My first article on this website was over 5 years ago, Inflation Destroys Dollars. I certainly did not have any idea that the price inflation would be triggered by the government’s response to the COVID-19 pandemic. I certainly didn’t anticipate the lockdowns and supply chain disruptions back in 2016.

I know the fiscal and monetary policy pursued by the United States and virtually all the world: money printing, onerous regulations, taxes and spending, would eventually result in significant price inflation. Government response to COVID-19 has made the situation worse and pulled the day of reckoning forward but it certainly isn’t the largest factor.

Timing is always a challenge and I was quite early.

Price inflation is here and it is happening fast enough where people notice it and are actually talking about it. Depending on who you trust and how you measure it, prices are rising at a rate of 6-10% per year now. I think what is interesting is that the government’s own numbers (the CPI-U) shows inflation at 6%. This is far beyond the 2% the Federal Reserve has been calling for.

In Inflation Destroys Dollars I write about how gold and silver are an inflation hedge. On 16 May 2016 when I wrote that article, gold was trading at $1,252 per ounce. As I write this it is currently up to $1,864.61, an increase of 48.9%. That is an annualized return of roughly 7.5%.

On 16 May 2016 Silver was trading at $17.14. It is now trading at $25.29. That is a 47.5% increase for an annualized return of approximately 7.3%.

So, if you think that inflation has been somewhere between 4% and 8% over the past five and a half year, gold and silver have on just kept up with inflation during this timeframe. Not bad but also not great. Gold and silver remain the boring reliable hedge and that is a good thing.

Value Stocks as an Inflation Hedge

Value stocks are another asset class I mentioned in Inflation Destroys Dollars. I didn’t mention specific funds. I have made some of my own individual value stock picks with some fantastic picks, but also some not so good picks.

Vanguard’s Selected Value fund (VASVX) is a mid-cap fund that could serve as a proxy for “value stocks”. It was trading at $26.41 on 16 May 2016. It is currently at $33.39. This is a return of 26.4% and an annualized return of 4.3%. Not stellar as I would not say this has kept up with inflation.

The Vanguard Value Index is a large cap value fund (VVIAX). It started this period at $32.49 and is up to $56.68. This is a return of about 74.5% and an annualized return of 10.65%.

A final example to look at, Vanguard’s Mid-Cap Index Admiral Shares Fund (VIMAX) started in this timeframe at $150.33 and is now at $320.62. That is a total percent return of 113% and an annualized return of 14.7%. Much better.

Compare those to the Vanguard 500 (VFIAX), which started this timeframe at $184.53 and is now at $432.9. The total return of this fund was 134.6% an an annualized return of 16.77%.

So while value stock fund did beat the rate of inflation and are a good hedge, they didn’t outperform your vanilla S&P 500 index fund.

Bitcoin as an Inflation Hedge

Compared to gold and silver, Cryptocurrencies, particularly Bitcoin has had all the action.

On 16 May of 2016 a Bitcoin was trading at about $454. Today Bitcoin is trading at $64,346. That is an astounding increase of 14,073% or an annualized return of about 146%.

Clearly Bitcoin has outperformed Stocks, Gold and Silver during this timeframe in an astounding way.

I own Bitcoin and I’m not anti-bitcoin. But I’m also not a Bitcoin maximalist. I think it is possible and perhaps even likely that Bitcoin will be replaced with a superior cryptocurrency that has some combination of faster transactions, higher transaction throughput, anonymity and or additional features. In my view Bitcoin in its current state is too slow and transactions are too costly for it to work as a medium of exchange for day to day transactions. These views are very unpopular with Bitcoin maximalists that ignore or downplay Bitcoin’s weaknesses.

However, Bitcoin has provided an incredible return and far outpaces inflation.

The 14,073% return is not just a result of inflation, although it is increasingly being viewed as a safe haven alternative investment.

Bitcoin has had several great tailwinds 1) It is an emergent asset class 2) It is trendy and popular and gets media attention 3) It is viewed as a Federal Reserve / dollar debasement hedge in place of gold.

