by John | Sep 18, 2016 | Capital Appreciation, Investor Mindset, Investor Psychology, Tax Strategies, Value Investing

Warren Buffett is considered to be one of the most successful investors. He’s one of the wealthiest people in the world and he’s also fond of publicity and public appearances.

If you have some humility and don’t get caught up in jealousy you can learn a lot from wealthy and successful people like Warren Buffett.

My own Father is fond of saying that poor people should take rich people out to lunch. The idea being that the wisdom that can be gained from the wealthy is worth more than paying for lunch.

So what lessons can we learn from Warren Buffett?

Do As Warren Buffett Does, Not As He Says

There is an old expression “Do as I say, not as I do.” With Warren Buffett it is “Do as I do, not as I say.”

There is an old expression “Do as I say, not as I do.” With Warren Buffett it is “Do as I do, not as I say.”

Warren Buffett talks A LOT and shares a lot of opinions. But you shouldn’t follow what he says as advice because he might actually be doing the opposite of what he is saying.

In order to learn lessons from Buffett one must first filter out a lot of what he says.

There is a quote from Daniel Loeb that summarizes Buffett’s contradictions quite succinctly.

“He criticises hedge funds yet he really had the first hedge fund,” Loeb said. “He criticises activists. He was the first activist. He criticises financial service companies, yet he likes to invest in them. He thinks that we should all pay more taxes but he loves avoiding them himself.”

Source: http://www.smh.com.au/business/warren-buffett-is-full-of-contradictions-hedge-funds-say-20150507-ggwv2o.html

Without further ado here are three lessons we can learn from Warren Buffett.

Lesson 1: Reduce Your Taxes

While publicly discussing how he wants to pay more taxes Warren Buffett has taken extraordinary steps to reduce his taxes.

Source: http://www.nytimes.com/2011/08/15/opinion/stop-coddling-the-super-rich.html

From how he structures his businesses to how he is paid to how he has bequeathed his inheritance Warren Buffett does all he can to reduce his taxes. He gets paid through dividends and long term capital gains rather than ordinary income. He’s also left 99% of his fortune to a private charity to avoid paying inheritance taxes.

Lesson number one from Warren Buffett is Reduce Your Taxes.

There are a variety of ways you can legally reduce your taxes: IRAs, 401ks, FSA, HSAs, charitable contributions, capital gains. I discuss some of them in Five Tax Strategies to Keep More Income.

Real estate is also an excellent way to increase your wealth in a tax advantaged way. BiggerPockets.com is an excellent Real Estate resource.

Lesson 2: Invest in High Quality Companies that are Undervalued

Warren Buffett loves great value. Much of his investing philosophy can be traced back to Benjamin Graham, the father of value investing.

According to Investopedia Buffett looks at six criteria for stock investments:

1. Has the company consistently performed well?

2. Has the company avoided excess debt?

3. Are profit margins high? Are they increasing?

4. How long has the company been public?

5. Do the company’s products rely on a commodity?

6. Is the stock selling at a 25% discount to its real value?

Source: http://www.investopedia.com/articles/01/071801.asp

Warren Bueffett is a value investor and I think value investing is an excellent way for the enterprising investor to achieve outsized returns. I’ll be writing more about value investing in future posts.

If you’re interested in reading one of Graham’s seminal works “The Intelligent Investor” use this link to buy it on Amazon and help support this site: The Intelligent Investor by Benjamin Graham. Buffet calls it “the best investing book ever written.”

Lesson 3: Use Derivatives Wisely

Warren Buffett has written “derivatives are financial weapons of mass destruction.”

Source: http://www.fintools.com/docs/Warren%20Buffet%20on%20Derivatives.pdf

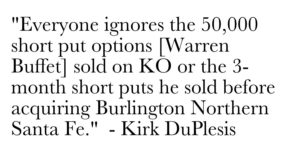

But Buffett has billions in derivatives as pointed out by Kirk DuPlesis of OptionAlpha.com.

Source: https://optionalpha.com/warren-buffett-options-trading-strategy-19655.html

In the article above Kirk talks about two ways Buffett uses derivatives:

1) Uses naked, short puts to lower the cost basis for purchasing stock or target companies that he wants to acquire.

