could do business with.

There is Nothing Exceptional about the US Dollar

In history there are other examples of dominant countries with the privilege of internationally recognized currencies.

In history there are other examples of dominant countries with the privilege of internationally recognized currencies.

Dating back to first century Rome and the aureus, the solidus of the Byzantine empire, the Spanish dollar backed by the mighty Spanish fleet, the dominance of the British pound in the 19th and 20th centuries, and now the US dollar in the 20th century. Each of these powerful empires rose and fell and with it went their currencies.

The Days of the Global US Dollar are Numbered

The days of the US dollar as a world reserve currency are limited.

The United States was once a business friendly environment that allowed entrepreneurs to thrive and bring unheard of prosperity. The United States of today has a labor force participation rate at multi-decade lows, a lack of manufacturing, stifling regulations, the highest corporate tax rate in the world and a hopelessly manipulated fiat currency.

Countries are Already Looking for Alternatives to US dollars

German economist Ernst Wolff has talked about how smaller countries already tried to break from US dollar hegemony with lethal results.

Saddam Hussein of Iraq wanted to sell his oil for euros. Muammar Gaddafi of Libya wanted to introduce a gold backed currency. These men ended up dead.

Source: http://sputniknews.com/europe/20160817/1044347872/brics-economies-expert.html

Russia and China and other “BRICS” nations would benefit from moving away from dollars. They have already moved to trade more in the ruble and yuan rather than the US dollar. No doubt China and Russia would love to see the downfall of the US dollar.

Russia and China and other “BRICS” nations would benefit from moving away from dollars. They have already moved to trade more in the ruble and yuan rather than the US dollar. No doubt China and Russia would love to see the downfall of the US dollar.

Source: http://www.globalresearch.ca/russia-and-china-the-dawning-of-a-new-monetary-system/5423637

It’s also possible, although this is just my own speculation, that China is positioning its national currency, the Yuan, as the replacement to dollars as the world reserve currency.

China’s documented actions, like importing and mining metric tons of gold and lobbying for and inclusion in the International Monetary Fund’s (IMF) basket of currencies, support this belief.

Source: http://globalriskinsights.com/2015/12/impacts-of-the-yuans-inclusion-in-the-sdr-currency-basket/

Unites States Economic Decline

Because the dollar is a fiat currency it’s value is dependent on the strength of the United States economy, the political stability of the country, and the military power of the US armed forces. All of these factors are in decline.

As flawed a metric as it is, it’s worth noting that US average annual GDP growth has been on a downward trajectory for some time.

This election has surpassed the last presidential election in divisiveness. The level of political discourse seldom gets above name calling and personality. Discussing ideas and principles is an afterthought. Corruption and cronyism are rampant.

The United States military is a bloated mess. The US spends more on defense than the next seven combined. Despite this the military is bogged down in failed projects like the F-35 and hopeless engagements in the middle east.

Source: http://www.pgpf.org/chart-archive/0053_defense-comparison

The process of US decline has been ongoing. The downfall of the US dollar is not because of one particular event, but the cumulation of many bad policies and decisions.

One can look at a variety of events, the creation of the Federal Reserve in 1913, the Federal income tax, growing national debt, the post World War II perpetual warfare state, the Nixon Shock of 1971, the Iraq war fiasco, Federal Reserve actions in 2000 and 2008. Historians will debate what went wrong.

Don’t expect the fall of the US economic might to happen overnight. It’s been an ongoing process where one bad decision leads to another.

As the United States’ economy continues to decline, as the US government debt continues to grow unabated and as the US Federal Reserve continues to debase the dollar, more and more countries will move away from US dollars.

As this happens it will cause increased price inflation in the United States and the impact of US Federal Reserve recklessness will be more keenly felt.

It could be that 10, 20 or 50 years from now people look around and realize the United States is no longer the superpower it once was.

How I Protect Myself from the Downfall of the US Dollar

The downfall of the US dollar informs some of the investing decisions I make. I’m investing in physical gold, gold mining stocks, and quality foreign stocks trading at a discount. I’m also dabbling in blockchain investments, despite the added risk in that arena.

The downfall of the US dollar informs some of the investing decisions I make. I’m investing in physical gold, gold mining stocks, and quality foreign stocks trading at a discount. I’m also dabbling in blockchain investments, despite the added risk in that arena.