Inflation Hedges

Protecting one’s wealth and purchasing power from inflation is important. Just keeping up with inflation is not ideal either, if the assets are not tax advantages, the government will tax the “gains”, and so purchasing power is eroded.

Let’s look at a simplified example. Say you frequently buy a widget or pay a service that costs $100 per year. Say the price goes up 5% per year due to monetary inflation. You also have a $100 investment that also goes up 5% per year. You’re still not keeping up with inflation because of taxes. If your $100 investment goes up 5% to $105, the government is going to want some taxes on that $5 gain. Say you’re on the hook for 15% capital gains taxes, the government is going to take their share and leave you with a $4.25 gain.

So you now have to come up with another $0.75 to pay for the item or service. Scale this up to include all of your expenses for the year and you see that you need to not only keep up with inflation, but exceed inflation so you have the money to pay the taxes on the gains.

In order to keep up with inflation your investment would need to be in a tax advantaged account that would lower or eliminate the tax burden owed or (again assuming a 15% gains tax) you’d need the investment to go up by about 5.9%.

This also shows how insidious inflation is. Not only is money worth less, but the government taxes the gains, even if there was no gain in terms of purchasing power.

One other thing to keep in mind, in the United States at least, realized gold and silver gains are taxed at the generally higher income tax rate rather than capital gains tax rate.

Are Gold and Silver Great Inflation Hedges Anymore

Gold and silver might not be very good inflation hedges anymore. If I owned gold or silver I wouldn’t sell unless I needed to rebalance my portfolio. I would expect these assets to at least keep pace with inflation, but unless the demand for gold and silver increases in excess of new supply, I don’t think gold and silver will beat inflation in the way needed in order to truly hedge for inflation when accounting for taxes. While it has produced a positive return in excess of inflation, it certainly hasn’t been a fantastic play over the last five and half years since I started HowIGrowMyWealth.com.

The world has almost always been pretty crazy. I think there is a bias, which isn’t necessarily a bad thing, to believe that now is a special time, it’s different. Now is “the best of times” or “the worst of times.” In a very real sense the current time IS the most important because the present is the only time we can directly impact. Also as humans we seem to enjoy superlatives. But it’s important to realize that things have almost always been fairly crazy. The world has almost always been mad.

Supply Chain Breakdown

So what is the crazy du jure? Well, the US and probably other countries are realizing what was obvious to anyone who cared to think about it: if you shut down industries, print money, pay people to stay home and otherwise disrupt and destroy supply chains you get price increases, delays and shortages. As if labor wasn’t tight enough, vaccine mandates are driving more people out of the work force.

One of the scariest phrases is “I’m from the government and I’m here to help.” When I heard Biden was going to get involved in the supply chain issues, particularly the ports on the United States left coast I knew it was only going to get worse.

Their brilliant solution? Fine Shipping Companies if their shipping containers remain in the marine terminals for too long. How that will actually enable the shipping containers to get unloaded and moved faster is anyone’s guess. Perhaps the shipping companies weren’t sufficiently motivated before and that was the problem? It makes no sense to me.

But I don’t have the experience in supply chain management that Biden and Harris do. Wait, scratch that, as a kid I worked in a warehouse shipping packages for four summers. Not stellar credentials in supply chain but four more summers experience than these public “servants” have.

Government Dysfunction

Forgive me for repeating myself when I use the phrase government dysfunction. When it became apparent Biden was going to occupy the White House and the blue team was going to have both chambers of congress I thought it was going to be bad. Really bad. I thought it would be bad because I don’t think that taxing, regulating and spending work and that is pretty much all Biden can or would do.

If you do think that taxing, spending and regulating work then we’ve been deprived from the socialist paradise by two moderate Democrats (or if you’re from New York or California, right wing extremists).

