Despite the fact that he is now 100% complicit in blowing a giant bubble that will eventually destroy the US economy as we know it, Trump is looking like a game theory genius.

Trump as Bagholder

Before he took office Trump knew the stock market was in a “big, fat, ugly bubble”.

Of course after he took office that capacious and ill-favored looking bubble magically transformed into a beautiful example of legitimate growth thanks to President Donald J. Trump parking his rump in the oval office. But I digress.

I thought the powers that be were going to crash the stock market in time for Trump to be defeated by whichever Democrat candidate manages to climb over the metaphorical bodies of the other ones.

Meanwhile Trump got the beginnings of a tightening cycle. In other words, under Obama everyone got drunk and partied, but when Trump took over the booze started to get packed up and the markets began to sober up with a nasty hangover.

However, by using tariffs Trump is forcing the US Federal Reserve to cut interest rates. This will re-inebriate the markets and probably ensure his re-election.

Trump will keep doing erratic tariff threatening, forcing the Fed to lower rates, until rates are as low as Trump wants, then he’ll declare victory in the trade war. The removal of the trade war worries coupled with low interest rates would rally the markets skywards like bubbles in a tornado.

Trump has found a way to avoid being the bag-holder of the next stock market crash, at least until his second term.

At least that is the theory to which I subscribe.

The Fed Doesn’t Want to be Blamed

One potential problem with this theory is that if the Fed really was out to get Trump, they could simply ignore his antics, hike rates and that combined with the tariffs would cause the markets to sell off, a lot, and probably trigger the next great depression and ensure that Trump couldn’t win the 2020 election against the devil himself.

However, Trump has talked about the Fed a lot, and put them more in the spotlight, so if the markets do crash, they might be afraid that Trump will successfully be able to blame them. So while the Fed would like to tighten, and lay the blame of the market crash at Trumps feet, they are afraid of Trump on the bully pulpit saying that the Fed crashed the markets and causes the recession.

So they essentially are caving to his desires to avoid being perceived as the bad guys. I think this explains why, against all conventional wisdom, with the markets at all time highs, price inflation as measured by the CPI near the 2% target, and low unemployment, the Federal Reserve cut rates.

If they had continued to tighten, while Trump was complaining about them, they might get blamed and they can’t have that.

At the same time they don’t want to look like they are not “independent” as they are so proud of claiming, so they can’t do the full 50 basis point cut and start easing, as it will look as though they are just following orders.

Trump Turns to Twitter

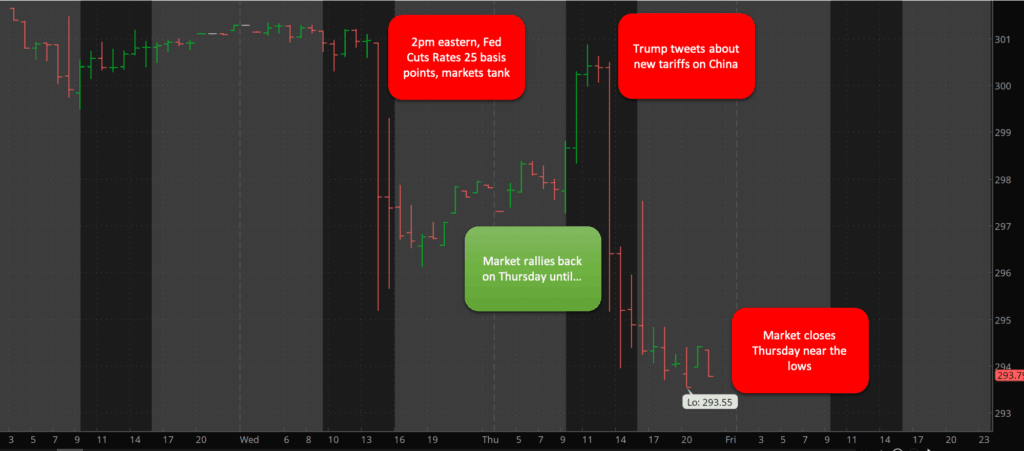

Consider that yesterday, July 31st 2019 Powell’s Fed cut rates by 25 basis points, but indicated it was basically a one and done insurance cut and not the start of a new easing cycle.

Mr. Market didn’t like this and sold off with only a modest partial rally going into the close as you can see from the SPY chart below.

Now at around 10am on August 1st the S&P 500 had rallied back to about where it was before Jerome Powell spoiled the party with a paltry 25 basis point cut and jaw-flapping about this not being the start of a new easing cycle.

Trump is fond of taking credit for the stock market highs, as Presidents are wont to do, so he wouldn’t throw cold water on the post rate cut rally, right?

Wrong, sir! Wrong!