2) Sells short index put options when volatility is at it’s highest, knowing that volatility is the one factor that is overpriced all the time.

I’ve written about trading options and think that done correctly it can be an excellent way to bring in monthly income. I’m interested in utilizing strategy one above more often as I open new stock positions.

Lessons from Warren Buffett

Those are three lessons I’ve learned from looking at what Buffett does, not what he says. Buffett probably gives some advice that is worth following directly but you have listen through a filter and weigh heavily what he actually does over his words.

by John | Sep 11, 2016 | Capital Appreciation, Getting Started, Passive Income, Preservation of Purchasing Power, Tax Strategies

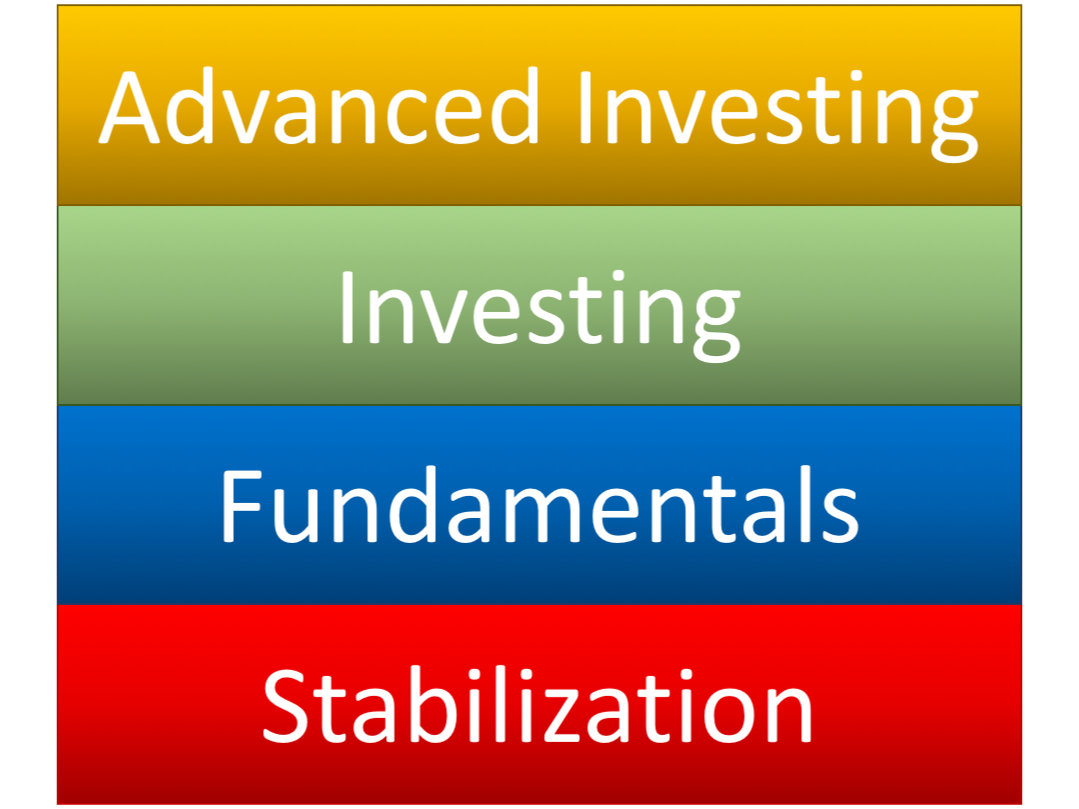

The Building Blocks of Personal Finance

If you haven’t already read parts I and II start there!

I visualize personal finance as building blocks stacked on top of each other (shown to the right).

You must master the lower levels before you can get to the upper levels.

Level 3: Basic Investing

I consider basic investing saving for retirement in a 401k and Individual Retirement Account (IRA) via mutual funds and bonds, and general savings in mutual funds.

