Central planners President Donald J. Trump and Fed Chair Jerome Powell both spoke regarding the US Economy this week. Trump was Tuesday; Powell Wednesday.

One interesting quote from Chair Powell’s prepared remarks were the following: “Nonetheless, the current low interest rate environment may limit the ability of monetary policy to support the economy.”

In other words if the economy goes south, the Fed won’t be able to do much to prop it back up.

This assumes rates don’t go negative (like Trump is already calling for) or Quantitative Easing (QE) isn’t further expanded (which Trump has also called for). With those in mind, the Fed still has tools at it’s disposal to wreck the dollar and re-inflate asset bubbles.

Powell also read, “In a downturn, it would also be important for fiscal policy to support the economy. However, as noted in the Congressional Budget Office’s recent long-term budget outlook, the federal budget is on an unsustainable path, with high and rising debt: Over time, this outlook could restrain fiscal policymakers’ willingness or ability to support economic activity during a downturn.”

As he states the obvious, Powell is of course correct about the unsustainable federal budget.

Seeing as how the Fed is empowering the Treasury to go deeper and deeper into debt it is ironic that the Chair of the Fed is concerned about the debt.

Powell also mentioned his “In no sense, is this QE,” Quantitative Easing program: “To achieve this level of reserves, we announced in mid-October that we would purchase Treasury bills at least into the second quarter of next year and would continue temporary open market operations at least through January. “

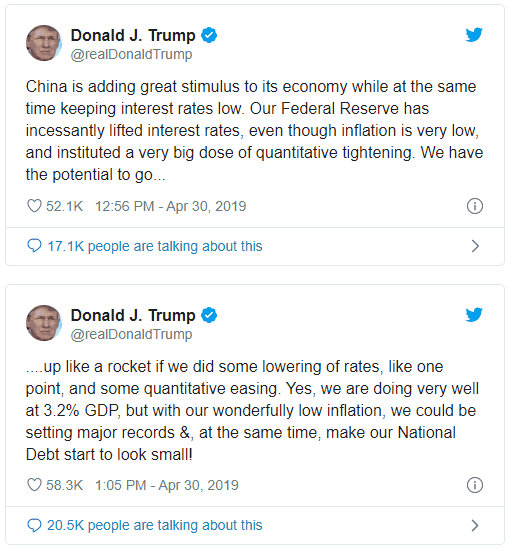

In his Tuesday speech President Trump called for negative interest rates. He is further complaining the Fed isn’t working with him and that interest rates were cut too slowly.

While touting the stock market at all time highs (which he once called a big, fat, ugly bubble), Trump purports the stock market would be 25% higher if not for the Fed.

Trump is the Bubble-Blower in Chief. He basically wants the kind of sweetheart deal Obama got.

He also mentioned a desire for more tax cuts. Tax cuts are fantastic and important, but without cutting spending they will only increase the unrepayable and unsustainable deficits.

All of this should be good news for gold. While the yellow metal has not dropped through the $1450 resistance line, it is hovering just about it.