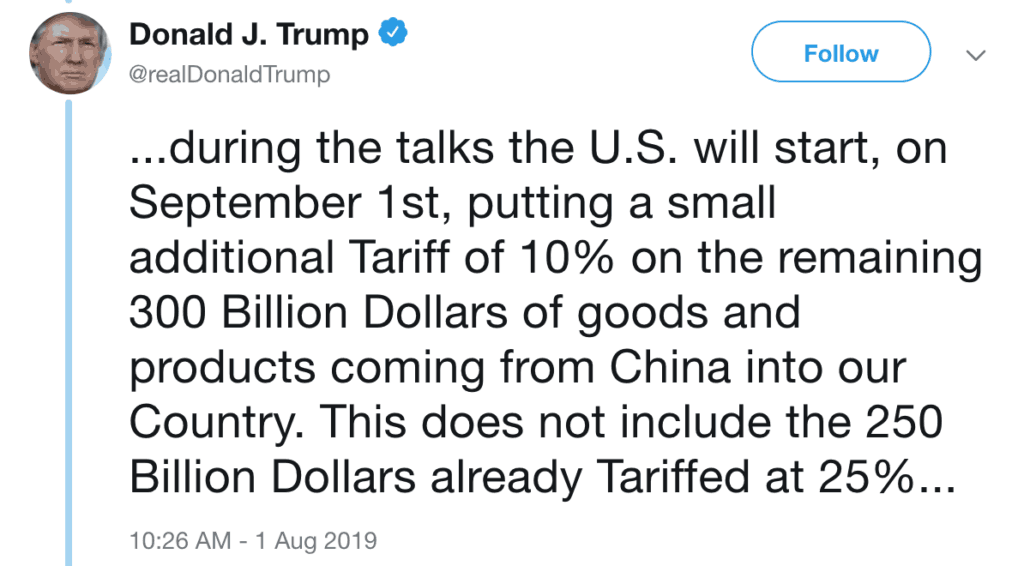

By announcing new Tariffs on China he stopped the rally dead in its tracks.

Why? Because Trump wanted the Fed to cut 50 basis points and he wants an easing cycle.

So the market tanks down even lower than it was before, and the odds of a rate cut in September increases from less than 50% up to 84%!

I should be mad at Trump for encouraging bubble blowing and what is incredibly destructive economic policy, but I have to admit I’m impressed with his gamesmanship.

A lot of people can’t see past Trump’s third grade vocabulary and “unpresidential” comportment–this causes them to underestimate him. I think Trump is good at persuasion and he understands perception and negotiation.

If it continues to work I think he’ll be re-elected. Of course it means that the day of economic judgment, while postponed will only be worse later.

On the bright side, investments in gold are looking quite shiny. And if the market doesn’t crash on Trump’s watch free markets won’t get wrongfully blamed.

Even though laissez-faire he is not, Trump does represent capitalism in the minds of many, and if the market crashes on his watch the United States will unfortunately pivot violently even more to the left.

Few predicted Donald Trump would be the 45th President of the United States.

Early on in the 2016 campaign, I believed it was going to be an election between Hillary R. Clinton and Jeb Bush. I actually won a bet (1 ounce of silver) that Hillary would be the Democratic presidential nominee.

I was certainly wrong about Trump.

[poll id=”4″]

Democrats hate Trump, the establishment Republicans hate Trump, there was no major news network that was even remotely neutral regarding Trump. He broke all the conventional rules. Trump disregarded the sacred institutions and unspoken rules of politics in the US, communicated directly to the people and defeated the Clinton machine.

Anyone who can set their preferences and biases aside for a minute should be able to appreciate the genius of Trump’s campaign, similar in magnitude to the genius of Barrack Obama’s 2008 campaign.

Trump Spoke Some Truths

Wars of Conquest and Adventure

The Iraq and Afghanistan wars were unpopular and Trump tapped into that sentiment. These wars were foolish, unnecessary and costly both in terms of money but also human lives and global standing.

Trump was right to criticize these wars. His anti-war rhetoric was a welcome divergence from the bi-partisan pro-war agenda that has gone back at least as far as George W. Bush.

An Economy that Left Many Behind

The economy was worse than any other candidates admitted–for people who did not own stocks or real estate. Trump emphasized jobs and restoring the United States to whatever perceived former glory it had.

President Obama presided over a stock market that recovered and made new highs as well as reclaimed highs in real estate prices. But this did not benefit younger people or middle and lower class folks who don’t own a lot of these assets and do have lots of debt and stagnant jobs. So these and the shrinking middle class were primed for Trump’s message.

I don’t know what impact this would have outside of some libertarian and Austrian economics circles, but my ears perked up when Trump made the following statement:

We are in a big, fat, ugly bubble. And we better be awfully careful. And we have a Fed that’s doing political things. This Janet Yellen of the Fed. The Fed is doing political — by keeping the interest rates at this level. And believe me: The day Obama goes off, and he leaves, and goes out to the golf course for the rest of his life to play golf, when they raise interest rates, you’re going to see some very bad things happen, because the Fed is not doing their job.

Candidate Trump, September 2016 Source: https://www.marketwatch.com/story/where-will-stocks-and-interest-rates-go-if-trumps-big-fat-ugly-bubble-bursts-2016-09-29

Trump’s comments regarding stocks being in,”Big, Fat, Ugly Bubble,” as well as commenting that interest rates were too low for too long, certainly resonated with me.

Trump Contradicted Himself

It is standard practice for a politician to say one thing at one time and then say or do quite another thing. Trump was no exception.

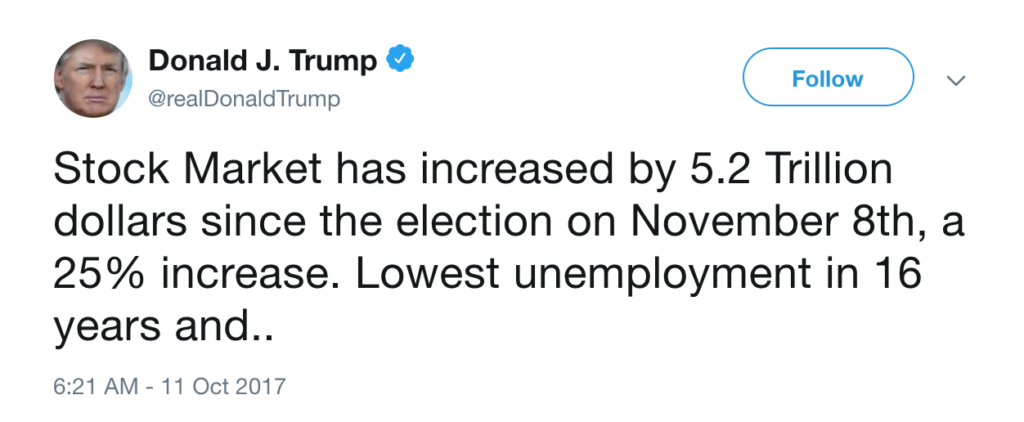

Early on in his presidency Trump began to take credit for the stock market. In Trump’s mind the stock market seems to have magically gone from being a big, fat, ugly bubble to legitimate growth once he was in office.