Both the 401k and IRA are ways to invest for retirement and get some tax benefits. 401ks are through an employer, and IRAs can be setup through a company like Vanguard, Fidelity, TD Ameritrade, or any number of other firms that act as the “custodian”. I talk about them in a little more detail in my article Five Tax Strategies to Keep More Income under strategies one and two.

Employer Matching 401k

Some employers will match your 401k contributions. As an example lets say your employer matches your contributions up to 5% of your salary. If you make $50,000, and you save $2,500 in your 401k, your employer will add an additional $2,500 to your 401k. I put money in my 401k up to but not beyond the point where I’ve maxed out the match.

Some employers will match your 401k contributions. As an example lets say your employer matches your contributions up to 5% of your salary. If you make $50,000, and you save $2,500 in your 401k, your employer will add an additional $2,500 to your 401k. I put money in my 401k up to but not beyond the point where I’ve maxed out the match.

I prefer Roth 401ks to 401ks because I believe tax rates are going up in the future. Roth 401ks are more rare but I have had employers who offer them.

The vast majority of the investment options offered by the employers I’ve been at are VERY limited. The easiest option is to go with a target retirement fund. Target retirement funds are basically funds on autopilot, they automatically adjust their asset mixes to become more conservative as investors approach the target retirement date.

If there are more options I avoid bonds and favor international funds but investments depend on your risk tolerance and goals.

Individual Retirement Accounts

IRA’s come in the Roth and Traditional flavor. It all depends if you’d rather pay taxes now, or in retirement. I prefer to pay the taxes up front.

I would open up a Roth IRA and try to max it out ($5,500 in 2016). Another neat trick is that you can contribute to a traditional IRA and then convert contributes to a Roth (you do of course have to pay the taxes though), so if you want to save more than $5,500 in after tax income, that is an option.

One of the things I like about IRAs is that the investment options are much, much more flexible. I think part of the reason employer sponsored 401ks have such limited investment options is because employers are afraid of being sued if an employee makes poor decisions and loses a lot of money, so employers only offer with the most conservative investment options.

If you want to save money and not think about, you’re asking for trouble, but one option is to open up an account at a low cost company like Vanguard (my favorite) or Fidelity. Setup auto-deposit and buy a balanced fund like the Vanguard STAR fund (VGSTX).

You can also buy additional index funds, like the S&P 500 index fund, Nasdaq, large and small cap US funds, etc. These index mutual funds are setup to track the gains and losses of the index they are based on. Again, I think it is good to have money in the emerging markets as well.

Vanguard has investment professionals that will help you decide how to allocate money to different mutuals funds. (Disclosure: I have been a vanguard client for years, but gain no benefit from listing them as an option).

By setting up auto-deposit and auto-invest into Vanguard (or your IRA custodian of choice) from your paycheck you’re dollar cost averaging into the fund and not trying to time the market.

Over time this is a good, conservative strategy, and one discussed by Benjamin Graham in his seminal work “The Intelligent Investor”. Ben Graham was a mentor to Warren Buffet, who you may have heard of, and has done decently well as an investor.

Conventional wisdom is often something like a 40% bonds and 60% stocks (mutual funds) as a conservative approach. Unless you’re retired and relying on your savings for monthly income, I would not buy bonds, but a portfolio that does not include bonds is considered more risky.

You can follow these same investing principles to buy non-retirement mutual funds.

Now I do think that US stocks and bonds are in a bubble. But if the Federal Reserve responds to the bubble bursting as I think they will, stocks and bonds will still go up. I just think there are other asset classes that will go up faster.

Consider Physical Gold

Consider Physical Gold

While this could be considered more advanced, I think it is very important to have somewhere around 10% of one’s assets in physical gold and silver bullion. While I don’t give investment recommendations I think that even some of the more conservative and traditional investment advisors would admit this is not a bad idea. I gain no benefit from mentioning them, but I buy bullion from Scotsman Auction house in Saint Louis. They have been in business a long time and have great pricing. I don’t buy numismatics or “rare” coins as an investment. I’m partial to Silver American Eagles and Gold Canadian Maples, but that is just personal preference.

There are lots of gold bullion companies but I would not want to pay more than around 2% over spot price for gold. I avoid numismatics unless they can be acquired at bullion prices.

