stonk: A term to express a financial decision that resulted in financial gain. Mostly used ironically.

For those of you not familiar GameStop is a brick and mortal video game retailer. Its stock had been heavily shorted by hedge funds. I heard that hedge funds were at one point short 150% of the GME stock in existence. How that is legal or possible is beyond me. That was the background. If the hedge funds had not been so short GME, this would not have happened.

But that is just the scene. Enter the main actors: a group of people on the reddit forums decided, for various reasons, to buy GME. The result triggered a massive short squeeze and stock price melt-up. In the course of 10 trading days GME went from around $30 to as high as $513 per share. It has cost hedge funds a lot of money as they’ve been forced to cover their short positions and buy the stock at the higher prices.

Several brokers halted GME trading or placed restrictions on the types of trades that could be made, angering (rightfully so) their “customers”.

I don’t know the reason reason why trading was halted by some of these brokers. It could have been for very innocent and good reasons on the part of the brokers to limit their risk. Other theories alleging nefarious intent abound. Did some of these hedge funds call in a favor? Was trading halted to tank the price so the hedge funds could cover their shorts? Who knows?

The volatility seems to have spilled into other markets as well. Major indices were down on the week–seemingly because hedge funds had to liquidate other holdings to cover their short positions.

It’s been a crazy week.

Here is an anecdote: I was in a company meeting (at my day job which has nothing to do with finance or investing) and the CEO was talking about GameStop. One employee mentioned a friend who was up over $100,000 in GME gains.

I hope they know when to sell.

Is the GME situation an extreme example of the broader trend?

While the GME stock melt-up, and even the other “reddit stocks” like AMC are extreme examples, I think they are indicative of the times: a lot of unemployed people at home, bored, angry, frustrated, armed with stimulus checks, low interest rates, and margin accounts buying up stocks. I think that is a bad sign. The rampant speculation devoid of fundamentals isn’t a good thing. A large number of unemployed people isn’t a good thing. Rampant speculation isn’t a good thing.

Of course it isn’t just retail investors. Institutional investors have low interest rates, are seeking returns, and have driven up asset prices beyond what I think the fundamentals would otherwise warrant. Sure, the institutional investors are supposed to be the “smartest folks in the room”. But they were also behind the dot com bubble and the housing bubble. So don’t tell me they don’t chase returns or make irrational decisions.

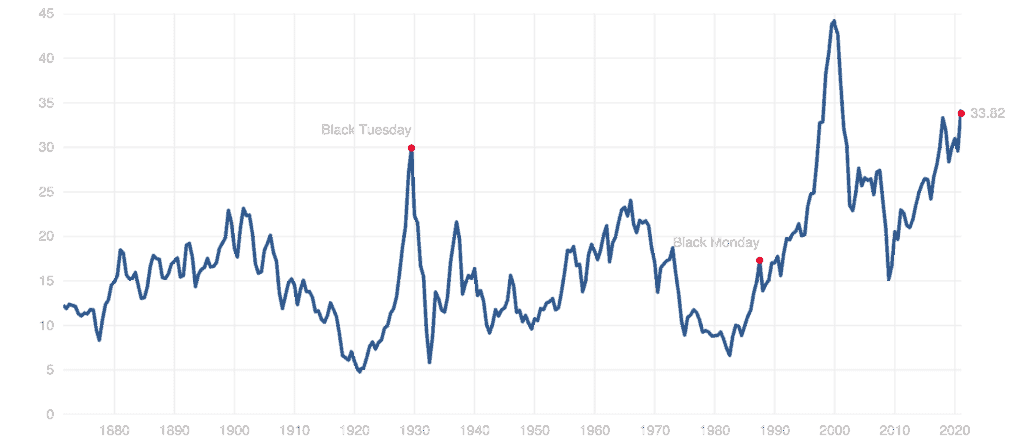

I have many reasons for believing assets are overvalued. I’ll just share one at this time, the Shiller PE ratio for the S&P 500 (shown below). The only time it has been higher is at the peak of the dot-com bubble in 2000.

I do think this short squeeze is a healthy thing. Some of these hedge funds are getting beat at their own game and getting taught an important lesson in risk management. It’s also got to be humbling for these hedge fund types to get beaten by the retail investors that they seem, in general, to have a lot of contempt for.

The GME Price Rocket is Still Absurd

On the flip side it is absurd. As of writing this GameStop now has a market capitalization of $22.6 billion. The market cap was just $1.3 billion on December 31, 2020.