If this is how you view Trump, you probably don’t care what he does or says.

He has even gone on to demand low interest rates as well as quantitative easing!

I think they should drop rates. I think they really slowed us down. There’s no inflation.

President Trump, April 2019 Source: Source: https://www.reuters.com/article/us-usa-fed-trump/trump-urges-fed-to-lower-us-interest-rates-idUSKCN1RH1M2

War

Trump also attacked Syria and has not stopped aggressive “freedom of navigation” exercises directed towards China. I find this bellicose foreign policy a deviation from what his foreign policy view seemed to be during his candidacy.

Trump’s Reelection will Sink or Swim with the Economy

Typically both the red and blue teams tend to pivot to the center after being elected.

But if the Democratic candidates running are any indication, the country will move significantly in a socialist direction.

Not many people believe in reincarnation, and yet believe Trump is literally Hitler.

Unless for the first time in history socialism actually works, this move to the so-called left will be bad for stocks and the country as a whole.

However the world has underestimated Trump before and there are a lot of factors. A big factor is of course the candidate that wins the Democratic primary.

Trump could also initiate some type of military conflict around the world and a president perceived to be tough could be more likely to be re-elected in a time of war.

A large percentage of people who voted for Trump won’t admit or won’t care that he acted in complete contradiction to key elements of his campaign rhetoric. But will the swing voters or people who turned out because they thought Trump was different do so again if the stock market crashes or they lose their jobs?

If the economy crashes before the next presidential election I’m inclined to think Trump will not be re-elected. I think this is the Trump card, which makes his focus on the trade war with China so dangerous for him.

Over the past few weeks I’ve been writing about the faulty wiring in the United States economy that will eventually result in an Economic Conflagration.

The faulty wiring that will ultimately lead to this economic firestorm includes the fact that the real economy is weak, the economy is crushed by profligate debt and that stocks are overpriced and due for a significant crash.

One of the reasons why candidates such as Bernie Sanders and Donald Trump were popular in the last United States presidential primary and general election is because people know that the real economy is weak. They know how much debt they have and they want someone to make radical changes and do something about it.

Unfortunately government has never been particularly good at creating wealth or prosperity.

Some people might choose to rely on politicians to fix things. This website is not for those people. HowIGrowMyWealth.com is for people who want to take some common sense steps to grow and protect their wealth.

Given the faulty wiring the economy it is more important than ever to grow and protect one’s wealth. It might take a while but this faulty wiring will eventually result in a fire that will burn uncontrollably.

I realize this isn’t necessarily very cheery stuff but fear not! There is plenty of room for optimism.

I’m not a doomsday “prepper” or perma-bear and I’m sure that entrepreneurs, if free to do so, will rebuild the economy and usher in greater prosperity that will not be funneled to the politically connected.

I’m also cognizant that the stock market has gone up nearly 300% since the great recession, there hasn’t been hyperinflation in consumer prices and on the surface the crisis seems to have passed long ago. I don’t have a crystal ball and being right early sometimes looks like being wrong.

Despite the relative calm there is faulty wiring in the economy and sooner or later it will spark and ignite blaze that will, to quote Peter Schiff, “will make the financial crisis of 2008 look like a Sunday school picnic.”

The politicians, if they even realize that there are systemic problems in the economy, simply aren’t willing to endure the short term pain and inconvenience of ripping out the faulty wiring in order to fix the underlying problems. So they will continue to kick the can until the economic house burns down.

The bright side is that this will present an opportunity to rebuild the economy based on a strong foundation as opposed to what we have now, a phony economy based on debt, cheap money and consumption.

There will be winner and losers. I’m very optimistic about the future and I want to be counted amongst the winners.

So where am I putting my money?

My asset allocation falls into three main areas. Value stocks, gold and cash.

Value Stocks

Most people love buying things on sale and getting a great deal, expect when it comes to investing. When it comes to investing people want to buy expensive things and hope they go higher. Value investing takes that same common sense, buying things when they’re on sale and applies it to stocks and other asset classes.

The stock market as a whole is overvalued by a variety of metrics. But there are still good deals out there especially in non-US markets. I don’t doubt that value stocks will also go down in the event of a stock market crash but I think they will go down less and they will recover with more strength.

I share my value stock picks publicly. But I only share if I would buy them today or if I would hold or add to my positions with members of my free email newsletter. I will also let me email subscribers know when I buy or sell a stock first, before I publish that information to this website.

Gold

I don’t think you will get rich buying gold but it could prevent you from getting poor. Under relatively normal circumstances the demand for gold is fairly steady and the supply is fairly steady so for the most part the price of gold will rise with the level of inflation.

Gold is a way to save purchasing power. It’s a way to opt out of the financial system and wait for sanity to return.

If the dollar tanks loses it’s reserve currency status gold will still be valued.

I also think there has been significant effort to suppress the price of gold and depending on how much downward price manipulation there really has been, the price of gold could go up significantly from where it is right now.