Level 4: Advanced Investing

Advanced Investing techniques are what I’m most passionate about. Examples of what I consider advanced investments are: Investing in individual company stocks, gold mining stocks, peer to peer lending, real estate investments, private equity, foreign stocks, offshore brokerage accounts, options, cryptocurrencies, physical precious metals like gold and silver, and physical gold stored remotely through a Goldmoney personal account.

Advanced Investing techniques are what I’m most passionate about. Examples of what I consider advanced investments are: Investing in individual company stocks, gold mining stocks, peer to peer lending, real estate investments, private equity, foreign stocks, offshore brokerage accounts, options, cryptocurrencies, physical precious metals like gold and silver, and physical gold stored remotely through a Goldmoney personal account.

These techniques are generally considered more risky, although I think that buying US stocks at all time highs and negative yielding bonds is much more risky, even though conventional foolishness wisdom says these are the safe bets.

Get Started!

To get started figure out where you stand in the four phases. Master that phase and work towards the next.

It’s an iterative process once you’re out of stabilization and focusing on the fundamentals and investing. I’m often re-evaluating my fundamentals such as my budget and my goals. I work on my basic investing like maxing out my 401k company match and Roth IRA.

Which phase are you in and what are your savings and investment goals?

by John | Jun 30, 2016 | Capital Appreciation, Geopolitical Risk Protection, Preservation of Purchasing Power, Value Investing

Trading Australian Stocks is fairly easy. You just need to have the right broker. Making profitable trades is a little harder. But before we get too far into brokers and trading you might be asking…

What is Special about Trading Australian Stocks?

The Australian Stock Exchange (ASX)

If you believe that US and European stocks are overvalued, as I do, and that gold mining stocks are undervalued, as I do, Australia presents, pardon the pun, a golden opportunity.

Australia is a stable jurisdiction that is gold mining friendly. It’s also relatively close to the biggest emerging markets in the world: India and China.

India and China are also some of the world’s largest purchasers of gold.

Why not just trade ADRs?

An ADR is defined by investopedia as follows:

An American depositary receipt (ADR) is a negotiable certificate issued by a U.S. bank representing a specified number of shares (or one share) in a foreign stock that is traded on a U.S. exchange. ADRs are denominated in U.S. dollars, with the underlying security held by a U.S. financial institution overseas.

Source: http://www.investopedia.com/terms/a/adr.asp

If the Australian stock you want to buy IS available as an ADR through your existing broker you can save yourself the trouble of opening a new brokerage account.

But there ARE advantages to owning a stock directly on the exchange (instead of buying the ADR).

1) It costs banks money to create ADRs and they sometimes keep part of the dividend to cover these costs (Peter Schiff, Crash Proof 2.0)

2) Trading stocks on the local exchange can be more liquid (Tim Price, Price Value International)

3) The only way you can acquire many excellent value stocks is to purchase them directly on their “native” exchange. So if you limit yourself to ADRs you’ll miss out on opportunities.

While I do make some of my own stocks picks I also rely on competent professionals that I trust.

Which brings me to…

Price Value International

One such expert I look to is Tim Price.

One such expert I look to is Tim Price.

Among many other accolades Tim boasts 25 years in the capital markets; 15 years as a discretionary multi-asset portfolio manager and was Chief Investment Officer at three successive firms. Tim is currently one of two principals at Price Value Partners and a columnist for MoneyWeek magazine.

Tim also has a monthly paid newsletter called Price Value International (PVI) in which he provides value stock picks of international companies. Tim hails from the UK which I believe helps adds to his unique perspective that is hard to find from asset managers closer to Wall Street.

I receive no financial benefit from Time Price or Price Value International by writing about his newsletter.

But I have been a Price Value International subscriber for over 10 months now and for me it has been worth every penny. As a result I want to share it with my readers.

You can sign up for the PVI newsletter at the following link: Price Value International.

Make Money Like Warren Buffet

Tim Price follows a methodology heavily influenced by “the father of value investing” Benjamin Graham. Graham developed investment strategies that Warren Buffet adopted to grow his fortune.