The rapid increase in market cap has nothing to do with GameStop as a company. As billionaire hypocrite Warren Buffet once said: “In the short-run, the stock market is a voting machine. Yet, in the long-run, it is a weighing machine.” So what we’re seeing right now is many people voting for GameStop. But the “weight” of the stock has not changed.

Maybe people start buying more video games at GameStop. Maybe GameStop issues more shares at these high prices to raise capital, revamp their business model and they become a company whose fundamentals support a $22 billion or more valuation. I think this is unlikely.

But maybe none of that matters. People can subjectively value whatever they want. I don’t think that Bitcoin’s market cap of $645 billion makes sense but the market disagrees with me. Those buying into bitcoin back when it was just a few bucks and held to this point are sitting on tremendous profits. Bitcoin means a lot of different things to different people and as long as there is demand for BTC the price will be what it will be. If there was a special kind of dollar bill, people might be willing to pay $2 for it. Maybe GameStop will represent sticking it to the man and people will buy it just to participate in that movement. Maybe people will just buy it “for the lulz”.

As long as people value GameStop it can stay high.

What Does it All Mean?

In the short term fundamentals don’t matter. GME is exhibit A. People can subjectively value whatever they want. But in the long term I believe fundamentals do matter. What we are seeing, and have seen, is a lot of price action devoid of fundamentals. GameStop is an extreme example of this price action, but I think the same principle applies in a variety of markets and assets.

But for someone blessed enough to have assets to invest, what can you do?

Cash and even bonds are going to get destroyed by inflation over the long term. I like gold and silver as an asset and I think having a 10-20% allocation to these assets makes sense but they don’t provide growth or income in the way stocks do. Real estate, particularly residential and farmland, could be a good play, but there is a high cost of entry. There are REITs, but a lot of the tax benefits from investing in real estate come from directly owning the property and you can’t buy $10,000 worth of an apartment complex. (Although if there is a way with WITH the tax benefits please let me know!)

I think there is a place for cryptocurrencies although it is still a very young and volatile market segment.

The “big three”: S&P 500, Nasdaq and Dow Joes are all negative for 2021. There is reason for caution. But I’m looking for opportunities to buy into stocks. I think stocks are overvalued. But I don’t think avoiding stocks is a viable option. If stocks do tank, I believe the Federal Reserve will print as much money as possible to prop up prices, even if it means it destroys the value of the dollar.

Although it might sound trite, the best investment might be in yourself and those around you. There is a lot an individual can’t control but you can do a lot to learn, grow, and take care of your physical, mental, and emotional health.

There is more bad news coming out for Tesla (NASDAQ: TSLA). First, there is a lawsuit pending against CEO Elon Musk and former Tesla CFO that alleges they mislead investors about Model 3 production.

One claim of the lawsuit is as follows:

“As early as mid-2016, Tesla executives responsible for planning and building the Model 3 production line plainly told Defendant Musk and the other Defendants in person, providing specific support for their statements that the Company could never mass produce the Model 3 by the end of 2017. These Tesla executives told Musk and the other Defendants that it was an impossible goal.”

Tesla has a strong history of not meeting their production goals. I’m not saying they always fail to meet their admittedly ambitious goals and below I chronicle a few examples where they did not

Let start with their most recently reported numbers and compare them to past guidance.

According to the Tesla, in a 3 April 2018 release, their Q1 2018 production totaled 34,494 vehicles. Of those 24,728 were Model S and Model X, and 9,766 were Model 3.

“Our Model 3 program is on track to start limited vehicle production in July and to steadily ramp production to exceed 5,000 vehicles per week at some point in the fourth quarter [2017] and 10,000 vehicles per week at some point in 2018.”

Unfortunately Tesla would only produce 2,425 Model 3s in Q4 of 2017. This means that instead of making 5,000 Model 3s in 1 week they made less than half of that in a span of 13 weeks.

In Q1 2018 so far Tesla has produced, on average, 2,653 total vehicles per week and only 752 Model 3s per week.

So to get to 10,000 Model 3s “sometime” in 2018 weekly Model 3 production would have to go up over 1,229% in the next 9 months.

How was Tesla’s Q4 2017 Guidance?