If fiat currencies collapse that could very well induce a flight to the safe haven asset of gold that this influx of demand would be very bullish for gold.

Because of the absurd expansion in central bank balance sheets and artificially low interest rates I like gold presents a fantastic value at current prices.

What I write about gold applies to silver–another asset I think will do very well in a downturn. Silver has the added benefit of being an industrial metal that is more widely consumed.

Cash

Long term, like every other fiat currency, I think the dollar will go to zero. So why would I want to hold dollars?

First, I own a month or two of expenses in physical cash in a secure location in case there are capital controls. If there is a panic and people start withdrawing money from the banks the banks might in turn say, you can only withdraw $500 a week or something like that. Withdrawal limits could also be imposed if the US implements negative interest rates and people (very rationally) decide it is better to hold dollars in physical cash so they don’t have to pay interest to their bank for the privilege of loaning their money to the bank.

I reside in the United States and everything is priced in dollars so I need dollars to buy things. If I lived in the eurozone I would hold pounds or euros, if I lived in China I would hold Yuan. If I lived in the socialist paradise of Venezuela I would probably hold dollars (and try to get out).

Secondly, apart from physical cash I also hold dollars in a money market fund as a war chest. If stocks tank I expect there will be bargains to be had. I want to be buying stocks (if they are high quality free cashflow producing companies) when everyone is panicking and selling.

Now I fully expect the United States Federal Reserve to do what it has done in all other crises it has created–it will lower interest rates and buy assets to prop up the markets.

With interest rates already low once they cut rates to zero they will only be able to do things like Quantitative Easing and Negative rates. This is very bearish for the dollar and very bullish for gold.

But in the highly unlikely chance the US Federal Reserve does the right thing and lets the stock market collapse and lets the US government default on it’s debts this could be very bullish for the dollar. So holding some dollars is a hedge against deflation as well as a war chest to draw upon to buy undervalued stocks post crash.

What are some other possibilities?

While the bulk of my holdings are in cash, value stocks and precious metals I also dabble in some other alternative investments.

If there is a dollar crisis or collapse in the faith of central bankers then more people could turn to cryptocurrencies and could see it rise. Demand for cryptocurrencies could also rise for other reasons pushing the price upwards.

While I think blockchain technology is here to stay the value of any one specific cryptocurrency or token could very easily tank to nothing. Cryptocurrencies are very risky and 90% swings (both directions) happen.

You need to have an iron stomach but having between 1-5% of your liquid net work in cryptocurrencies isn’t the most outlandish idea in the world.

I would only speculate on cryptocurrencies with what you can afford to lose and I don’t considering buying cryptocurrencies investing in a technical sense since I am simply betting on the price going up.

I’ve shared with my readers my Group of Six cryptocurrencies that I’ve chosen to own and speculate on.

Options

Net I’ve actually lost money trading options. I traded options while unemployed and failed to remain dispassionate and objective. I was so focused on making money that I opened positions when the conditions were not ideal and took risks I should not have been taking.

I do believe if you are disciplined and follow the appropriate rules, you can do well trading options.

During a stock market crash volatility spikes and selling options could be a good strategy. When the VIX (a volatility index) spiked up in early February I sold a few options and those positions are doing well as volatility has dropped and the market has recovered. Markets don’t move straight up or down for very long so even if the February selloff portends drops to come, the market doesn’t drop as fast as people think in the midst of the drop.

Real Estate

Unlike all the other assets mentioned above I do not and never have owned any real estate.

Lots of people have made lots of money in real estate. I am working to learn more about this asset class and hope to own my own rental property at some point.

What I like about real estate is that it is easy to use leverage and the tax benefits are ridiculous. You can effectively pay no tax on investment property income and borrow a lot of the money you need to get started.

You of course need to know what you’re doing.

My goals for owning real estate involve owning a multi-family apartment building. The key for me is a cashflow positive property. I don’t have any interest in trying to buy and flip, although some people are very successful doing this. There are lots of ways to make money in real estate and I recommend biggerpockets.com to learn about them.

I think cashflow positive real estate will do okay in the event of a crash. If you’re in an area that has stable employment prospects those workers will always need a place to live and have the money to pay for it. Of course real estate won’t “always go up” and there are a lot of risks and headaches associated with managing property (if you don’t outsource property management).

This is part 5 of 5 of what I’ve decided to term The Economic Conflagration series where I discuss the faulty wiring pervasive the global economy:

Not only is this debt impossible to repay but it continues to grow with little chance that this spending will subside until it has to.

According the United States Congressional Budget office the US Federal Government brought in $3.3 trillion in taxes in 2016. The US Federal Government spent $3.9 trillion.

But the vast majority of expenses was in areas that simply will not be cut.

The United States spent $910 billion on Social Security, $588 billion on Medicare, $368 billion on Medicaid, and another $563 billion on other mandatory spending which includes items such as Federal employee retirement programs, SNAP (food stamps) and Veteran’s Benefits. So total “Mandatory” spending was $2.4 trillion. These are the kinds of programs that will never be voluntarily cut by any congress and in the case of Social Security and Medicare, will only go up in cost as more people retire.

Not only that, once you factor in interest on the $241 billion in net interest paid on the national debt (another item that congress won’t cut because it would tank the credit rating of the United States) total spending rises over $2.6 trillion. Considering congress keeps borrowing and that interest rates are rising these borrowing costs will only continue to rise.

This leaves $630 billion left to spend.

But $584 billion goes to the military. Which leaves $36 billion left. However in 2016 the US Federal Government spent an additional $600 billion in discretionary money.