Using these methods Tim looks for high quality companies around the globe that trade close to or even less than their book value. It’s kind of like buying a house for $190,000, when building the same house would cost $200,000. Value investing provides built in downside protection and is a proven investing method.

Through the Price Value International newsletter Tim shares a new value stock recommendation each month. When you sign up you also get access to back issues so you can see recommendations from prior months.

The stocks range from firms throughout the world and two of them are traded on the Australian Stock Exchange.

I’d love to share the names of these stocks (both of which I own) but it would not be right to do so since I learned about them from Tim through his Price Value International newsletter.

But if you do sign up for PVI and/or decide you want to trade stocks on the Aussie stock exchange, I can provide you with the name of…

A Broker that allows you to trade directly on the Australian Stock Exchange

Most foreign brokers don’t accept US clients largely because of the onerous US laws foreign brokers would have to comply with if they did allow US citizens.

However, I’ve found a US based broker that allows you to trade directly on the Australian Stock Exchange.

This allows me to purchase an Australian stock recommended by Tim Price that I know for a fact is not available as an ADR.

This broker has no minimum account balance which is great if you don’t have a lot of capital to invest.

I DON’T get anything if you sign up for an account with this broker. It’s a firm that I personally have an account with and find valuable.

What is the name of the Broker?

I AM trying to gain more subscribers to my own FREE email newsletter where I talk about what I’m doing to grow my wealth. So while I’m more than happy to provide the name of the broker at no cost, in return I just ask that you sign up for the How I Grow My Wealth email Newsletter using the form below.

Again, out of respect for Tim I’m not going to share the name of any of his stock recommendations. Plus he might cancel my subscription and then I’ll miss out!

But I am happy to share the name of broker that I use.

I was able to start trading Australian stocks quickly. It took me less than a week to get my account setup and make my first trade.

To get instant access to the name of this broker simply sign up for my free email newsletter using the form below.

by John | Jun 16, 2016 | Capital Appreciation, Passive Income, Preservation of Purchasing Power, Real Estate

Buying Rental Property and Real Estate has helped create many a millionaire. Robert Kiyosaki, Barbara Corcoran, and even Donald Trump amassed fortunes via Real Estate.

Buying rental property is an investment that hits on three out of five of my Investment Goal Categories: Capital Appreciation, Preservation of Purchasing Power and Passive Monthly Income.

At it’s most basic level, investing in rental property consists of buying a property and then renting it out to gain monthly income.

I don’t directly own any rental property at this time but it is an area I’m investigating and learning more about.

Buying Rental Property has Five Great Benefits

1) Passive Monthly Income (Cashflow)

2) Equity Build-Up

3) Leverage Utilization

4) Very Favorable Tax Benefits (in the US)

5) Appreciation

Let’s explore the five benefits of buying rental property.

Passive Monthly Income

In many areas it’s feasible to purchase a rental property that generates positive cashflow each month. Even after making a monthly mortgage payment, taxes, fees and maintenance expenses, a good rental property can be have net positive cashflow from the rent payments of the tenants.

In many areas it’s feasible to purchase a rental property that generates positive cashflow each month. Even after making a monthly mortgage payment, taxes, fees and maintenance expenses, a good rental property can be have net positive cashflow from the rent payments of the tenants.

This meets one of my investment goal categories of passive monthly income.

Equity Build-up

Many banks will loan qualified persons enough money to purchase a rental property but typically require a 20-30% down payment. By renting the property you can use the rental income to pay the mortgage and continue to build equity in the property until you own it outright.

With equity in a property you have the option to choose between selling the property, taking a loan out on the property and re-mortgage it, or simply hold onto the property and continue to enjoy the monthly income.

Leverage Utilization

By taking out a loan to buy a positive cashflow rental property you are leveraging the capital you have to make more money. For example by using $16,000 for a down payment you could purchase an $80,000 property and rent it for $600 per month. Lets say after making the mortgage payments, paying property taxes, and other expenses, you are bringing in $150 per month in cashflow. At the end of the year that $150 monthly income would be $1,800 from a $16,000 investment, or over an 11% return. And that doesn’t even include the increase in equity.

