One of my twitter followers “W.C. Varones” (I am one of his followers as well!) responded to my Roth versus pre-tax 401(k) article and purported a Roth 401(k) was better even if the tax rates are the same.

I initially balked at this since it defied what I’d been taught in school and even my own prior analysis.

But after crunching the numbers to disprove this argument I realized the following:

Even assuming the tax rates are the same at the time of the contributions and distributions there are more tax savings with a Roth because you aren’t getting taxed on your compounded gains.

Put another way, with a 401(k) the money is taxed after it has grown in a compound fashion. With a Roth the money is taxed before it goes through compound growth. So if you max out a Roth 401(k) you end up being able to save more compared to the same amount in a pre-tax account.

The Scenario

In 2019 if you aren’t eligible for the catch up provisions you can invest a maximum of $19,000 in a 401(k) (Roth, pre-tax or a mix of both).

Say there are three people each committed to saving $19,000 for retirement.

Person A the “Roth investor” chooses to contribute their $19,000 in a Roth 401(k). Person B the “pre-tax investor” contributes to a pre-tax 401(k). Person C the “non-retirement investor” who forgoes any tax-advantaged retirement account and saves for retirement in a brokerage account.

Because of taxes (we’ll assume a 20% tax bracket both now and in retirement) one needs to earn $23,750 worth of income in order to invest $19,000 .

Note: I’m excluding payroll taxes since they are always owned at the time the income is earned and add unnecessarily complexity that has no impact on the conclusion.

We’ll also assume the money triples between now and retirement. All other factors about these individuals are the same.

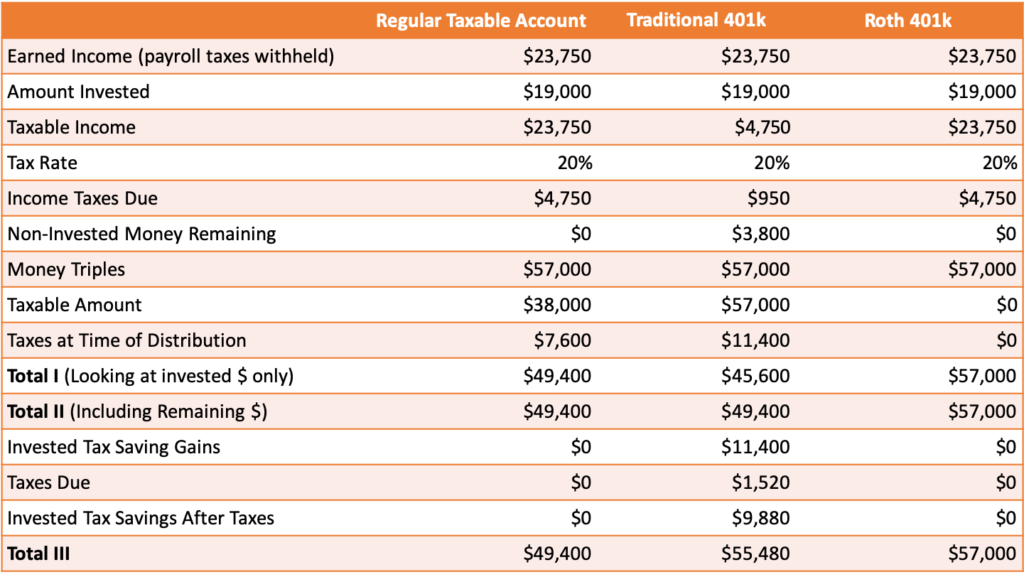

Total I: The Basic Scenario

Fast forward to retirement the Roth investor has $57,000 and owes uncle Sam nothing. The pre-tax investor also has $57,000 but they owe uncle Sam $11,400 in taxes, so in retirement they’d be left with just $45,600. See “Total I” below.

Interestingly the non-retirement account investor has more than the pre-tax investor ($49,400 versus $45,600). This is because they were able to count the $19,000 cost basis whereas the cost basis of a pre-tax 401(k) is zero.

So the Roth investor is the clear winner!