One of the easiest and in many respects best ways to buy and store physical gold is by opening up a Goldmoney personal account. To learn more about this opportunity and sign up for account, click here.

by John | Aug 14, 2016 | Geopolitical Risk Protection, Preservation of Purchasing Power

I get excited about the prospect of a gold backed debit card from that is not prepaid. I call this type of card a “point of sale gold backed debit card”.

Saving and Spending Gold

I believe that gold is going much higher in the coming years and that dollars will continue to lose value. Saving in gold makes a lot of sense.

Goldmoney is an excellent way to buy physical gold online and store it at locations around the world.

The whole point of saving is to have money to purchase goods and services in the future.

I don’t know any retailers that accept gold as payment. If I want to spend gold I have to convert it to dollars. That’s where the debit card comes in.

Prepaid versus Point of Sale

Prepaid gold backed debit card: Gold is sold for dollars in advance, dollars are spent

Point of Sale gold backed debit card: Dollars are spent, gold is sold to cover sale and pay vendor in dollars

Point of Sale Gold Backed Debit Card

I was over on the “social medes” and asked Goldmoney co-founder Roy Sebag about this.

Roy says that this type of point of sale gold backed debit card should be available in 60 days, which would be early October.

Prepaid Debit Card

Goldmoney (formerly BitGold) currently offers a prepaid gold backed debit card. What this means is a person with gold in a Goldmoney personal account could sell all or a portion of his gold, the proceeds from the sale fund the prepaid card (denominated in USD, GBP, or EUR), the card arrives in the mail and then the debit card can be used to buy things just like any other debit card.

The card can be reloaded or auto-loaded by selling additional gold to load the card with dollars (or EUR or GBP).

If price inflation picks up even more this could be an invaluable tool.

Point of Sale Gold Backed Debit Card

What I am even more exited about is a gold backed debit card that sells gold at the point of sale.

The critical difference between a prepaid gold backed debit card and a point of sale gold backed debit card is convenience.

I could get a prepaid card from Goldmoney and then load it right before each purchase by selling just enough gold to cover the purchase.

I could also load it with a set amount of dollars but at that point the card is really just dollars–it’s no longer really gold backed.

For example, if I were to load a prepaid card with $500 and gold goes up 5% I would miss out on those gains. True, it would work in the opposite as well and protect from losses, but I anticipate a rise in the USD price of gold.

If the card is not prepaid Goldmoney does the math for me. When I make a purchase with my point of sale gold backed debit card, my savings remain 100% in gold until the charge comes across and only then is enough gold sold to cover the purchase.

I wouldn’t have to anticipate how many dollars I was going to spend and sell gold to cover it in advance. I could simply make the purchase and the gold would be sold to cover it.

Again, the difference is subtle but in practice I think a point of sale gold backed card provides the maximum convenience and gold exposure.

If you’d like to setup an account where you can save and spend gold, check out Goldmoney.com and get free gold when you setup and fund an account using this link: Goldmoney.com/r/1HWLl0.

by John | Jul 31, 2016 | Geopolitical Risk Protection, Liquidity, Preservation of Purchasing Power

I remember hearing about inflation as a kid and I remember asking “Why are my savings worth less each year?” What I was really asking was “What causes inflation?”

I might have gotten an answer about rising prices or more dollars in circulation but I didn’t understand. When I got older I did my own research and now understand the mechanics and causes of inflation.

Today I Explain What Causes Inflation

But before I do I want to make sure we’re on the same page regarding what Inflation is.

Inflation and Price Inflation are often used interchangeably, but it makes more sense to separate them out because one is the cause and the other is the effect.

Let’s define some terms:

Inflation: An increase in the money supply. An increase in the money supply is a fancy way of saying there are more dollars in existence than before.

Price Inflation: Rising prices as result of an increase in the money supply.

Inflating the money supply causes rising prices

An Example of the Effects of Inflation

Imagine everyone woke up one morning to find their bank account balances had doubled. The money supply had been inflated by a factor of 2!

Imagine everyone woke up one morning to find their bank account balances had doubled. The money supply had been inflated by a factor of 2!

Some people would choose to buy goods and services with their new-found “wealth”. But there aren’t more goods and services in the economy. Thus, consumers will bid up prices.

Basic laws of economics tell us that when demand increases and supply does not, prices rise.

Prices would then be higher as a result of the increase in the money supply in what is properly called Price Inflation.

What Causes Inflation?

Inflation is caused by creating new dollars. But who is creating these new dollars and how do they do it?

New dollars are created by banks.

The main bank responsible for inflation is the US Federal Reserve. But virtually all other banks also cause inflation via Fractional Reserve Banking.

