A Roth 401(k) is Better

One of my twitter followers “W.C. Varones” (I am one of his followers as well!) responded to my Roth versus pre-tax 401(k) article and purported a Roth 401(k) was better even if the tax rates are the same.

I initially balked at this since it defied what I’d been taught in school and even my own prior analysis.

But after crunching the numbers to disprove this argument I realized the following:

Even assuming the tax rates are the same at the time of the contributions and distributions there are more tax savings with a Roth because you aren’t getting taxed on your compounded gains.

Put another way, with a 401(k) the money is taxed after it has grown in a compound fashion. With a Roth the money is taxed before it goes through compound growth. So if you max out a Roth 401(k) you end up being able to save more compared to the same amount in a pre-tax account.

The Scenario

In 2019 if you aren’t eligible for the catch up provisions you can invest a maximum of $19,000 in a 401(k) (Roth, pre-tax or a mix of both).

Say there are three people each committed to saving $19,000 for retirement.

Person A the “Roth investor” chooses to contribute their $19,000 in a Roth 401(k). Person B the “pre-tax investor” contributes to a pre-tax 401(k). Person C the “non-retirement investor” who forgoes any tax-advantaged retirement account and saves for retirement in a brokerage account.

Because of taxes (we’ll assume a 20% tax bracket both now and in retirement) one needs to earn $23,750 worth of income in order to invest $19,000 .

Note: I’m excluding payroll taxes since they are always owned at the time the income is earned and add unnecessarily complexity that has no impact on the conclusion.

We’ll also assume the money triples between now and retirement. All other factors about these individuals are the same.

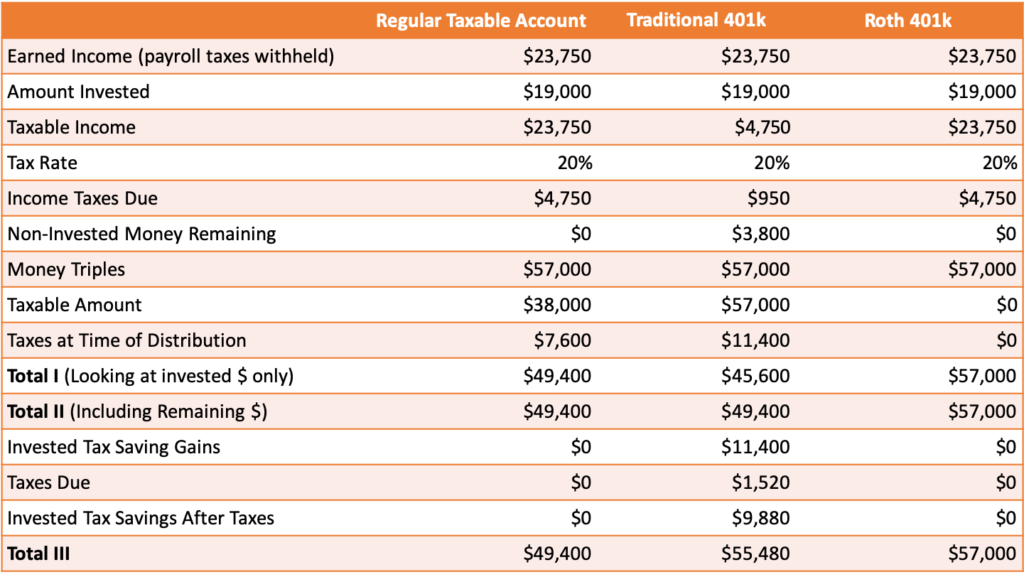

Total I: The Basic Scenario

Fast forward to retirement the Roth investor has $57,000 and owes uncle Sam nothing. The pre-tax investor also has $57,000 but they owe uncle Sam $11,400 in taxes, so in retirement they’d be left with just $45,600. See “Total I” below.

Interestingly the non-retirement account investor has more than the pre-tax investor ($49,400 versus $45,600). This is because they were able to count the $19,000 cost basis whereas the cost basis of a pre-tax 401(k) is zero.

So the Roth investor is the clear winner!