Total II: Accounting for pre-tax Savings

One objection is the $19,000 saved in the Roth was an additional $19,000 taxed at 20%. So the Roth investor (as well as the non-retirement account investor) paid $3,800 in taxes they don’t have today. This is true and it does make a difference.

The Pre-tax investor has $57,000 in their 401(k) minus the $11,400 they owe in taxes plus the $3,800 they saved in taxes or $49,400.

So even when we account for the additional taxes paid by the non pre-tax investors, Roth still appears to be the way to go. See “Total II” below for these numbers laid out.

However, at this point, we can see that the pre-tax 401(k) is at least as good as the non-tax advantaged account.

Total III: Investing the pre-tax 401(k) Savings

But what if pre-tax investor used that $3,800 to buy a non-dividend paying stock, and held that stock until retirement? The $3,800 triples to $11,400, they sell in retirement and have to pay 20% capital gains tax rate on $7,600 in gains so they owe $1,520 to uncle, leaving them with an additional $9,880 to enjoy in retirement.

Wearing the black gloves, Roth has landed the knock-out blow on the pre-tax 401(k): Roth wins

So at this point the pre-tax Investor effectively has $55,480, compared to the Roth Investor who has $57,000.

See “Total III” below.

Both the tax-advantaged investors did better than the non-retirement account investor who has just $49,400.

Even when we account for the pre-tax savings, and even if those savings were invested, the Roth investor still wins.

The reason my prior analysis concluded a pre-tax 401k was equal to a Roth 401(k) is because I assumed the additional taxes reduced the amount saved in the Roth.

When you max out the Roth and save the same amount as a hypothetical pre-tax 401(k), the Roth still wins.

A Roth is Better Under a Specific Scenario

There are a lot of variables and depending on what assumptions you make the Roth could look better than a traditional pre-tax 401(k) or vice versa.

If you are in a lower tax bracket in retirement than when you were saving for retirement then a pre-tax 401(k) would be better.

But if tax rates are the same, and the return is the same, the Roth does have an advantage if you contribute the same amount. The Roth has an advantage even if you invest the tax savings of a pre-tax 401(k).

If I changed the scenario to say the 401(k) tax savings was invested in a high yield dividend paying stock with no dividend reinvestment the taxes on the invested 401(k) savings would be higher and would be due each year the dividend was paid.

Another big advantage to 401(k)s not shown here is that if you rebalance a portfolio (or own investments that pay dividends) those actions are irrelevant in a 401(k) or IRA. However, in a non-retirement account each time a stock is bought or sold, taxes will be due. When dividends are paid, taxes will be due. A retirement account allows savings to continue to grow without

A lot depends on an individual’s tax situation. Unless you are retiring today you don’t know what the tax rate is going to be when you retire. You do know how much money you make, what tax bracket you’re in based on your income and how much you can contribute to tax-advantaged retirement accounts.

$57,000 Roth is worth more than $57,000 in a pre-tax 401(k)

A car with a lien on it is worth less than a car paid in full. So $19,000 in a 401(k) is worth less than $19,000 in a Roth 401(k) because the withdrawals from the traditional 401(k) are subject to income taxes.

This is somewhat obvious but it is important to keep in mind that you owe taxes on your pre-tax retirement savings.

If you invest the tax savings from a pre-tax 401(k) it does narrow the gap but the Roth is still better.

But I doubt most people have the discipline to narrow the gap by saying, “I saved $3,800 in taxes by maxing out my 401(k) so I’m going to put it in this non-retirement account and tag it for retirement.”

In the real world people who contribute to a Roth 401(k) probably have more saved for retirement than people who save in a 401(k) because the people with a 401(k) are probably not earmarking the tax savings for retirement as well.

There are probably a lot of people who don’t even have non-retirement accounts and their employer sponsored 401(k) are their only stock market investments. In this scenario saving in a Roth 401(k) is effectively saving more for retirement for the reasons stated above.

I already preferred a Roth IRA/401(k) to a pre-tax account and now I prefer it even more! Not only does a Roth allow me to save more for retirement, but I think tax rates will be higher in the future and I like knowing how much I have saved for retirement without having to factor in how much the government will take when I make a withdrawal.