The red team politicians will never cut defense spending (the blues realistically won’t either).

Neither side is interested in cutting social safety net programs either like Medicaid or SNAP.

Neither side will cut Social Security or Medicare.

There a Fiscal Crisis on the Horizon

The $20.49 trillion in “Total Public Debt Outstanding” does not include unfunded Social Security and Medicare obligations.

The 2017 Social Security and Medicare Boards of Trustees report has again stated that these programs are underfunded. “The Trustees project that the combined trust funds will be depleted in 2034, the same year projected in last year’s report.”

https://www.ssa.gov/OACT/TRSUM/index.html

The Trustees cite an increase in baby boomer retirees drawing Social Security and Medicare and fewer workers paying into the system.

How will the United States Federal government make up the difference between the benefits promised to be paid out and a depleted “fund”? In reality there is no “fund” and the money from payroll taxes goes into the general budget. Lawmakers only have a few options to “save” Social Security and Medicare: some combination of raising taxes and lowering benefits (either by raising the retirement age or reducing the monetary value of benefits paid out). That is of course unless people start having a lot more kids who in turn have jobs and pay into the system.

The last option, which is really a way of lowering benefits in a dishonest way, is simply borrowing and or “printing” the money to pay the benefits.

But these expenses incurred in 2016 don’t include a multi-billion dollar bailout of some kind, funding a new war or some other large, unforeseen expense. So what would happen to the Federal debt if one of these events occurred?

Debt at the federal level will continue to climb.

Debt at the State Level is Unrepayable

I grew up and lived in Illinois for most of my life. It is just about the most indebted state in the United States, surpassed only by New Jersey.

Illinois only had enough revenue to cover 96% of expenses in 2015. The Illinois government is more than capable of overspending in any circumstance, but the revenue shortfall continues to be exacerbated by the state population decline. A total of 114,144 residents moved out of the state in 2016 and new residents plus births could not offset this exodus. The result was the count of Illinois residents dropping by 37,508 people in 2016.

Despite this Illinois remains the 5th most populous state in the US and the fact that the fifth most populous state is in such a bad financial position does not bode well.

While Illinois can issue debt and for some reason their debt continues to be purchased, their financial risk means the cost of borrowing is high and without a central bank they aren’t able to drive down the cost of borrowing or print currency. Not that those strategies work in the long term, but they don’t have those tools to delay the pain.

I choose to single out Illinois since they spent years of my hard earned tax dollars so recklessly but many other states are in bad shape as well.

Overall state pensions are underfunded by a total of between $1 trillion to $4.3 trillion depending on how well you think the pensions will perform.

Despite years of economic “recovery” since the 2008-2009 financial crisis these problems have only gotten worse. With this “recovery” getting long in the tooth, what will happen when the economy officially slips back into a recession?

Debt at the Personal Level is Unrepayable

Student Loan Debt

Some of the most indebted people in the United States are also some of the least capable of repaying it. I’m talking about former college students. According to Lendedu.com there are over 45 million individuals in the US with student loan debt. The default rate is 11.5%.

A study by Nerdwallet.com indicated the average person with student loan debt owes $46,597 with a total owed of $1.36 trillion.

So there are 45 million people in the US that have a considerable amount of student loan debt.

These are these are the same people who will presumably have to shoulder the burden of the $20 trillion debt and accept delaying retirement or paying more in taxes to pay for baby boomer’s retirement and medical cost.

Auto Loan Debt

US consumers owed $1.21 trillion in auto loans in 2017. Unlike student loans (in which theoretically you borrow money to increase your purchasing power for the rest of your life) or mortgages used to buy a house (which can theoretically go up in value), auto loan debts are taken out on an asset that rapidly depreciates.

On average a person in the US with this kind of debt owes $27,669.

While I am sympathetic to people who have to use a credit card to pay for the basics of life such as food or utilities–credit card debt is a horrible form of debt.

Credit cards are primary used to consume and they carry high interest rates. If you need to use a credit card to pay for something it is likely that you will not be able to pay for it later when it effectively costs more due to the credit card interest.

In 2017 individuals in the US owed $905 billion in credit card debt. Households with credit card debt owed $15,654.

While housing can go up in price, it is not guaranteed to do so, as many people learned in 2008.

With many Americans burdened with debt and without savings the only way they can purchase a house is to borrow the money. As interest rates rise the cost of a mortgage will increase and therefore people will not be able to borrow as much, the result is that housing prices must fall.

Why Does this Debt Matter?

Debt, specifically debt to consume, does not grow the economy. It is a drag on the economy. The amount of debt in the United States will eventually crush the US economy.

Lets assume for a moment that consumption grows the economy even though it does not. If a debtor pays back the loan that means that is money that goes towards the person who loaned the money and not towards buying goods and service. Thus a person is not able to buy as much in the future when they are servicing a debt, all else equal. So even if consumption did grow the economy consumer debt can only pull consumption into the present at the expense of future consumption.

What does grow the economy is capital investment in machinery, tools, training and other technology that make the economy more efficient and allow the production of more goods and services. If there are more goods and services prices will fall and this allows people to buy more goods and services. If it takes less materiel and labor to make something those people and materials can go to work in other or new areas of the economy that they would not otherwise be free to do so.

Another problem is that the person borrowing the money might not be able to repay it, in which case the person who loaned the money will have to take a loss. This does not benefit the economy either.

The massive amount of Federal, State and Personal debt in the United States is a huge drag on the economy and is one of the biggest problems or “faulty wirings” that is coursing through the US economy.

My next article will be about one of the last main areas of faulty wiring in the US economic house: an overvalued stock market.