The Federal Reserve Inflates the Money Supply

The US government spends much more than it brings in via taxes. To make up the difference the US treasury borrows money by issuing debt in the form of bonds.

This debt, these bonds, are then bought by investors, foreign governments, pension funds, and the central bank of the United States called the Federal Reserve.

If the debt was purchased with existing money this would not be inflationary. However, the US Federal Reserve conjures money out of thin air to buy US bonds. How do they conjure money?

They simply create deposits in the Federal Reserve accounts. Imagine if you could go into your bank account and type in that you now had 1 million more dollars. You’d be creating money out of thin air! That is what the Federal Reserve does.

The Fed has inflated the money supply. The Fed caused inflation by creating new dollars.

Using this this freshly minted money the Fed buys US government bonds. The US government then takes the dollars it got from the bonds it sold and spends it on tanks, government employee salaries, national parks, welfare, social security payments, you name it.

This new money that was created out of thin air by the Fed flows through the government into the economy and bids up the prices of goods and services for everyone else.

This resultant rise in prices is one of the effects of inflation.

A Second Cause of Inflation: Fractional Reserve Banking

Another cause of inflation is fraction reserve banking.

Fractional reserve banking means that banks do not have to keep all of their depositor’s funds available for withdrawal. Banks only have to keep a fraction (or portion) of their clients funds in reserve.

When you despot $100 into your checking account it doesn’t go into a vault and sit there. The bank loans that money out to other people or uses it to buy stocks, or bonds, or other investments.

Now banks aren’t allowed to loan out and invest all of their depositors money. After all, if you were to go to an ATM, you need to be able to withdraw cash, or when you write a check to pay your mortgage, the bank needs to send that money to your landlady.

Banks estimate how much money people will spend and withdraw over a given time and they keep that amount in reserve.

There are also regulations in place that dictate the amount of liquid dollars a bank must have in reserve. This is known as the reserve requirement. The reserve requirement is set by the Fed.

If the reserve requirement is 10%, that means that for every $100 in deposits, a bank can loan out $90. So, if you deposit a $100 bill into your checking account, the bank will loan out $90.

The person who received that $90 might spend it on a new pair of shoes. So they give $90 to the cobbler (shoemaker). The cobbler then deposits the $90 back into the bank, which can then be loaned out again. So the bank could make an additional $81 loan. This process repeats itself again and again and that $100 deposit, with a 10% reserve requirement, could become nearly $900 floating around the economy with only $100 in reserves in the bank.

So that little $100 bill has now become $1,000.

If you’re a more visual person you can check out this handy fractional reserve calculator.

So by not holding 100% of deposits in reserve, banks increase the money supply and cause inflation.

Do you have a better understanding of Inflation now?

The actions of the Federal Reserve and Banks cause inflation. I personally don’t like that my dollars are worth less each year because banks only hold fractional reserves and because the Fed prints money out of thin air.

This knowledge has led me to hold some money in gold. Unlike dollars banks can’t create gold by typing in numbers into a computer.

It also goes to show that if everyone were to try to withdraw their money from the bank at once the system would collapse. Don’t count on the FDIC, which is supposed to back up the banks, because it is undercapitalized. This knowledge leads me to hold some money in physical cash.

As I mentioned in a previous article the increase in money supply has caused dollars to be worth half a much since the year 2000.

Another one of the effects of inflation is the creation of bubbles (like the housing bubble of 2008) and the misallocation of resources. But that is a topic for another article.

by John | Jul 17, 2016 | Preservation of Purchasing Power, The Inflation Bandit

If a frog is placed in boiling water, it will jump out, but if it is placed in cold water that is slowly heated, it will not perceive the danger and will be cooked to death.

– Motto of the Inflation Bandit

There is a thief called the Inflation Bandit. He steals YOUR money every year. The ‘Bandit has been robbing and plundering since 1913. He has never been caught and he has never been stopped.

The Inflation Bandit Stole Half Your Money Since 2000

He is a terrible scoundrel and has robbed Americans of millions and billions of dollars but he’s also clever in an evil sort of way.

He doesn’t break into banks and steal money directly–after all that would be dangerous and he’d be caught.

How the Inflation Bandit Operates

The dastardly Inflation Bandit just prints up new money that looks exactly like all the other real money and spends it.

By spending his fake money into the economy he causes prices to go up for everyone else.

So while he doesn’t take your money directly he accomplishes the same thing by stealing the purchasing power of your money.