I do invest in a 401(k) if it can reduce my taxable income and get me into a lower tax bracket. Pre-tax savings also provides tax diversification which is important when I don’t know what my future tax situation will be in retirement.

Roth IRA vs 401k: who will win? Both plans enable a person to save and invest for retirement in a tax advantaged way. What does tax advantaged mean? That you pay less taxes!

Taxes are a large cost when it comes to investing. In the United States long term investments (held 366 days or longer) are taxed at 15% for most people. For those in lower tax brackets long term capital gains are taxed at 0% and for those in the top tax bracket the IRS calls for a 20% cut.

So, if one has $20,000 in gains 15% would be $3,000. In another example $100,000 in gains would be $15,000 paid to the IRS. It’s not an inconsequential amount. Furthermore that amount of gains is very realistic, particularly over a long period of time, $10,000 invested over a period of 40 years with an 8% interest rate would grow to over $217,000.

Fortunately there are ways to shield long term retirement savings from these destructive taxes. One way is a 401(k) and another is an individual retirement account (IRA).

Traditional 401(k)s and IRAs

Many employers offer 401(k) plans. A 401(k) allows pre-tax money (money for which income tax hasn’t been paid) to be invested. Unfortunately the medicare and social security payroll taxes are still due. One can start taking money out of a 401(k) at age 59 and 1/2. Any distributions from a 401(k) (with some exceptions) prior to age 59 and 1/2 will result in taxes being due plus a 10% penalty.

No capital gains taxes are owed when the investments are sold and distributions are made but the money is taxed as ordinary income at the state and federal level.

The main advantage to a traditional 401(k) or IRA is that the money grows tax deferred and it is only taxed once. If one were to simply invest money from a paycheck without a retirement vehicle it would be first taxed at the Federal and State level and then any capital gains would be taxed as well.

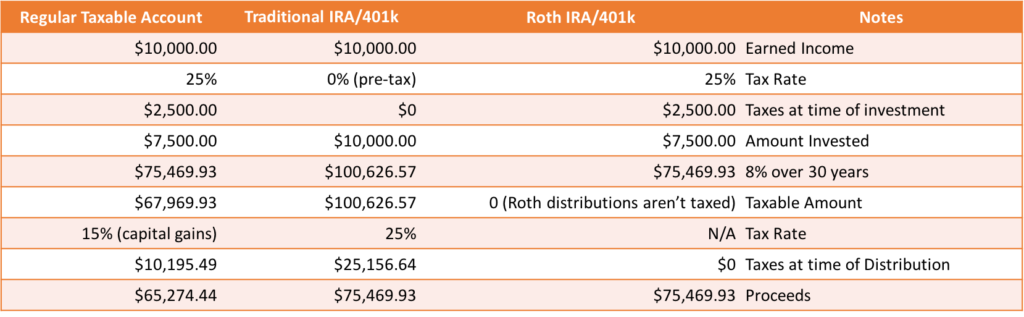

For example, if one were to allocate $10,000 from a paycheck to an IRA or 401(k) it would not be subject to any state or federal taxes. It would hopefully grow (lets say at 8% over 30 years). After 30 years it would have grown to $100,626.57 and all the money is withdrawn from the 401(k). At this point (assuming the person is over 59 and 1/2) the money would be taxed as ordinary income. Let’s assume for the purposes of this example it is taxed at the 25% tax bracket, and thus the IRS would be expecting $25,156.64. The total proceeds would be $75,469.93.

A traditional IRA would work the same way with an important caveat. Your employer isn’t aware of the IRA so you will be overpaying in your federal and state withholding taxes in each paycheck (and get a larger refund which I think is a BAD thing), because the income reduction won’t come until you file your taxes the following April. But you can compensate for this by increasing withholding allowances.

This brings up the secondary advantage of IRAs and 401(k)s: they allow you to reduce your taxable income. This can be particularly helpful if one is on the cusp of a tax bracket. For example, lets say you made $40,000 in otherwise taxable income in 2016. If you contributed $4,000 to a 401k, instead of having to pay 25% on the amount over $37,651, you’d be taxed no more than 15% on any earnings that year.