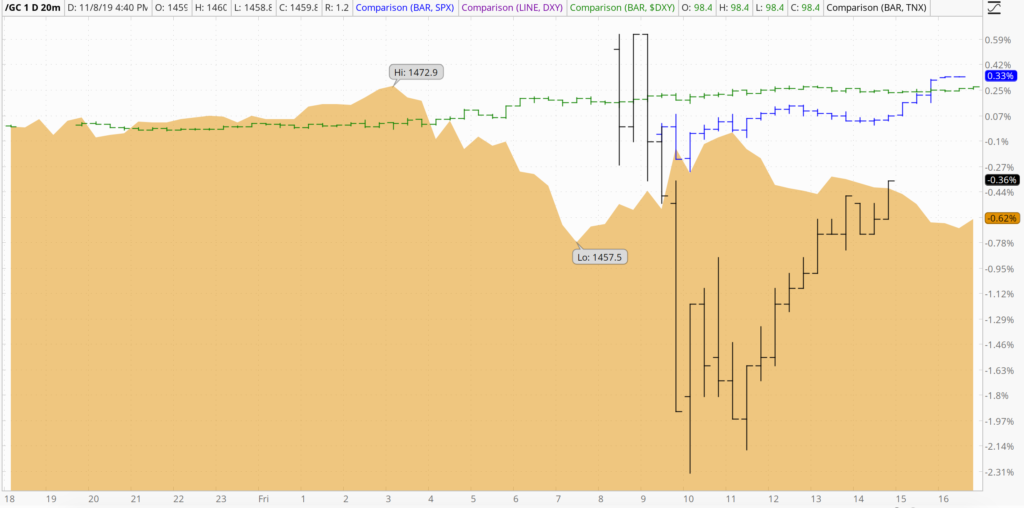

The S&P 500 made fresh and new all time highs Friday. Bonds were down, the dollar index was modestly higher and gold was on the receiving end of a severe drubbing.

On the day the S&P 500 was up 0.33%, the dollar index was up 0.26%, 10-year treasury down 0.36% and gold bring up the rear down 0.62%

On the year gold is still up over 13%. But the over the course of the fall the S&P 500 has surpassed gold’s performance and is up 23%.

Gold has fallen over $100 from the 4 September highs

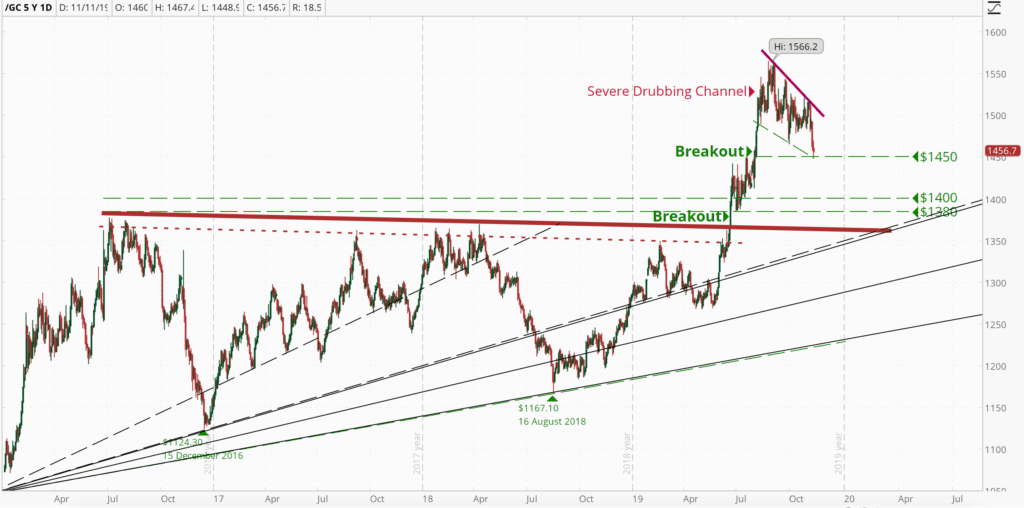

Looking back: 2019 Gold

In June of 2019 Gold finally managed to break out of the monkey-hammer zone of the $1350s, consolidated between $1400 and $1450, made a second breakout and with a great run up as high as $1566.

However, starting in September, gold has been trending down again and has been drubbed down to the mid $1450s.

I think this is a temporary setback for the price of gold and a buying opportunity for someone who is under-allocated in gold.

2016 was indeed the start of a new gold bull market after gold bottomed out in December of 2015.

Finishing 2019 and Beyond

The price of gold ebbs and flows a great deal with news and sentiment. Right now the market seems to believe 1) the Fed is done easing and 2) the trade war is close to a peaceful resolution.

Certainly the Fed is not done easing as the balance sheet continues to grow. There are also certain core issues in which Trump and China are both unwilling to compromise on.

A limited trade deal is certainly possible, but I doubt China is going to relent on certain core demands the US is making.

To me the chart looks bearish in the short term. Some potential places gold can find support would be where it is currently trading, at around $1450. Below that perhaps $1400.

If traders become very optimistic about the stock market, could even go down to $1380 or retest the monkey-hammer zone in the $1360s.

Of course it is only my educated guess but I think gold will find support somewhere between $1400 and $1450.

While the recent price action looks rather bearish over the next 3-6 months I think gold will reach $1600 in 2020.