I am waiting for the other shoe to drop because Senator Joe Manchin a blue team member from West Virginia and Kyrsten Sinema, another blue teamer from Arizona are actually doing things I don’t wholly disapprove of. Or to be more precise they are not doing things.

That is the standard I have for politicians: did they do one or two things I don’t wholly disapprove of? If so they’re doing pretty good relative to their peers.

When his wife was appointed to a federal position that pays some $163,000 per year for public “service” I thought for sure Manchin was bought and paid for and would march to whatever beat Biden (who whomever is actually in charge of the executive branch) drummed.

But so far he hasn’t.

Manchin has put the Kibosh down on ending the filibuster (which is a racist Jim Crowe relic when anyone but the Democrats use it), he’s stopped the IRS from violating the fourth amendment by being able to snoop on anyone’s bank account with more than $600 $10,000 in transactions in a year, which is basically everyone not on welfare. He’s stopped the carbon tax and done some other good stuff. I didn’t realize there were still moderate Democrats but there is Joe Manchin.

Kyrsten Sinema gets some credit too. See? I can say something nice about Democrats.

Politicians always fail us, usually miserably, so I’m sure it is only a matter of time before Manchin and Sinema are brought in line and they click their heels like a good party members and do as they are told. But not so far.

Biden the Lame Duck

President’s who don’t accomplish anything are great. Gridlock in Washington is great for ordinary Americans. If Biden turns out to be a lame duck that would be fantastic. If you’re on the government dole it is a bummer, if you’re connected with the right folks in government you might not make another few million which is a bummer, but I’m convinced that for everyone else government inaction is a real plus.

Biden’s approval rating is pretty bad. I’m glad the US isn’t officially in Afghanistan anymore and I give Biden credit for having actually withdrawn. Obama didn’t make it happen, Trump didn’t make it happen. Biden (or whomever is actually in charge of the executive branch) made it happen. Full credit for that.

But even still it was a disaster. Incompetent leadership is not without its costs, some of which are deadly serious.

I’m not a military man (and neither is Biden) but why wouldn’t you make sure the US civilians (and Afghan allies) were evacuated PRIOR to withdrawing most of the military? I don’t think you need to have gone to West Point or the Naval Academy to have that instinct. What happened over there makes no sense to me.

Seeing desperate Afghanis clinging to airplane landing gear so they would not be left behind to be killed by the Taliban was disturbing and horrifying. But perhaps the worst was when the United States government killed an innocent family of 10 including 7 children.

That combined with how he is “handling” COVID-19 and the economy I think Biden’s prospects at a second term, should he decide to run, are not great. Disclaimer: “In my opinion the President has more power than he should have but less than people realize. The President gets blamed when the economy is doing poor and gets credit when it is doing well. But it’s all unwarranted.” But while not impossible (as we’ve seen with Jimmy Carter, George H.W. Bush, and Trump in recent decades) it is tough to beat the President in an election.

Regardless I expect the blue teamers to do poorly in the mid-term elections. My political predictions haven’t been stellar, but if history is any guide the party occupying the White House tends to lose ground in the next election cycle, and with Biden being less popular than most things (ok that link is to a satirical news site), I don’t expect 2022 to be any different. At this point in my life, I would be content if no new laws were passed and the government was in deadlock. When either party gets control particularly bad things happen.

Gold Has Failed as an Inflation Hedge

This has been a real bummer because I’ve written about gold a lot. I’ve written about how I think it is an important part of a diversified portfolio. Well inflation is here and gold hasn’t done much of anything. Stocks are up, real estate is up, Bitcoin and Ethereum are up, plywood is up, Costco has reinstated paper towel quotas, even $163,000 a year isn’t enough to buy a US Senator anymore, the CPI for goodness sake, a metric seemingly designed to not measure inflation is up. It seems like the price of everything is up, except gold. Gold is not up. Maybe it is a “barbarous relic”. If you own any I wouldn’t sell it, but it has been a disappointment.