Model S burning in 2013. Photo from autoblog.com

The Q4 2017 Update Letter stated:

“We continue to target weekly Model 3 production rates of 2,500 by the end of Q1 and 5,000 by the end of Q2. It is important to note that while these are the levels we are focused on hitting and we have plans in place to achieve them, our prior experience on the Model 3 ramp has demonstrated the difficulty of accurately forecasting specific production rates at specific points in time.”

Well at least they are admitting predictions are difficult! We know from the 3 April 2018 release that in the last week of Q1 Tesla only produced 2,000 model 3s and on average in Q1 2018 Tesla only produced 752 Model 3s. In total they produced just 9,766 Model 3s.

But that didn’t stop them from bragging, “The Model 3 output increased exponentially, representing a fourfold increase over last quarter.” Well Q4 2017 Model 3 production was just 2,425 so going up to 9,766 isn’t that great especially when you said you’d be producing that many a week 3 months ago.

“In the past seven days, Tesla produced 2,020 Model 3 vehicles. In the next seven days, we expect to produce 2,000 Model S and X vehicles and 2,000 Model 3 vehicles. It is a testament to the ability of the Tesla production team that Model 3 volume now exceeds Model S and Model X combined. What took our team five years for S/X, took only nine months for Model 3.

Given the progress made thus far and upcoming actions for further capacity improvement, we expect that the Model 3 production rate will climb rapidly through Q2. Tesla continues to target a production rate of approximately 5,000 units per week in about three months, laying the groundwork for Q3 to have the long-sought ideal combination of high volume, good gross margin and strong positive operating cash flow. As a result, Tesla does not require an equity or debt raise this year, apart from standard credit lines.”

I read that as a total of 4,000 vehicles per week, at least in “the next seven days”. Then they go on to say that they will produce 5,000 units (which I read as Model 3s) by June.

They would need to more than double their Model 3 production in the next 3 months to hit their targeted production rate of 5,000 units per week by June.

How likely is Tesla’s Q1 2016 Guidance?

In 2016 Tesla said they were planning to build half a million vehicles in 2018. This got a lot of press at the time and people were all excited.

The Q1 2016 Update Letter stated:

“Additionally, given the demand for Model 3, we have decided to advance our 500,000 total unit build plan (combined for Model S, Model X, and Model 3) to 2018, two years earlier than previously planned. Increasing production five fold over the next two years will be challenging and will likely require some additional capital, but this is our goal and we will be working hard to achieve it.”

How likely is Musk and Company to produce this many vehicles?

Well let’s assume for a minute that Tesla, starting in Q2 is able to produce on average 4,000 (Model X, S, 3) vehicles per week in Q2 for a total of 52,000.

Then they are able to produce 7,000 vehicles (Model X, S, 3) for the remainder of the year without disruption for a second half total of 182,000.

Those three quarters combined would be 234,00 vehicles and added to the 34,494 produced in Q1 and you get to 268,494, so its a little over half of the stated goal they listed in the Q1 2016 Update Letter.

Remember Tesla did not produce 4,000 vehicles in a week in Q1. They said “In the next seven days, we expect to produce 2,000 Model S and X vehicles and 2,000 Model 3 vehicles.” Bold added.

On average in Q1 the total combined production was just 2,688. So thinking they could produce 4,000 vehicles a week consistently, in Q2 and 7,000 in the second half of 2018 is giving Tesla a big benefit of the doubt.

Another way to look at it is even if they can double production starting in Q2, up to 5,376 total vehicles per week they would only get to 209,664 by the end of the year. So it seems highly unlikely Tesla will reach 500,000 vehicles produced by the end of 2018.

A picture of the 25 March 2018 Tesla crash which resulted in a fatality. Photo From Business Insider

In addition to the lawsuit the other recent bad news for Tesla is in regard to Model 3 production. Production of the Model 3 has halted at least twice already in 2018, first in February from the 20th-24th. Another halt started today and is estimated to last 4-5 days.

To paraphrase Yogi Berra, forecasting is hard, especially about the future. However, providing the best possible “forward guidance” is what publicly traded companies are expected to do. At best Tesla is not very good at predicting what they will be able to do and at worse they are being deceptive. To be clear I am not saying Tesla intentionally attempting to deceive investors.

I do think that Elon Musk, at times, has demonstrated a rather fluid relationship with reality.

On the one hand I admire his vision, I remember doing some research into Mars exploration and terraforming when I was in college so it is exciting that Musk is interested in colonizing the red planet as well. Flamethrowers are also awesome. The idea of the hyperloop is a fascinating concept.