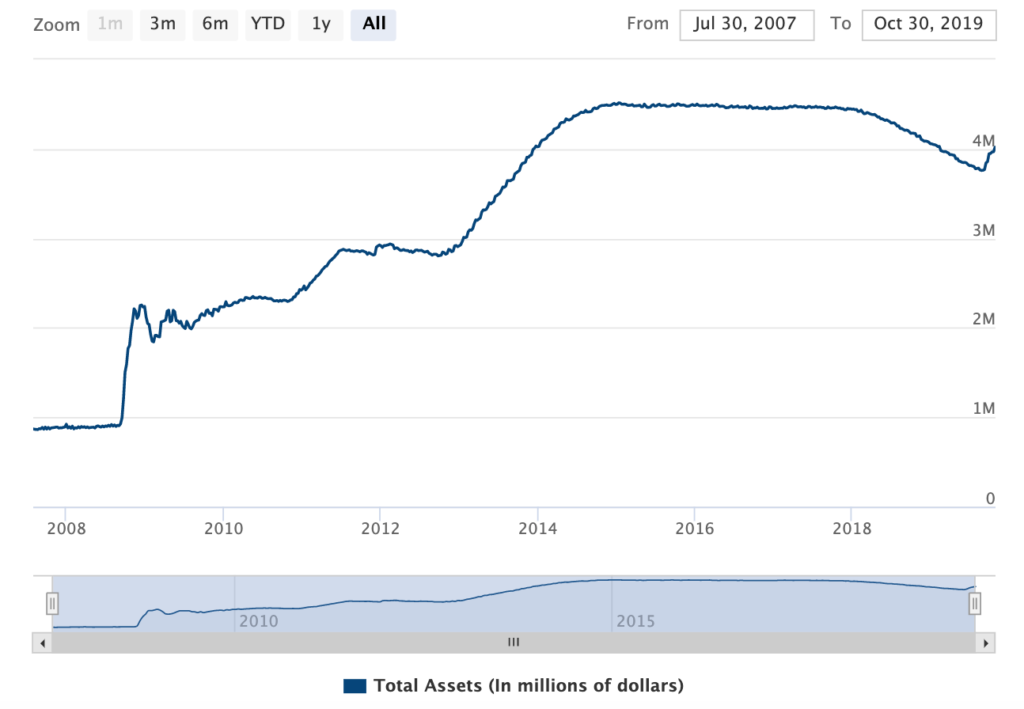

The Federal Reserve Balance sheet is back above $4 trillion for the first time since February of 2019.

This is more evidence that the US Government will monetize the national debt.

Monetizing the debt is when the government conjures money out of thin air “expanding the money supply” (in what amounts to legal counterfeiting) in order to pay the money it owes.

Monetizing the debt this puts downward pressure on the value of dollars and hence makes everything more expensive in what is described as price inflation, all else equal.

Is the Fed Monetizing the Debt?

The Federal Reserve has indicated that it would not monetize government debt.

“The Federal Reserve will not monetize the debt.” – Fed Chair Ben Bernanke

The reasoning goes that because they intend to shrink their balance sheet they aren’t just conjuring money created out of thin air.

But this is dependent on balance sheet normalization. Indeed, starting under Fed Chair Janet Yellen and accelerating under Fed Chair Jerome Powell the balance sheet had been trending down from the January 2015 high–at least until August 2015.

But as of 28 October 2019 the Fed’s balance sheet is back above $4 trillion. As humans we tend to place greater significance on large whole numbers when in fact there is nothing special about $4 trillion. But the point is that the Federal Reserve balance sheet began to tick back up starting in September of 2019.

Was the balance sheet declining from $4.5 trillion in January of 2015 down to $3.7 trillion in August of 2015 the extent of the “normalization” process?

The S&P 500 is making all time highs, everything is supposed to be wonderful in the economy, and yet starting back in September the Fed’s balance sheet is growing again, quite rapidly in fact as evidenced by the steepness of the chart.

How can the Fed ever normalize if they can’t do it after 10 years of stock market growth?