I’m not all doom and gloom. Far from it. I think there are tremendous opportunities to grow and protect your wealth through alternative investments.

I previously wrote about how this time is not different how there are systemic problems with the US economy and the economy at large. I wrote how there is the economic equivalent of faulty wiring in a building. You don’t know exactly when the building is going to burn down but it is only a matter of time.

One of the three main reasons why an economic conflagration is on the horizon and why it makes sense to start preparing now through alternative investments is the real economy is weak.

There are a variety of metrics that show the real economy is weak. I’d like to look at two: labor force participation and stagnant wages.

Labor Force Participation is Down

I don’t like looking at the unemployment rate for two reasons. 1) If people give up looking for work then that lowers the unemployment rate 2) The unemployment rate doesn’t look at the quality of jobs. If a person loses one high paying full time job but then they get 1 or even 2 part time jobs that pay less and have fewer benefits, that in and of itself, does not impact the unemployment rate, even though the person might be working lower paying jobs outside of their previous field.

The labor force participation rate is by no means perfect either, but it is in my view a more useful metric in today’s economy.

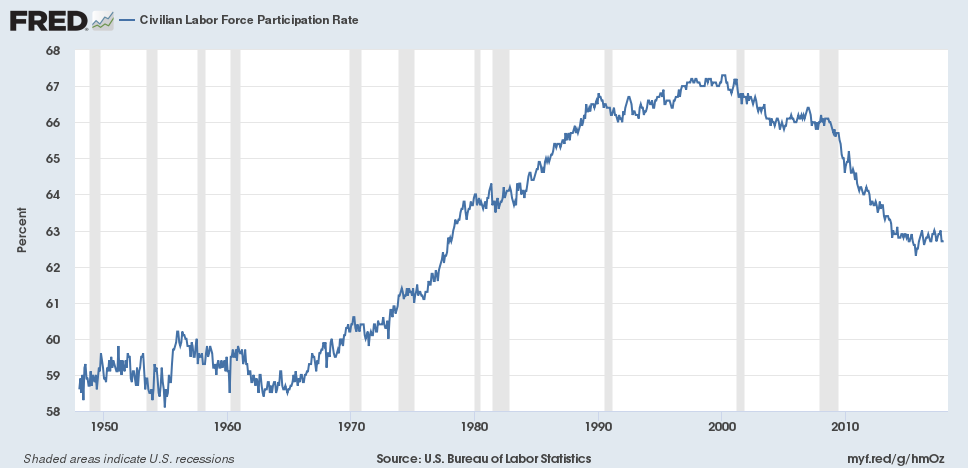

The civilian labor force participation rate is at a level not seen since the 1970s.

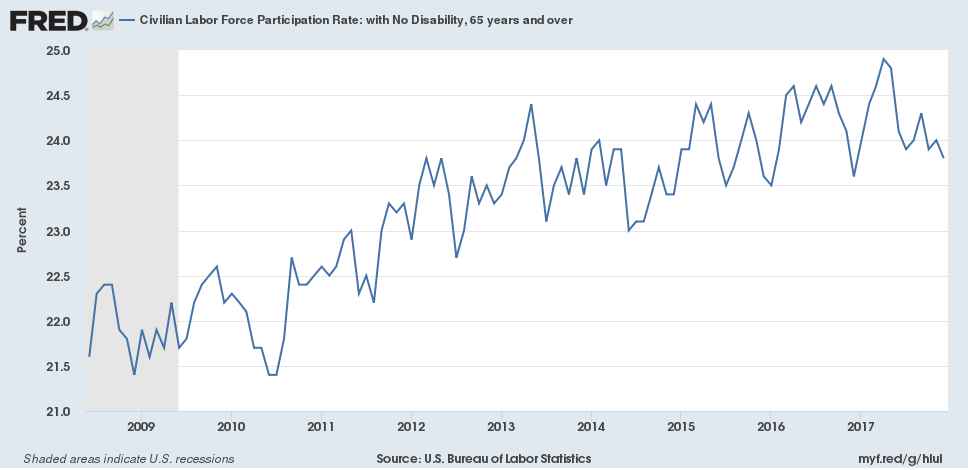

And no, it’s not because the baby boomers are retiring. The labor force participation rate amongst those 64 and older has been steadily climbing even as the the labor force participation rate at large has been declining.

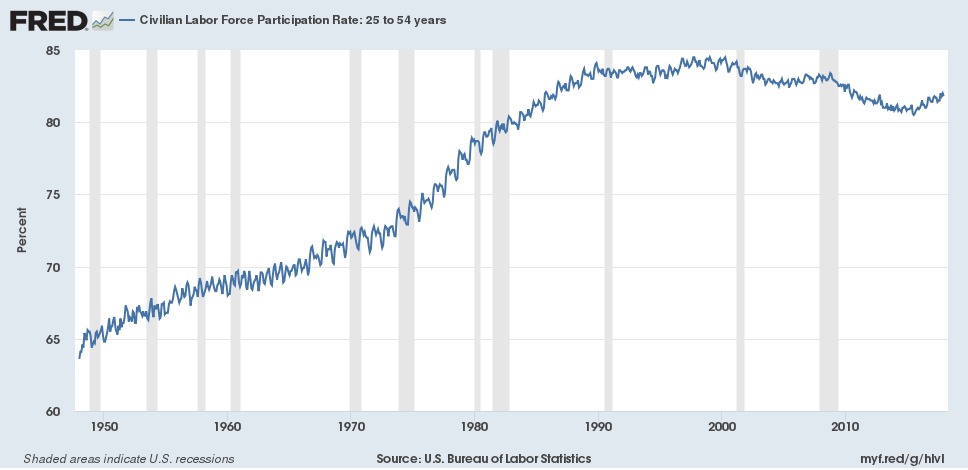

The civilian labor force participation rate amongst those in their prime working years, 24-54, has not regained the levels seen before the great recession nor the dot com bubble, despite rising steadily for decades, it’s been trending down since the peak in the late 90s.