Sure, it had that tease-of-a-run-up in 2020 where it broke over $2,000, but since then it has dwindled and is stuck around $1,800. While it is better than a sharp stick in the eye gold going form $1,500 at the start of 2020 up $300 as of writing this isn’t going to save anyone from inflation. That is about a 20% increase. Meanwhile, the dollar has depreciated some 15% during that time. Not fantastic.

I still think gold is important. It doesn’t have counter-party risk, it’s been subjectively valued for thousands of years. It’s not liable to get replaced by Bettercoin 2.0 like Bitcoin is, but I would have expected it to go up more during COVID times.

The World Has Gone Mad

The world has gone mad, but it didn’t happen in 2020, it happened much, much earlier. Twenty-twenty was certainly crazier than other years but it could have been worse.

I don’t mean to downplay these past few years for those who have lost loved one or who have had their life dramatically impacted by COVID-19 and the ensuing government response. Almost 5 million people worldwide have passed as a result of COVID-19. If you’ve lost a friend, family member, co-worker, teammate or anyone else due to COVID-19 it is not a statistic it is a very real tragedy. If you’ve lost someone because they couldn’t get preventive care or screening because of the lockdowns, if they committed suicide as a result of the social isolation resultant from social distancing policies and lockdowns, if they’ve lost hope because of job losses these are all real tragedies. Perhaps you yourself are suffering. These are all real and tragic realities that we’ve all been coping with to one extent or another.

Having said that I want to end on a (relatively? kind of?) upbeat note. The last couple years have not as bad as the Bubonic Plague outbreak of the 14th century where perhaps 25 million people (about 2/3 of Europe at that time) perished. It’s not been as bad as the 1918 pandemic where perhaps 50 million people died. It wasn’t as bad as the mid 1940s in Europe during World War II when an estimated 50-70 million people died. Or the 1950s in China under Mao where some 30-40 million people died or were killed. Thankfully, nearly 223 million people worldwide have recovered from COVID-19. It’s not like we’ve had World War 3. And while that is a low standard perhaps that is good enough for now. And God willing, perhaps 2022 will be a little better.

Peter Schiff is Chief Economist & Global Strategist at EuroPacific Capital. He is also chairman of a gold reselling company. He appears on RT and has authored several books about the collapse of the dollar. Peter is a vocal critic of the US Federal Reserve and warned loudly about the housing bubble prior to the 2008-2009 financial crisis.

I owe much of what I know about the Federal Reserve to Peter Schiff. I’ve read some of his books and used to listen to his podcast.

But I’ve come to realize that Peter Schiff is not someone you want to listen to for financial or investment advise. The following are some key areas where I think he goes wrong.

His EuroPacific Funds are Expensive and Underperform

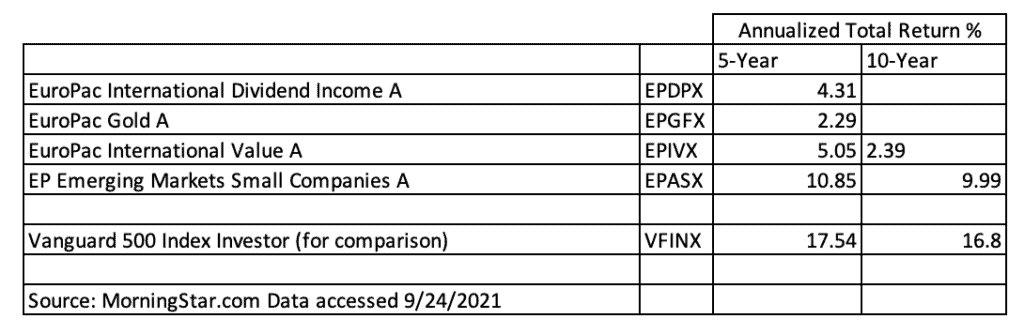

I invested some money with his firm, EuroPacific Capital between December 2014 and December 2020.