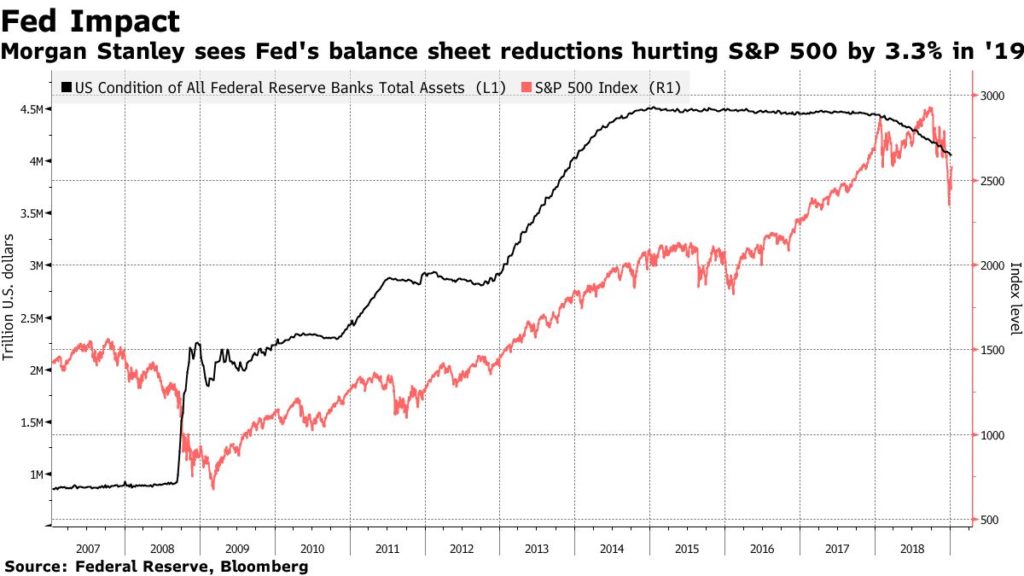

The above chart only goes through 2018. But it does show that the Fed’s balance sheet is correlated with the S&P 500. Despite the balance sheet tapering off slightly from 2016 onward through mid 2018 the S&P 500 continued to grow, until it sold off rather significantly in December.

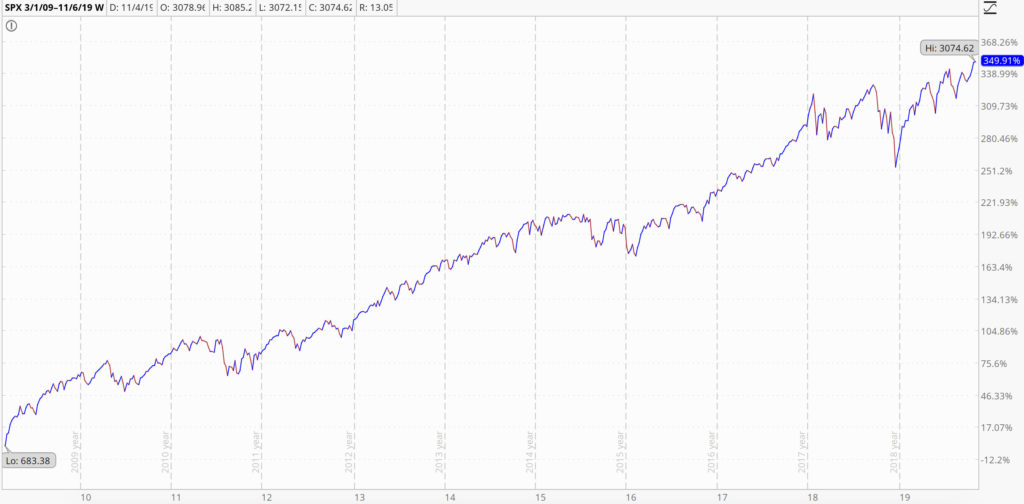

Since December the S&P 500 has rallied back and achieved new highs. All told, the S&P 500 has gone up nearly 350% since the March 2009 lows.

An intrepid investor who purchased the S&P 500 in the dark days of March 2009 would have done very well. However, I believe this artificial “growth” is really a bubble blown by the Federal Reserve.

If this “growth” has been fueled by the Fed’s monetary policy, then the Fed can’t even normalize without also tanking the markets.