Because of the use of leverage, price inflation actually reduces the cost of the remaining loan balance over time. This combined with the universal human need (and hence demand) for shelter even when the economy is not performing well makes buying rental property a great investment for preserving purchasing power.

Tax Benefits

I’m not a CPA or tax advisor, but I understand that when it comes to investment properties, mortgage interest, depreciation of the property, and other expenses that go into maintaining the property are tax deductible. Often times the 11% profit can be made tax free because of all the deductions the tax code (at least in the US) provides to real estate investors.

Appreciation

Partly due to price inflation, partly due to an increasing population and demand for housing, real estate prices tend to rise. So it is possible to grow wealth because the value of the property has gone up. While this is more on the speculative side of the housing and real estate market, appreciation can be a very nice bonus.

This meets one of my investment goals of capital appreciation as well as preservation of purchasing power.

What has stopped me from Buying Rental Property in the past?

- Capital I need money for a down payment. Most of my savings go into stocks and I want to buy a rental property with new money. So I’m going to start earmarking money for buying rental property. While it might be possible to buy a property with zero down I think this is reckless and irresponsible. It’s a good way to find yourself underwater on your mortgage. By making a 20% down payment you can weather a 20% drop in the value of the property and still be even in terms of equity. Plus if the property is cashflow positive, even if you are not making money via appreciation, you can still make money via cashflow and equity building.

- Knowing how to make an offer I would like to better learn how to coordinate having a loan pre-approved with making the offer. With real estate you have to be able to move quickly. In some markets if you go eat lunch to think it over the property will be sold by the time you get back.

- Maintenance Costs and Expenses If you know purchase price of a property and how much you can rent it for (by looking at similar properties being advertised in the same area) and what your costs are going to be you can determine if a property will be profitable (or not). However, I find the most difficult part to research is estimating maintenance costs. The hot water heater breaks, furnace needs repair, a crazy tenant tears up the place, etc. As someone who has been a renter all his life I don’t have a good sense of how much I need to budget for maintenance costs for a rental property. These costs are a huge factor in the profit and loss calculations.

There are five great reasons why real estate investing is a superb way to build and grow wealth. I’ll be sharing my progress in the coming months as I continue to learn more about real estate investing.

by John | May 19, 2016 | Capital Appreciation, Geopolitical Risk Protection, Liquidity, Passive Income, Preservation of Purchasing Power

Inflation has reduced the purchasing power of dollars by over 90%. Holding dollars is a sure way to lose value.

You need diverse and high quality investments to protect your purchasing power from the ravages of dollar debasement caused by inflation.

No one likes going to the store to find that a box of cereal is smaller and costs the same price or the same item now costs more.

Inflation is caused when private banks and the Federal Reserve increase the money supply. A larger money supply means there are more dollars in circulation.

This increase in dollars chasing the same amount of goods and services in the economy leads to rising prices or what’s properly called price inflation.

It is common to simply refer to rising prices as “inflation”.

I take steps to protect my Wealth from inflation

You can’t do anything about rising prices, but you can take steps that grow your wealth so that when you need to buy something you have more dollars (or Euros, or Yen) with which to pay the higher prices.

This is what is known preserving purchasing power and is a key concept.

I’m going to talk about two investments that help me meet my investment goals.

At the end of this article you’ll have an opportunity to subscribe to my Newsletter.

Newsletter subscribers receive details on the actionable ways I’ve chosen to protect myself from inflation that you can start doing today even if you only have a few dollars to invest.

These investments are not suitable for everyone and it might not be right for you, but the investment you’ll learn about immediately just by signing up below is an investment to which I’ve personally allocated several hundred dollars.

Let’s jump into two investments that help protect wealth from inflation.

Investments to Fight Price Inflation

Value Investing

8 March 2017 Note: I have further refined my value investing metrics in my article Better Metrics for Value Investing.

Believe it or not, there are certain stocks that trade below their book value.

Investopedia tells us that book value is “the total value of the company’s assets that shareholders would theoretically receive if a company were liquidated.”