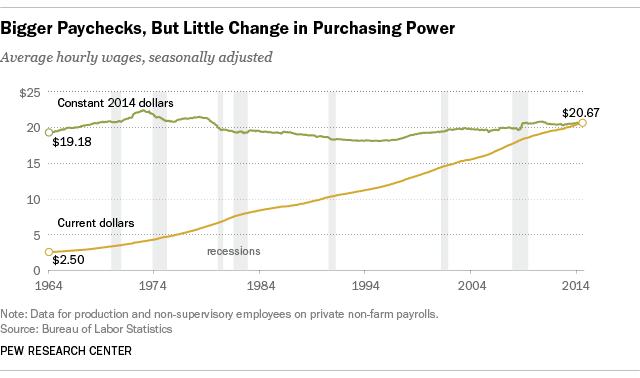

Stagnant Wages

Not only are a smaller percentage of people are in the workforce but those that are working face stagnant wages. According to a PEW Research study, when adjusted for inflation wages have barely budged since the 60s.

However, I’m sure that the inflation adjustments used understate the rate of price inflation. If that is the case then real wages have actually fallen.

Fewer People are Working and They are Getting Paid Less

In summary the real economy is weak. A smaller percentage of people are working and they are getting paid less. The labor force participation rate is on par with levels from the 70s and at best people are not making any additional money and quite possibly making less money on average than in decades past, depending on how much trust you have in the official price inflation numbers.

On top of these factors debt has increased dramatically at the Federal, State, and personal levels. More on that next week.

This is not a consequence free environment. The real economic weakness in the US economy is one of the reasons I think that the US economy (and probably global economy) is due for a large correction. It might not happen this year or even next year, but such a correction is long overdue and it makes sense to take some basic precautions through alternative investments.

Today I read an interview MarketWatch did with Robert Kiyosaki: “‘Rich Dad’ author Robert Kiyosaki: If you’re investing for the long term, ‘you’re crazy’”

I’ve never read Robert Kiyosaki’s Rich Dad Poor Dad but I have read Unfair Advantage. From what I understand from speaking with folks who have read Rich Dad Poor Dad the principles in Unfair Advantage are very similar.

Robert Kiyosaki

I learned from reading his book. I didn’t learn a lot about specifics actions I could take but I did learn about mindset and principles of the wealthy.

For specifics he pushes his paid training classes and seminars pretty hard. I went to one of his “free” real estate seminars and it is sales heavy and content light.

I’ve never been to a paid Rich Dad seminar but I hope they have a lot more actionable content than the free one I attended.

Based on my exposure to the teachings of Robert Kiyosaki I will say that I agree with what he is saying. I just think he overcharges for training and actionable information.

[mc4wp_form id=”4538″]

Summary of Kiyosaki’s Interview

In the MarketWatch article above he says a few things:

Money isn’t money because it isn’t backed by gold

The rich don’t work for money they work for assets

He is predicting a 2016 market collapse

Describes himself as a “gold bug” and views gold not as an investment but an insurance policy and hedge

He states who he’ll vote for with the caveat the president doesn’t make any difference at this time

You know what, I agree with all of that, with the exception of calling 2016 as the year of the crash. It could be but I don’t know when stocks will crash and when they do I believe the Fed will step in and prop up prices.