Combine this with trillion dollar annual budget deficits and $23 trillion in national debt, the US simply doesn’t have any ammunition to fight the next economic downturn, at least not without seriously compromising the value of the dollar.

Source: https://usdebtclock.org/

US stocks have been the investment strategy for the past ten years. But this is the longest period of economic expansion in the history of the United States.

One of my twitter followers “W.C. Varones” (I am one of his followers as well!) responded to my Roth versus pre-tax 401(k) article and purported a Roth 401(k) was better even if the tax rates are the same.

I initially balked at this since it defied what I’d been taught in school and even my own prior analysis.

But after crunching the numbers to disprove this argument I realized the following:

Even assuming the tax rates are the same at the time of the contributions and distributions there are more tax savings with a Roth because you aren’t getting taxed on your compounded gains.

Put another way, with a 401(k) the money is taxed after it has grown in a compound fashion. With a Roth the money is taxed before it goes through compound growth. So if you max out a Roth 401(k) you end up being able to save more compared to the same amount in a pre-tax account.

The Scenario

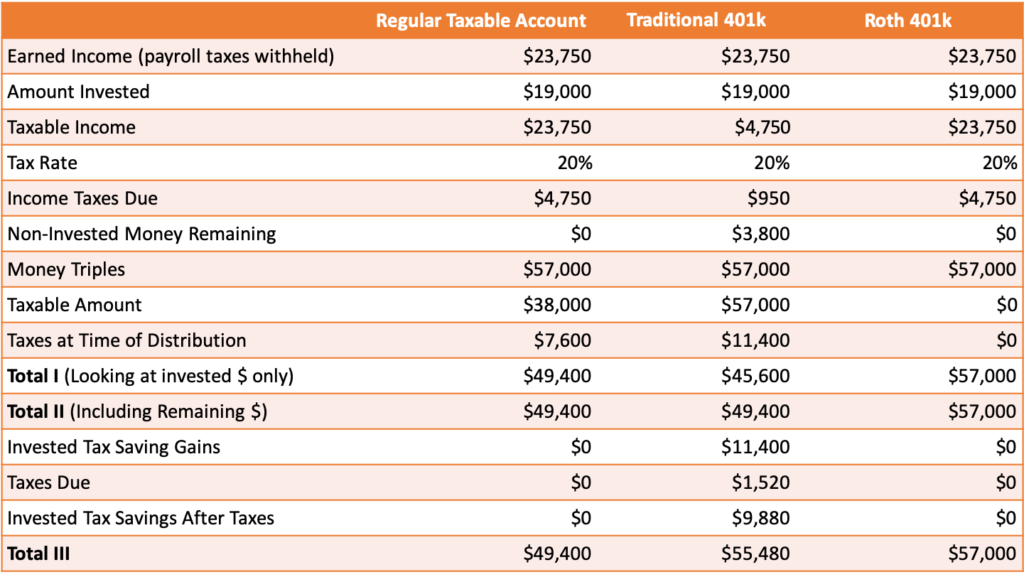

In 2019 if you aren’t eligible for the catch up provisions you can invest a maximum of $19,000 in a 401(k) (Roth, pre-tax or a mix of both).

Say there are three people each committed to saving $19,000 for retirement.

Person A the “Roth investor” chooses to contribute their $19,000 in a Roth 401(k). Person B the “pre-tax investor” contributes to a pre-tax 401(k). Person C the “non-retirement investor” who forgoes any tax-advantaged retirement account and saves for retirement in a brokerage account.

Because of taxes (we’ll assume a 20% tax bracket both now and in retirement) one needs to earn $23,750 worth of income in order to invest $19,000 .

Note: I’m excluding payroll taxes since they are always owned at the time the income is earned and add unnecessarily complexity that has no impact on the conclusion.

We’ll also assume the money triples between now and retirement. All other factors about these individuals are the same.

Total I: The Basic Scenario

Fast forward to retirement the Roth investor has $57,000 and owes uncle Sam nothing. The pre-tax investor also has $57,000 but they owe uncle Sam $11,400 in taxes, so in retirement they’d be left with just $45,600. See “Total I” below.

Interestingly the non-retirement account investor has more than the pre-tax investor ($49,400 versus $45,600). This is because they were able to count the $19,000 cost basis whereas the cost basis of a pre-tax 401(k) is zero.