Roth 401(k)s and IRAs

Traditional 401(k)s and IRAs are not taxed initially, but are taxed when money is withdrawn. Roth IRAs and Roth 401(k)s work in reverse. You don’t get any tax benefits initially with a Roth 401(k) or Roth IRA. You use after tax money to save for retirement but you don’t have to pay any taxes on distributions.

If your tax bracket is the same when you put money in the IRA as when you withdraw the money, it doesn’t matter if you have a Roth IRA or a traditional IRA, the tax savings is going to be the same.

However, if you’re in a higher tax bracket later in life as compared to earlier in life, the Roth 401(k)/IRA is better because you can pay taxes at say 15 or 25%, invest the money, it grows tax free, then if you’re in a 35% tax bracket because you’ve made it big and you’re still working at age 59 and 1/2 you can withdraw that money and you don’t have to pay any additional taxes.

Conversely, if you’re in a lower tax bracket when you retire the traditional IRA or 401(k) is going to be better.

But because of the move towards a more socialized society and given the monstrous debt in the US I anticipate taxes will only go up in the future. So I’d rather pay them now when tax rates are lower.

The Advantage of an IRA or 401(k)

Let’s compare a Roth IRA/401(k), to a traditional IRA/401(k), to simply investing the money without a retirement savings vehicle in a regular taxable account. Let’s say you earned $10,000 of W2 income and want to invest all of it. I’m ignoring social security and medicare taxes because there is no way to avoid those on W2 income in the US, for all three scenarios they are due up front.

As you can see, if one is in the same tax bracket when the investment was made, as when the distributions are made, it doesn’t matter if one has a Roth or traditional 401k/IRA. But there is a $10,000 advantage over a non-tax advantaged brokerage account.

3 November 2019: However, this is only true when you assume that the loss of tax savings is taken out of the amount saved in a Roth IRA or 401(k). If the same amount is in both accounts the Roth IRA/401(k) is better.

Roth or Traditional?

I prefer after-tax, Roth IRAs/401(k)s in general but in specific circumstances using a pre-tax vehicle makes more sense. I like Roths because I can check the balance of my Roth IRA or Roth 401(k) and I know that is how much I would have access to when I achieve an age of 59 and 1/2. I don’t have to figure in taxes. I also hope to be making more when I’m 60 than I am now. Plus, I think taxes are going to be going up in order to pay for unfunded entitlement programs and to pay the national debt (not that I think it is repayable).

I also generally prefer IRAs versus 401(k)s of any kind because with an IRA you can choose a broker that has more investment options than the limited range of choices employer sponsored plans typically allow. Pretty much all the investment options I’ve seen for company sponsored 401(k)s are very limited and are focused in the US.

But I will use a traditional 401(k)/IRA under certain circumstances. 1) If I can use it to get to a lower tax bracket. 2) If my employer offers a 401(k) with company matching–I will contribute to the 401(k) until I’ve maxed out the employer match. 3) If I’ve already maxed out the Roth IRA contribution for the year ($5,500 for a single person under 50 years old in 2017) then I would consider contributing to a 401(k).

Wether you go with a Roth IRA or traditional IRA you can only contribute up to a combined total of $5,500 in 2017 if you’re under 50. If you’re 50 or over you can contribute $6,500.

For 401(k)s the 2017 contribution limit is $18,000 but goes up to $24,000 if you’re 50 or over.

So if you contribute to both a 401(k) and an IRA you could save a total of $23,500 in tax advantages funds ($30,500 if you’re 50 or older).

So in general I prefer Roth to traditional, and I prefer IRAs to 401(k)s. However, if my employer offers matching I take advantage of that.

SEPs, solo 401(k)s

There are other tax-advantaged ways to save for retirement, like a SEP or a solo 401(k). I haven’t taken advantage of these options but it is something I’m researching.

I think saving and investing for retirement is important. But there are some strong headwinds working against folks planning for retirement in the US: taxes reduce income and gains, pensions are becoming a thing of the past, Social Security is woefully underfunded, inflation ravages savings.

Tax-advantaged retirement savings vehicles like IRAs and 401(k)s provide needed advantages when it comes to investing for retirement. It’s important to understand how they work and to make use of the tax-advantaged benefits they provide when suitable.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.