One of the Million ways this Master Thief has stolen from you

If the Inflation Bandit finds a car he wants he prints up fake money and uses it to buy one for himself and maybe even a few for his friends.

He buys up enough cars so that there aren’t enough left on the lot for all the people with real money to buy one.

When buyers can’t get what they want they tend to get upset. They complain to the car dealer. “I want to buy one of those awesome new cars but you’re sold out! Get some more ordered from the manufacturer!”

So when the car dealer orders more cars from the manufacturer, the dealer thinks, “Hey, people really love these cars! I bet I can raise my prices when I get more. That way people who most want the cars will be able to get one and I’ll make more money.”

Plus the dealer doesn’t like it when his customer’s come in and complain because he doesn’t have cars available for them to buy.

So now the price is higher for people who still want to buy a car. Because the Inflation Bandit used his fake money to buy cars he effectively stole from people who now have to pay the higher price for a car.

Don’t blame Business

It’s really not the car dealer’s fault he sold the cars to a thief. He didn’t recognize the Inflation Bandit. The ‘Bandit wears many disguises and his fake money is indistinguishable from real money.

The Inflation Bandit doesn’t just buy cars, he buys eggs, milk, gasoline, houses, movie tickets, iPhones, computers, cable TV subscriptions. He buys everything with his fake money.

And it isn’t like once the Inflation Bandit spends his fake money it is gone. That fake money is now mixed into the economy and bids up the prices of everything else.

The Inflation Bandit gets slowed down

Back in the late 70s the Inflation Bandit got especially greedy and printed up a lot of fake money. This was causing prices to go up by over 15% per year!

The ‘Bandit got away with it for a few years but people were outraged.

The government cracked down on his efforts and by the mid 80s he was on the run and printed less of his fake money so prices rose by about 5% per year.

Not a bad take for this master thief. He was still stealing millions upon billions but people were less concerned when prices rose by 5%. After all they had been accustomed to prices rising by 15%.

The ‘Bandit learned his lesson

The Inflation Bandit knows if he prints too much fake money people will be outraged. People will demand he be stopped or at least slowed down.

So he’s gotten smarter and he’s gotten patient. He knows that as long as he doesn’t create too much of his fake money each year most people won’t notice it and people won’t be motivated to stop him.

The Inflation Bandit also knows that if people do notice the rising prices they’ll likely blame greedy businesses.

He has a good chuckle every time a business gets blamed for his crimes.

Have you heard of Price Inflation?

While the Inflation Bandit might not be a real person. Price Inflation is as real as it gets. Price Inflation is caused by fake money being spent into the economy.

Price inflation means things cost more and your money can’t buy as much. For example, in 2000, a dozen eggs cost $.96. In 2015 a dozen eggs cost $2.75. That is over a 186% increase in price over 15 years.

Source: http://www.statista.com/statistics/236852/retail-price-of-eggs-in-the-united-states/

In the egg example that is a 7% average annual inflation rate.

Since the year 2000 I believe price inflation causes your money to be worth 5% less per year on average. This means when you try to buy things from food to gas and yes even electronics like iPhones and computers you’re paying 5% more each year than you otherwise would have.

Source: http://www.shadowstats.com/alternate_data/inflation-charts

Another Way to Understand Price Inflation

Lets say you lost a $100 bill in your couch on New Year’s Eve in 1999 and you found it on Christmas of 2015.

With an average inflation rate of 5% that $100 bill in 2015 now has the purchasing power of about $46 in 2000.

You would be able to buy less than half as much stuff! That means you’ve lost over half your purchasing power!

Don’t get Slowly Boiled Alive!

Imagine if you woke up one morning and someone had stolen half of your money. If you’re like me you’d be outraged. You’d call the police and demand justice.

But because inflation causes money to lose value relatively slowly over time it’s harder to notice.

People have had half their dollar’s value stolen over the past fifteen years and few people complain about it.

Like the proverbial frog in water, if the water is heated slowly enough, it will not jump out and be boiled alive.

Most people don’t think much about inflation and they don’t care. But if you buy things using dollars you’re being robbed blind by the Inflation Bandit.

There are ways to protect yourself from inflation thievery but you first have to realize you’re being boiled.

If you’d like to hear about the ways I put the beatdown on the Inflation Bandit click here.

by John | Jun 30, 2016 | Capital Appreciation, Geopolitical Risk Protection, Preservation of Purchasing Power, Value Investing

Trading Australian Stocks is fairly easy. You just need to have the right broker. Making profitable trades is a little harder. But before we get too far into brokers and trading you might be asking…

What is Special about Trading Australian Stocks?