So the Roth investor is the clear winner!

Total II: Accounting for pre-tax Savings

One objection is the $19,000 saved in the Roth was an additional $19,000 taxed at 20%. So the Roth investor (as well as the non-retirement account investor) paid $3,800 in taxes they don’t have today. This is true and it does make a difference.

The Pre-tax investor has $57,000 in their 401(k) minus the $11,400 they owe in taxes plus the $3,800 they saved in taxes or $49,400.

So even when we account for the additional taxes paid by the non pre-tax investors, Roth still appears to be the way to go. See “Total II” below for these numbers laid out.

However, at this point, we can see that the pre-tax 401(k) is at least as good as the non-tax advantaged account.

Total III: Investing the pre-tax 401(k) Savings

But what if pre-tax investor used that $3,800 to buy a non-dividend paying stock, and held that stock until retirement? The $3,800 triples to $11,400, they sell in retirement and have to pay 20% capital gains tax rate on $7,600 in gains so they owe $1,520 to uncle, leaving them with an additional $9,880 to enjoy in retirement.

Wearing the black gloves, Roth has landed the knock-out blow on the pre-tax 401(k): Roth wins

So at this point the pre-tax Investor effectively has $55,480, compared to the Roth Investor who has $57,000.

See “Total III” below.

Both the tax-advantaged investors did better than the non-retirement account investor who has just $49,400.

Even when we account for the pre-tax savings, and even if those savings were invested, the Roth investor still wins.

The reason my prior analysis concluded a pre-tax 401k was equal to a Roth 401(k) is because I assumed the additional taxes reduced the amount saved in the Roth.

When you max out the Roth and save the same amount as a hypothetical pre-tax 401(k), the Roth still wins.

A Roth is Better Under a Specific Scenario

There are a lot of variables and depending on what assumptions you make the Roth could look better than a traditional pre-tax 401(k) or vice versa.

If you are in a lower tax bracket in retirement than when you were saving for retirement then a pre-tax 401(k) would be better.

But if tax rates are the same, and the return is the same, the Roth does have an advantage if you contribute the same amount. The Roth has an advantage even if you invest the tax savings of a pre-tax 401(k).

If I changed the scenario to say the 401(k) tax savings was invested in a high yield dividend paying stock with no dividend reinvestment the taxes on the invested 401(k) savings would be higher and would be due each year the dividend was paid.

Another big advantage to 401(k)s not shown here is that if you rebalance a portfolio (or own investments that pay dividends) those actions are irrelevant in a 401(k) or IRA. However, in a non-retirement account each time a stock is bought or sold, taxes will be due. When dividends are paid, taxes will be due. A retirement account allows savings to continue to grow without

A lot depends on an individual’s tax situation. Unless you are retiring today you don’t know what the tax rate is going to be when you retire. You do know how much money you make, what tax bracket you’re in based on your income and how much you can contribute to tax-advantaged retirement accounts.

$57,000 Roth is worth more than $57,000 in a pre-tax 401(k)

A car with a lien on it is worth less than a car paid in full. So $19,000 in a 401(k) is worth less than $19,000 in a Roth 401(k) because the withdrawals from the traditional 401(k) are subject to income taxes.

This is somewhat obvious but it is important to keep in mind that you owe taxes on your pre-tax retirement savings.

If you invest the tax savings from a pre-tax 401(k) it does narrow the gap but the Roth is still better.

But I doubt most people have the discipline to narrow the gap by saying, “I saved $3,800 in taxes by maxing out my 401(k) so I’m going to put it in this non-retirement account and tag it for retirement.”

In the real world people who contribute to a Roth 401(k) probably have more saved for retirement than people who save in a 401(k) because the people with a 401(k) are probably not earmarking the tax savings for retirement as well.

There are probably a lot of people who don’t even have non-retirement accounts and their employer sponsored 401(k) are their only stock market investments. In this scenario saving in a Roth 401(k) is effectively saving more for retirement for the reasons stated above.

I already preferred a Roth IRA/401(k) to a pre-tax account and now I prefer it even more! Not only does a Roth allow me to save more for retirement, but I think tax rates will be higher in the future and I like knowing how much I have saved for retirement without having to factor in how much the government will take when I make a withdrawal.