Kiyosaki in Comment Pillory

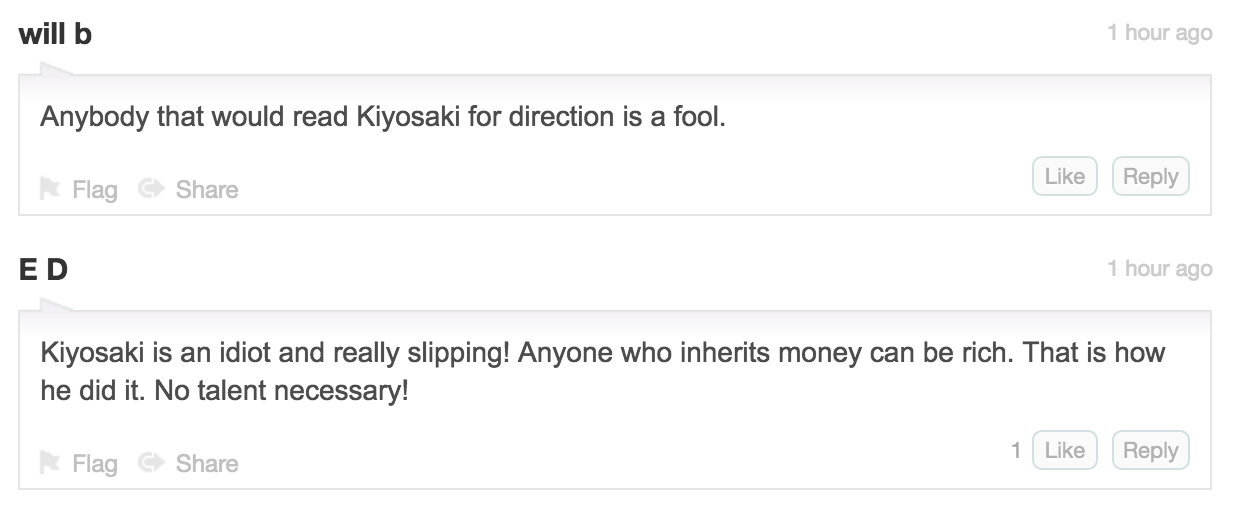

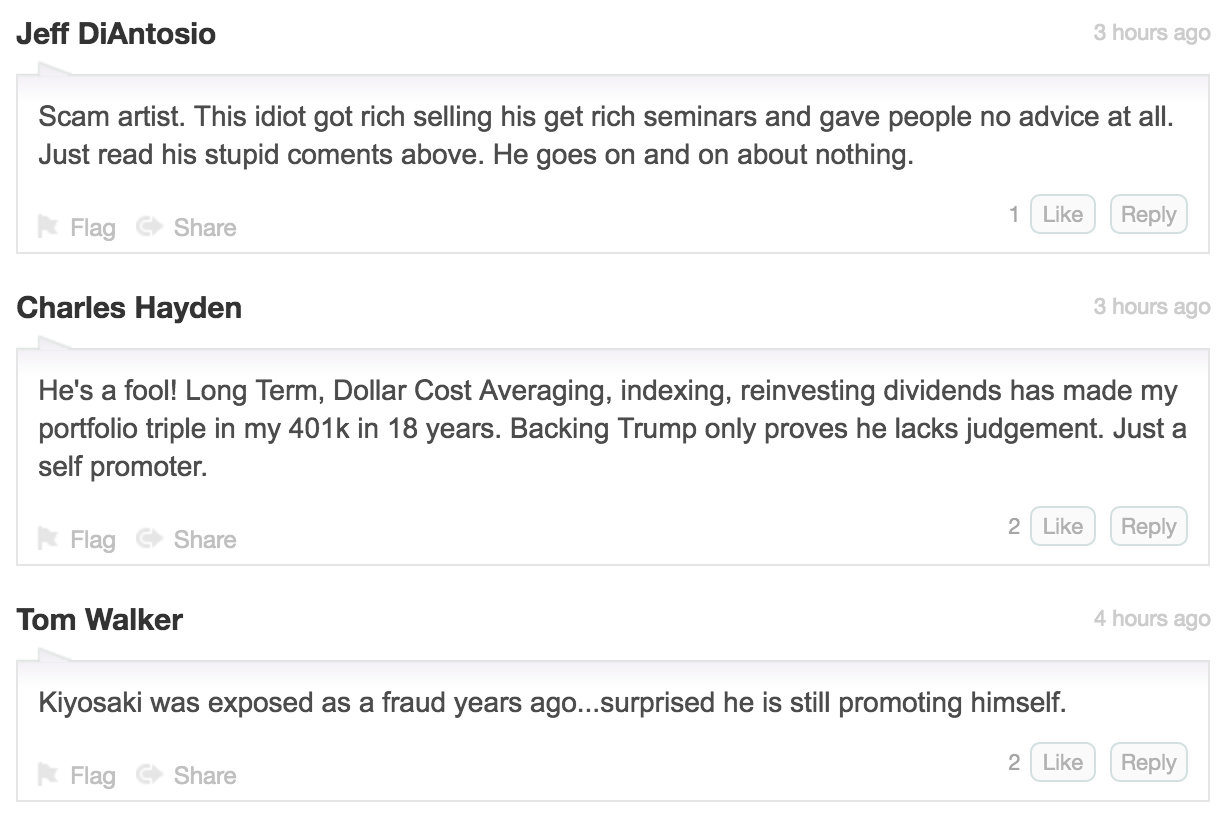

But what I’m surprised by is the comments below the article. They weren’t all negative, but it seemed like most of the ones I read were.

Not a lot of substance besides name calling. I think the comments could provide some insights into how some retail investors think. They don’t want anyone raining on the stock rally parade.

These quotes are from people who, in my opinion, don’t understand the stock market or the economy.

Why I think Kiyosaki is Right

The Federal Reserve’s unprecedented action in propping up assets has created a huge bubble. The bubble is bigger than the dot com bubble in 2000 and the housing crisis of 2008.

Even if you think that the $4 trillion fed balance sheet is no big deal, there are other metrics that indicate the S&P 500 is overvalued. On average the P/E ratio of the S&P 500 has been around 15. It’s currently up to 25. Not exactly a bargain.

Source: http://www.multpl.com/

Gold is a hedge against Federal Reserve and central bank insanity. I don’t think gold should be the sole asset in one’s portfolio but could very well have an important place depending on your risk tolerance and other factors impacting suitability.

Gold (dark red) has outperformed each of the 3 main US indices by nearly 300% since 2000

I also know several people personally who have done very well investing in real estate. I think real estate is a great way to grow wealth with lot’s of tax benefits.

In the article Kiyosaki also discusses one practical strategy for buying a stock, first buying an option, as well as the importance of buying stocks at a great discount. Buying companies for less than their book value is classic Benjamin Graham.

I can appreciate if people don’t like Kiyosaki’s sales tactics as I don’t particularly care for them either. But I would like it if people could discuss ideas without immediately resorting to name calling.

If you think stocks are fairly valued based on fundamental factors, why?

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

Source: https://fred.stlouisfed.org/series/CIVPART

Source: https://fred.stlouisfed.org/series/CIVPART Source: https://fred.stlouisfed.org/series/LNU01375379

Source: https://fred.stlouisfed.org/series/LNU01375379 Source: https://fred.stlouisfed.org/series/LNU01300060

Source: https://fred.stlouisfed.org/series/LNU01300060