During that 6 year timeframe, my investments with EuroPacific Capital went up 20.5% (about a 3.8% annualized return) which doesn’t sound too bad until you consider the S&P 500 doubled in price during that same timeframe and provided an annualized return of nearly 15%.

Peter’s firm EuroPacific Capital, charges what I consider to be high load fees and they underperform. For someone who preached about inflation, you’d think he’d make sure his funds at least beat inflation. They don’t. Looking up his funds on MorningStar, you can see the poor 5 and 10 year returns.

The EuroPac gold fund has a 5-year annualized total return of 2.29%. Inflation has been well over that for the past five years.

His Bias for Gold and Silver Blinds Him

Some might consider me a gold bug. I believe gold and silver are an important part of a diversified portfolio. But with Peter being a gold salesman, he is overly biased towards gold, this has caused Peter to miss out on an emerging asset class (cryptocurrencies) that while more volatile, has far outperformed gold. He has unsuccessfully predicted many tops to this asset class.

Not only that, but he’s failed to predict where all the Fed money printing would go. It’s gone into real estate, stocks, cryptocurrencies. It hasn’t gone into gold, silver and foreign stocks the way he has been predicting.

He Can’t Time the Dollar Crash

Peter Schiff is the boy who cried wolf.

Sometimes there is a “wolf” and when there is, it’s is important to let other people know there is a wolf so we don’t all get eaten.

Peter did correctly cry “wolf” before the 2008-2009 “wolf” reared its head. But he’s been wrong ever since.

Peter is a big fan of extended metaphors. So here is one for him. Peter is the boy who cried wolf, no one believed him and it turned out there was a wolf and he was right. Then he cried wolf again over and over again for the next 12 years as if the wolf was just behind the bushes, even though the wolf was 500 miles away.

His rhetoric that the dollar crash is imminent might be an effective sales tactic in the short term, but he has been wrong since the 2008-2009 financial crisis. It weakens his message and erodes his credibility to the point that I don’t listen to him anymore.

He has not been able to time when the dollar will crash. I agree the US Federal Reserve is reckless, is a prime cause of market crashes and price inflation. There is no question the dollar will continue to lose value. But will it happen all at once in a huge crash, or will it continue to decline 2-6% per year like it has for over the past 100 years? I don’t know and Peter Schiff certainly doesn’t know.

He has had no ability to predict how long the powers that be (the big banks, the military industrial complex, the Federal Reserve, the US government) can keep the dollar charade going. He will talk and write about how “The Dollar Will Implode When The Markets Figure X Out” but the market consists of a lot of people who stand to benefit from the charade continuing.

If you listen to Peter you will probably be correct eventually, after all, reserve currencies don’t last forever, but you might not benefit from it in your lifetime. Or you might.

What Can you Learn from Peter Schiff?

I certainly wouldn’t bet the farm on the US maintaining its reserve currency status for the next thirty years. I will remain thankful to Peter for opening eyes to some very real risks the US and the dollar face. But I will never be happy that I missed out on a 100% return if I hadn’t been invested with his firm from 2014-2020. He is not the person I will be going to to figure out how to grow and protect my wealth.

The answer is to take a more diversified approach and to keep your costs down. You can own foreign stocks through a low cost Vanguard mutual fund. Most large non-US companies are listed on US exchanges anyway. Most US companies have large foreign components for their business. When you invest in large US stocks, you are also investing in their non-US sales.

I think owning 5-10% of your liquid net worth in gold and silver is important. I think if you have some extra money to speculate on with cryptocurrencies that could also result in some outsized returns. I think owning hard assets like real estate and yes even some gold and silver is important.

But thinking there is some impending dollar collapse looming on the corner doesn’t do any good. It certainly hasn’t for the past 12 years.

Gold isn’t supposed to tarnish but it has certainly lost its luster in my eyes so far in 2021. I have determined that for me, having 10-20% of my liquid net worth in precious metals makes sense as a protection against dollar debasement. Right now we’re in the kind of environment in which I would expect gold to shine (that should be it for the gold puns in this article.).