The Australian Stock Exchange (ASX)

If you believe that US and European stocks are overvalued, as I do, and that gold mining stocks are undervalued, as I do, Australia presents, pardon the pun, a golden opportunity.

Australia is a stable jurisdiction that is gold mining friendly. It’s also relatively close to the biggest emerging markets in the world: India and China.

India and China are also some of the world’s largest purchasers of gold.

Why not just trade ADRs?

An ADR is defined by investopedia as follows:

An American depositary receipt (ADR) is a negotiable certificate issued by a U.S. bank representing a specified number of shares (or one share) in a foreign stock that is traded on a U.S. exchange. ADRs are denominated in U.S. dollars, with the underlying security held by a U.S. financial institution overseas.

Source: http://www.investopedia.com/terms/a/adr.asp

If the Australian stock you want to buy IS available as an ADR through your existing broker you can save yourself the trouble of opening a new brokerage account.

But there ARE advantages to owning a stock directly on the exchange (instead of buying the ADR).

1) It costs banks money to create ADRs and they sometimes keep part of the dividend to cover these costs (Peter Schiff, Crash Proof 2.0)

2) Trading stocks on the local exchange can be more liquid (Tim Price, Price Value International)

3) The only way you can acquire many excellent value stocks is to purchase them directly on their “native” exchange. So if you limit yourself to ADRs you’ll miss out on opportunities.

While I do make some of my own stocks picks I also rely on competent professionals that I trust.

Which brings me to…

Price Value International

One such expert I look to is Tim Price.

One such expert I look to is Tim Price.

Among many other accolades Tim boasts 25 years in the capital markets; 15 years as a discretionary multi-asset portfolio manager and was Chief Investment Officer at three successive firms. Tim is currently one of two principals at Price Value Partners and a columnist for MoneyWeek magazine.

Tim also has a monthly paid newsletter called Price Value International (PVI) in which he provides value stock picks of international companies. Tim hails from the UK which I believe helps adds to his unique perspective that is hard to find from asset managers closer to Wall Street.

I receive no financial benefit from Time Price or Price Value International by writing about his newsletter.

But I have been a Price Value International subscriber for over 10 months now and for me it has been worth every penny. As a result I want to share it with my readers.

You can sign up for the PVI newsletter at the following link: Price Value International.

Make Money Like Warren Buffet

Tim Price follows a methodology heavily influenced by “the father of value investing” Benjamin Graham. Graham developed investment strategies that Warren Buffet adopted to grow his fortune.

Using these methods Tim looks for high quality companies around the globe that trade close to or even less than their book value. It’s kind of like buying a house for $190,000, when building the same house would cost $200,000. Value investing provides built in downside protection and is a proven investing method.

Through the Price Value International newsletter Tim shares a new value stock recommendation each month. When you sign up you also get access to back issues so you can see recommendations from prior months.

The stocks range from firms throughout the world and two of them are traded on the Australian Stock Exchange.

I’d love to share the names of these stocks (both of which I own) but it would not be right to do so since I learned about them from Tim through his Price Value International newsletter.

But if you do sign up for PVI and/or decide you want to trade stocks on the Aussie stock exchange, I can provide you with the name of…

A Broker that allows you to trade directly on the Australian Stock Exchange

Most foreign brokers don’t accept US clients largely because of the onerous US laws foreign brokers would have to comply with if they did allow US citizens.

However, I’ve found a US based broker that allows you to trade directly on the Australian Stock Exchange.

This allows me to purchase an Australian stock recommended by Tim Price that I know for a fact is not available as an ADR.

This broker has no minimum account balance which is great if you don’t have a lot of capital to invest.

I DON’T get anything if you sign up for an account with this broker. It’s a firm that I personally have an account with and find valuable.

What is the name of the Broker?

I AM trying to gain more subscribers to my own FREE email newsletter where I talk about what I’m doing to grow my wealth. So while I’m more than happy to provide the name of the broker at no cost, in return I just ask that you sign up for the How I Grow My Wealth email Newsletter using the form below.

Again, out of respect for Tim I’m not going to share the name of any of his stock recommendations. Plus he might cancel my subscription and then I’ll miss out!

But I am happy to share the name of broker that I use.

I was able to start trading Australian stocks quickly. It took me less than a week to get my account setup and make my first trade.