So, if a stock is trading at a book value of .5, that means if you could buy all the shares then liquidate the company, you would make 50% per share. Now I’m not planning on buying all the shares of a company and liquidating it, but by purchasing quality stocks below book value there is built in downside protection.

There are other criteria as well, and stocks that meet the criteria are value stocks:

- Price to book less than 1.5

- Price to earnings less than 15

- Return on equity greater than 8% on average per year

- Dividend Yield

Value investing is how folks like Warren Buffet became billionaires.

When I allocate capital, I do so to areas that meet one or more of my Five Investment Goal Categories.

Value Stocks hit on all Five Investment Goal Categories. Value stocks serve to preserve purchasing power, provide capital appreciation, can create monthly income via dividends, foreign value stocks help hedge against geopolitical risk, and stocks tend to be among the most liquid assets.

One such stock I purchased back in October 2015 is Sberbank of Russia, ticker SBER on the London Stock Exchange. I have a offshore brokerage account (which is perfectly legal) that allows me to trade a variety of foreign stocks directly on foreign exchanges.

SBER has a price to book of 1.2, a price to earnings of 13.8, a return on equity of 9.53%% and a modest yield of .4%.

Source: MorningStar.com and TDAmeritrade.com

I purchased 100 shares of SBER at 4.772 USD, my brokerage firm charges me a $40 commission for both buy and sell. Sberbank is currently trading at $7.556 so I’m sitting on an unrealized 58.34% profit.

Not all of my trades go this way of course. I have $10,240 cost basis in my international brokerage account, and my account value is currently around $8,950. So I have both unrealized gains and losses that currently net out to unrealized losses. However, for value stocks, my time horizon is in the 2-3 year range and I’m very confident that in that time I’ll be in the black.

I’ll be devoting future videos and posts to value investing, which I feel is very important.

Precious Metals

The second investment I’ll touch on today are Precious Metals.

In my culture we have a saying, “Gold is the money of kings, silver is the money of gentlemen, barter is the money of peasants – but debt is the money of slaves.” Okay, that is actually a quote by Norm Franz from his book Money & Wealth in the New Millennium: A Prophetic Guide to the New World Economic Order but I’ve adopted it.

Gold took a serious pummeling since the latter half of 2011 through 2015. But despite that correction Gold has been up over 15% in 2016 and is up over 240% over the last 25 years. Yes, 240%.

Gold can’t be printed out of thing air and has been used as money throughout human history.

Gold also hits on four of the five criteria to varying degrees. Gold has a 5,000 year history of preserve purchasing power, it is unrivaled in this category.

If gold is undervalued, as I believe it is right now, it could provide capital appreciation (in purchasing power terms, not just dollar terms). Gold is a superb hedge against geopolitical risk, and while physical gold bullion is not liquid at this time compared to fiat cash, it is more liquid than say real estate or a business.

Despite large gains, I believe that Gold is still a great value and will go even higher and so I have chosen to invest a portion of my savings in physical gold.

I began purchasing physical gold and silver in December of 2012 and as a result I’m underwater on some of my positions. I’ve continued to make purchases throughout this time and overall I need gold to rally back to $1,400 to break even, and silver back to $24 to break even.

I would have preferred to have bought gold at the lows of $1,040, but as yet I don’t have a crystal ball that allows me to perfectly time the bottom of markets and I firmly believe that based on the fundamentals gold will make new highs in excess of $2,000.

When it comes to gold I firmly believe that it is better to be early to party than late. If the dollar goes down dramatically in value in a crisis situation there simply might not be any physical gold available for sale.

I also own multi-hundred dollars worth of gold through a relatively new and innovative way to purchase and store physical gold with very little up front investment. The benefit of this new way of owning physical gold is that it is very liquid as well.

Inflation is a destructive force, but with the right investments I’m able to position myself to continue to grow my wealth in spite of rising prices. I’ve discussed two assets I own: value stocks and precious metals that could be helpful as you make your own investment decisions.

There is exclusive information I ONLY share with subscribers of the HowIGrowMyWealth email Newsletter. Sign up using the form above!