However, gold has not fared well so far in 2021.

What kind of environment am I writing about? Rising interest rates and helicopter money. Interest rates, while still historically low, have been rising. There has also been “helicopter” money where the treasury is directly sending people checks.

The Economic Environment

The latest round of these “stimmy bucks” should be coming soon, as President Biden is expected to sign a $1.9 trillion bill, which among many other things includes a $360 billion bailout of state, local and territorial governments and $1,400 check to anyone making $75,000 or less.

The blue team currently controls taxes and spending in the United States. While the reds are spendthrifts in their own right, and these stimmy checks were initiated under Trump, the blue team is worse. I’m not aware of a party which practices fiscal discipline in the United States. I expect this to be the first of many trillion dollar spending bills passed during the Harris-Biden Administration.

I understand that if the government is going to make it illegal for a lot of people to work and a lot of business to operate that creates problems, such as unemployment, less available goods and services and a lack of economic resources for individuals and families struggling to make ends meet. So this spending bill is no doubt an attempt to try to fix the some of the problems created by the lockdowns.

Whether these lockdowns were necessary to prevent people from dying from the Wuhan Coronavirus frequently referred to as COVID-19 should be debatable. However, thanks to censorship we all just have to click our heals and accept that without lockdowns the bodies would have piled up in the streets, hospitals would be overwhelmed and furthermore, that the increase in deaths due to undiagnosed cancer, suicide, etc., simply don’t exist or don’t matter. But I digress.

In an environment in which it has been illegal for people to show up to work to produce goods and services, and which the government is sending people checks, you expect rising prices. Prices have been rising. We’ll ignore the CPI, which seems to be designed to not measure rising prices. Lumber is up, oil is up, many commodities are up.

Gold is Not Rising

Even though many commodities are up, gold and silver are not up. Why is that?

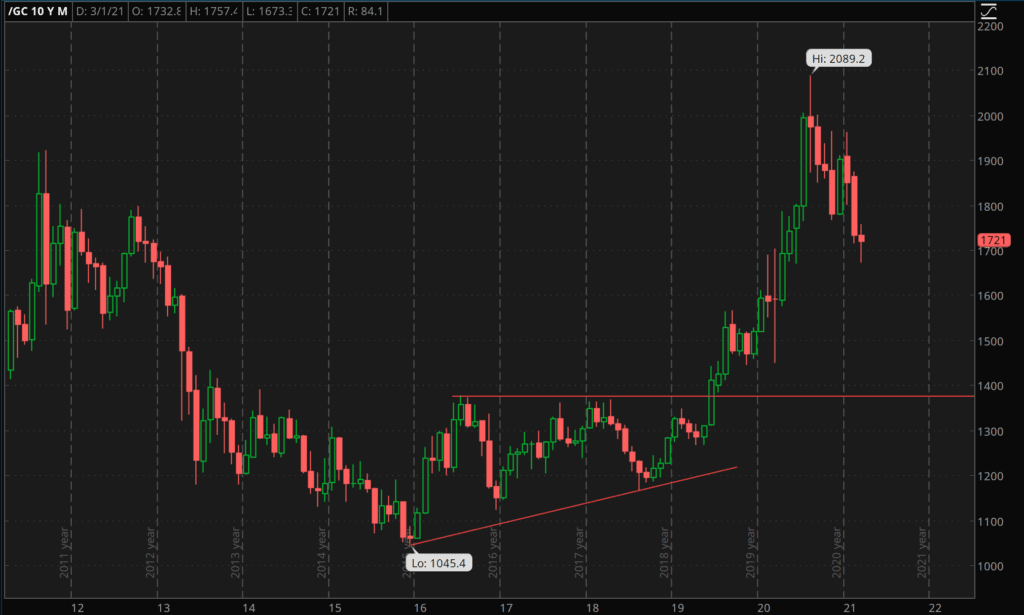

Gold Price Action over the last Ten Years

After making new highs in the wake of the 2008-2009 financial crisis, Gold had been in a bear market from September 2012 through November 2015, where it made a low of $1,045. It pretty much traded sideways and slightly up for the next four years, until 2019, when gold rocketed up, finally making that new high in August of 2020, reaching $2,089 per ounce. It then proceeded to sell off and is currently trading around $1,721. I think $1,800 was an important price level, but the yellow metal zipped right through it.