I do invest in a 401(k) if it can reduce my taxable income and get me into a lower tax bracket. Pre-tax savings also provides tax diversification which is important when I don’t know what my future tax situation will be in retirement.

If ever there was a case study on the advantages of name recognition and first mover it is Bitcoin. There are dozens if not hundreds of altcoins technologically superior to Bitcoin, that have a market cap significantly lower than Bitcoin. Some of the major Bitcoin flaws I see are the following:

Bitcoin is slow, taking a minimum of 10 minutes per transaction but realistically at least 20 or more minutes.

Bitcoin transactions are expensive

It is energy intensive

Source: bitcoinfees.info

Let’s say you want to use Bitcoin to buy a $2 cup of coffee. You’re going to have to pay $0.36 cents, wait 10 minutes for the transaction to get picked up, and nearly all vendors require 1-2 transaction confirmations to prevent double-spending. It doesn’t work practically speaking.

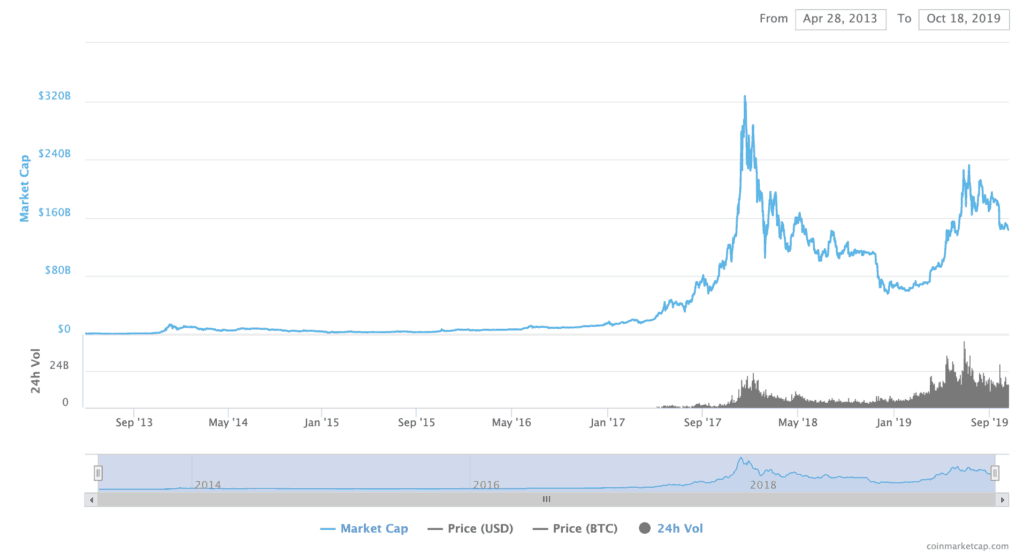

And yet the Market Capitalization of Bitcoin is over $143 billion. The next closest cryptocurrency, Ethereum, doesn’t come close, having a market cap of $18.8 billion.

The price and Market Capitalization of Bitcoin peaked in December of 2017. The market cap was as high as $327.1 billion on the 16th of December.

Bitcoin was groundbreaking and truth be told I still own some Bitcoin. But I believe that if another cryptocurrency took its place as the biggest crypto by market cap it would be a good thing. I’m calling for the death of Bitcoin.

I also think this provides an investing opportunity, or perhaps more realistically, a speculative opportunity. There are a variety of other cryptocurrencies that excel far beyond Bitcoin in a variety of ways, be it speed, security, anonymity, energy efficiency, user-friendliness, the list goes on.

I think this provides a speculative opportunity. Cryptocurrencies like EOS or other projects with real-world use cases could go up dramatically in value. There are hundreds of cryptocurrencies and a lot of them will probably be worth very little in the mid to long term.

It’s worth educating yourself on the various cryptocurrencies projects apart from Bitcoin. It might be worth investing in a few if you think they could have future promise.

Coinbase has a program that allows you to learn about various cryptocurrencies and earn free crypto at the same time. My referral link for EOS can be found here coinbase.com/earn.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.