To get instant access to the name of this broker simply sign up for my free email newsletter using the form below.

by John | Jun 16, 2016 | Capital Appreciation, Passive Income, Preservation of Purchasing Power, Real Estate

Buying Rental Property and Real Estate has helped create many a millionaire. Robert Kiyosaki, Barbara Corcoran, and even Donald Trump amassed fortunes via Real Estate.

Buying rental property is an investment that hits on three out of five of my Investment Goal Categories: Capital Appreciation, Preservation of Purchasing Power and Passive Monthly Income.

At it’s most basic level, investing in rental property consists of buying a property and then renting it out to gain monthly income.

I don’t directly own any rental property at this time but it is an area I’m investigating and learning more about.

Buying Rental Property has Five Great Benefits

1) Passive Monthly Income (Cashflow)

2) Equity Build-Up

3) Leverage Utilization

4) Very Favorable Tax Benefits (in the US)

5) Appreciation

Let’s explore the five benefits of buying rental property.

Passive Monthly Income

In many areas it’s feasible to purchase a rental property that generates positive cashflow each month. Even after making a monthly mortgage payment, taxes, fees and maintenance expenses, a good rental property can be have net positive cashflow from the rent payments of the tenants.

In many areas it’s feasible to purchase a rental property that generates positive cashflow each month. Even after making a monthly mortgage payment, taxes, fees and maintenance expenses, a good rental property can be have net positive cashflow from the rent payments of the tenants.

This meets one of my investment goal categories of passive monthly income.

Equity Build-up

Many banks will loan qualified persons enough money to purchase a rental property but typically require a 20-30% down payment. By renting the property you can use the rental income to pay the mortgage and continue to build equity in the property until you own it outright.

With equity in a property you have the option to choose between selling the property, taking a loan out on the property and re-mortgage it, or simply hold onto the property and continue to enjoy the monthly income.

Leverage Utilization

By taking out a loan to buy a positive cashflow rental property you are leveraging the capital you have to make more money. For example by using $16,000 for a down payment you could purchase an $80,000 property and rent it for $600 per month. Lets say after making the mortgage payments, paying property taxes, and other expenses, you are bringing in $150 per month in cashflow. At the end of the year that $150 monthly income would be $1,800 from a $16,000 investment, or over an 11% return. And that doesn’t even include the increase in equity.

Because of the use of leverage, price inflation actually reduces the cost of the remaining loan balance over time. This combined with the universal human need (and hence demand) for shelter even when the economy is not performing well makes buying rental property a great investment for preserving purchasing power.

Tax Benefits

I’m not a CPA or tax advisor, but I understand that when it comes to investment properties, mortgage interest, depreciation of the property, and other expenses that go into maintaining the property are tax deductible. Often times the 11% profit can be made tax free because of all the deductions the tax code (at least in the US) provides to real estate investors.

Appreciation

Partly due to price inflation, partly due to an increasing population and demand for housing, real estate prices tend to rise. So it is possible to grow wealth because the value of the property has gone up. While this is more on the speculative side of the housing and real estate market, appreciation can be a very nice bonus.

This meets one of my investment goals of capital appreciation as well as preservation of purchasing power.

What has stopped me from Buying Rental Property in the past?

- Capital I need money for a down payment. Most of my savings go into stocks and I want to buy a rental property with new money. So I’m going to start earmarking money for buying rental property. While it might be possible to buy a property with zero down I think this is reckless and irresponsible. It’s a good way to find yourself underwater on your mortgage. By making a 20% down payment you can weather a 20% drop in the value of the property and still be even in terms of equity. Plus if the property is cashflow positive, even if you are not making money via appreciation, you can still make money via cashflow and equity building.

- Knowing how to make an offer I would like to better learn how to coordinate having a loan pre-approved with making the offer. With real estate you have to be able to move quickly. In some markets if you go eat lunch to think it over the property will be sold by the time you get back.

- Maintenance Costs and Expenses If you know purchase price of a property and how much you can rent it for (by looking at similar properties being advertised in the same area) and what your costs are going to be you can determine if a property will be profitable (or not). However, I find the most difficult part to research is estimating maintenance costs. The hot water heater breaks, furnace needs repair, a crazy tenant tears up the place, etc. As someone who has been a renter all his life I don’t have a good sense of how much I need to budget for maintenance costs for a rental property. These costs are a huge factor in the profit and loss calculations.

There are five great reasons why real estate investing is a superb way to build and grow wealth. I’ll be sharing my progress in the coming months as I continue to learn more about real estate investing.