There does seem to be some support around $1,700 but it doesn’t look super strong. I’m definitely biased to the upside, but my guess is gold bounces between $1,700-$1,800 unless and until the Fed does something to manipulate interest rates back down. Why would the Fed do that? An economic recession or a stock market selloff.

In February of 2020, the S&P 500 was trading around $3,350 or so. This was before the lockdowns and the panic. Now, after having shut down a lot of the global economy, after unemployment going upwards, the stock market has recovered, but are things better than they were in February of 2020? The stock market thinks so. The S&P 500 has made a new high of roughly $3,950.

I would think that if interest rates continue to rise there will be a significant correction in the stock market. The Fed would then step in and do what it can to lower interest rates back down which would prop up stocks. So far the market had shrugged off rising rates, however.

Why Hasn’t Gold Performed?

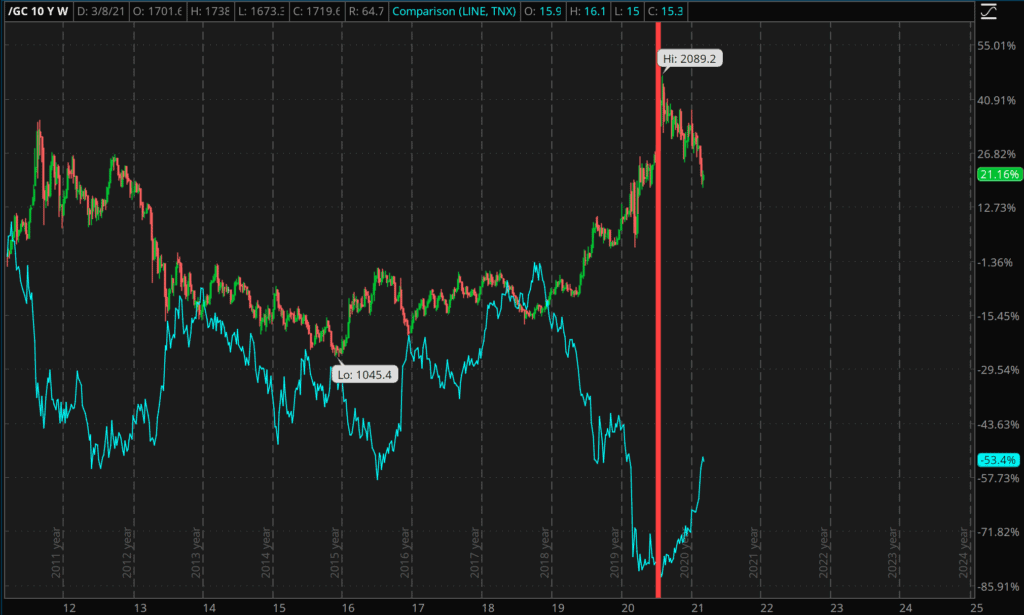

There are three main reasons. Reason #1 why gold hasn’t performed: rising interest rates. If bonds are yielding nothing, then it is easier for gold (which also yields nothing) to compete.

This is supported by the chart below. The 10 year treasury yield is in blue. You can see in late July, the yield on the 10 year bottomed and then started rising. At that same time gold peaked and then began to sell off. That inverse correlation looks very tight to me.

Gold has been a safe haven alternative to bonds in a low interest rate environment. Now that there is some yield to be had with treasuries, perhaps gold investors are concerned that zero yield gold will be replaced paltry (but at least nominally positive) yielding US debt.