Total II: Accounting for pre-tax Savings

One objection is the $19,000 saved in the Roth was an additional $19,000 taxed at 20%. So the Roth investor (as well as the non-retirement account investor) paid $3,800 in taxes they don’t have today. This is true and it does make a difference.

The Pre-tax investor has $57,000 in their 401(k) minus the $11,400 they owe in taxes plus the $3,800 they saved in taxes or $49,400.

So even when we account for the additional taxes paid by the non pre-tax investors, Roth still appears to be the way to go. See “Total II” below for these numbers laid out.

However, at this point, we can see that the pre-tax 401(k) is at least as good as the non-tax advantaged account.

Total III: Investing the pre-tax 401(k) Savings

But what if pre-tax investor used that $3,800 to buy a non-dividend paying stock, and held that stock until retirement? The $3,800 triples to $11,400, they sell in retirement and have to pay 20% capital gains tax rate on $7,600 in gains so they owe $1,520 to uncle, leaving them with an additional $9,880 to enjoy in retirement.

So at this point the pre-tax Investor effectively has $55,480, compared to the Roth Investor who has $57,000.

See “Total III” below.

Both the tax-advantaged investors did better than the non-retirement account investor who has just $49,400.

Even when we account for the pre-tax savings, and even if those savings were invested, the Roth investor still wins.

The reason my prior analysis concluded a pre-tax 401k was equal to a Roth 401(k) is because I assumed the additional taxes reduced the amount saved in the Roth.

When you max out the Roth and save the same amount as a hypothetical pre-tax 401(k), the Roth still wins.

A Roth is Better Under a Specific Scenario

There are a lot of variables and depending on what assumptions you make the Roth could look better than a traditional pre-tax 401(k) or vice versa.

If you are in a lower tax bracket in retirement than when you were saving for retirement then a pre-tax 401(k) would be better.

But if tax rates are the same, and the return is the same, the Roth does have an advantage if you contribute the same amount. The Roth has an advantage even if you invest the tax savings of a pre-tax 401(k).

If I changed the scenario to say the 401(k) tax savings was invested in a high yield dividend paying stock with no dividend reinvestment the taxes on the invested 401(k) savings would be higher and would be due each year the dividend was paid.

Another big advantage to 401(k)s not shown here is that if you rebalance a portfolio (or own investments that pay dividends) those actions are irrelevant in a 401(k) or IRA. However, in a non-retirement account each time a stock is bought or sold, taxes will be due. When dividends are paid, taxes will be due. A retirement account allows savings to continue to grow without

A lot depends on an individual’s tax situation. Unless you are retiring today you don’t know what the tax rate is going to be when you retire. You do know how much money you make, what tax bracket you’re in based on your income and how much you can contribute to tax-advantaged retirement accounts.

$57,000 Roth is worth more than $57,000 in a pre-tax 401(k)

A car with a lien on it is worth less than a car paid in full. So $19,000 in a 401(k) is worth less than $19,000 in a Roth 401(k) because the withdrawals from the traditional 401(k) are subject to income taxes.

This is somewhat obvious but it is important to keep in mind that you owe taxes on your pre-tax retirement savings.

If you invest the tax savings from a pre-tax 401(k) it does narrow the gap but the Roth is still better.

But I doubt most people have the discipline to narrow the gap by saying, “I saved $3,800 in taxes by maxing out my 401(k) so I’m going to put it in this non-retirement account and tag it for retirement.”

In the real world people who contribute to a Roth 401(k) probably have more saved for retirement than people who save in a 401(k) because the people with a 401(k) are probably not earmarking the tax savings for retirement as well.

There are probably a lot of people who don’t even have non-retirement accounts and their employer sponsored 401(k) are their only stock market investments. In this scenario saving in a Roth 401(k) is effectively saving more for retirement for the reasons stated above.

I already preferred a Roth IRA/401(k) to a pre-tax account and now I prefer it even more! Not only does a Roth allow me to save more for retirement, but I think tax rates will be higher in the future and I like knowing how much I have saved for retirement without having to factor in how much the government will take when I make a withdrawal.

I do invest in a 401(k) if it can reduce my taxable income and get me into a lower tax bracket. Pre-tax savings also provides tax diversification which is important when I don’t know what my future tax situation will be in retirement.