Reason #2, which is conjecture on my part, is the stock market continues to rise. If there is real economic growth I would expect stocks to outperform gold long term. Gold is a safe haven asset outside the banking system. It does well when there is economic uncertainty, when a currency is in doubt.

Stocks have not sold off despite rising interest rates. As a result there isn’t a pressing need for a safe haven asset and money flows out of it. There was some volatility in the fall of 2020, but for the most part stocks have continued to go upwards. So while rising rates seems to have scared gold investors, it doesn’t seem to have impacted equity investors much.

Reason #3 is cryptocurrencies, specifically Bitcoin, which currently has over a 61% dominance in the cryptocurrency space. Some corporations are now deciding to put some of their money into BTC, and this institutional investment is doubtlessly driving the price up, and some people who are concerned about dollar debasement are probably deciding to go with so-called “digital gold” rather than real gold. You know it is bad when Peter Schiff’s son is liquidating his silver stocks and going 100% into Bitcoin.

From a transactional perspective it is less expensive to buy Bitcoin through an exchange like Coinbase, than it is to buy and ship gold from a bullion dealer. Some people are doubtlessly taking their stimulus checks and using it to buy Bitcoin.

Bitcoin Over Gold?

I won’t bother charting gold next to Bitcoin because Bitcoin has gone up so much that you would hardly even see gold on the chart.

I’ve never had enough confidence in Bitcoin to put a lot of money into it, and as a result have missed out on a lot of gains. The first mover advantage and name recognition seem to be enough to carry Bitcoin despite the existence of other coins that have superior characteristics, such as anonymity, higher and faster transaction throughput and lower transaction costs.

I’ve bought and sold Bitcoin over the years dating back to 2011 or 2012 and I still own some Bitcoin and EOS. Of course if I knew the price of BTC in 2021 was approaching $60,000 I would have bought and held onto more.

Despite the continued price rise to the moon and beyond, I personally have a lot more confidence that gold will be worth something 20 years as compared to Bitcoin which I have less confidence will be worth anything 20 years from now.

The two mains risks to Bitcoin are 1) The widespread adoption of a better alternative to Bitcoin 2) Interference from the Chinese Communist Party.

But, as I’ve written about countless times before, you can own both, it doesn’t have to be either or.

In the meantime I’ll continue to hold onto my gold and silver as a part of my overall asset allocation.

I was watching a video the other day by a famous YouTuber. He specializes in “modern homesteading” and I find some of his videos informative and entertaining.

However, he went off the rails with one of his comments.

He mentioned someone asked him if they should buy gold and he pointed out that you can’t eat gold.

I’m rather tired of this silly cliché. So I’ve decided to give this line of thinking a name.

Batteries are not edible. Please do not eat batteries.

The “Can I eat it?” School of Investing

The “Can I eat it?” school of investing is simple. People trained in this method rule out any investment or purchase they can’t eat.

For example, if someone were to ask, “Should I buy a car?”

Answer: “Well, you can’t eat a car, so what is the point?”

“Should I buy stock in Netflix?” “You can’t eat Netflix, so no.”

To be honest I‘ve never heard anyone make the “You can’t eat it” argument for any other investment or purchase decision. But for some reason when it comes to gold people think it is important to be able to eat it.

The notion that you have to be able to eat something in order to want to own it reminds me of small children at that developmental stage where they tend to stick everything in their mouth.

It seems like a fair number of people don’t understand the purpose of gold and so they revert to that childlike instinct of sticking in in their mouth.

I Buy some things knowing I Can’t Eat Them

As it turns out, there are many useful things that people might want to own that in fact can’t be eaten.

Some people have decided that it makes sense to allocate a portion of their savings to physical gold as a way to “store value” (Austrian economists: please don’t take that phrase too technically) and protect purchasing power against inflation and dollar devaluation.

Of course it only makes sense to own gold after you own a lot of other basic necessities.

But if you really must be able to eat an investment for you to be able to consider it–I give you the following dish which uses edible gold leaf as a garnish.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.