The guy is not afraid to dream big and I admire him for that. But on the other hand I think it is possible that he misleads investors and with billions on the line I have a problem with that.

People are taking notice. A recent tweet by the Economist prompted an almost Trumpian response (and forward guidance about Q3 and Q4) from Musk.

The Economist used to be boring, but smart with a wicked dry wit. Now it’s just boring (sigh). Tesla will be profitable & cash flow+ in Q3 & Q4, so obv no need to raise money.

I predict that Tesla will not be cashflow positive in Q3 2018. I further predict Tesla will not be cashflow positive in Q4 2018.

Good Marketing and Design Don’t Mean a Good Manufacturer

I’ve wanted a car with “gull-wing” doors ever since watching Back to the Future as a kid. Photo from Motor Trend

A recent article by Jim Collins points out that Tesla is a horrible automobile manufacturer.

“Tesla is the worst car manufacturer in the developed world. Bar none. Note that I didn’t write “designer” or “marketer,” but manufacturer. Musk had zero auto industry experience when founding Tesla and CTO J.T. Straubel—who according to Tesla’s 10-K filing personally holds Tesla’s important patents—developed a love for electric vehicles by rebuilding golf carts. It’s just astounding to me that the markets are affording a $50 billion valuation to a company that can’t perform the most basic task for which it was incorporated.”

Even though Tesla designs some great looking automobiles and does a heck of a job marketing them doesn’t mean Tesla is a good business or a company in which a person should invest.

And in fact quarter after quarter of negative free cashflow, missing many production targets and increasing debt would suggest that Tesla is a very bad business.

None of those facts will stop a believer from believing as summarized I think by this tweet:

A Tesla fail is now shorted by many.. They lost so much before and still haven’t learned.. Tesla is not only a business.. It’s a movement for a better future.. Shame on The Economist for not recognising

Electric car company Tesla has a market capitalization over $40 billion. Over the past few months the stock (TSLA) has lost nearly a third of it’s value dropping from $360 per share down as low as $244.

Bonds issued by this electric car company are yielding higher than that of Ukraine (indicating higher risk) and recently the autopilot on one of their cars resulted in a death.

Tesla as a company is not exactly in great shape. The stock was already trading down to the year lows.

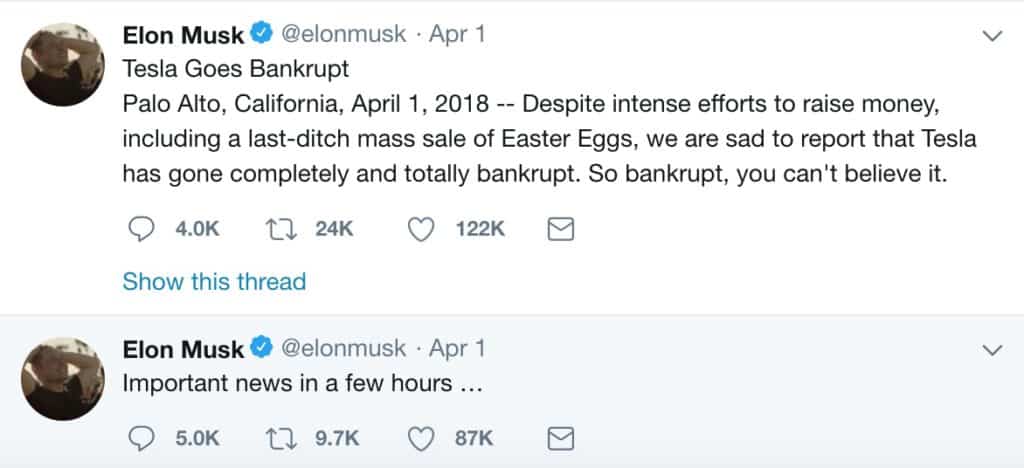

Now it’s 1 April–what does CEO Elon Musk decide to do?

Elon decided it would be hilarious to tweet about his company going bankrupt.

CEO Elon Musk tweeted out some “jokes” about his company filing for bankruptcy

Now if Tesla was humming along nicely this would be little more than a sophomoric prank by an eccentric billionaire.

However Elon’s company is performing extremely poorly.

In terms of free cash flow Tesla has consistently “generated” negative free cash flow in the billions since 2014. It’s free cash flow has been negative as far back as I can find data (2008).

Many other metrics are similarly dismal.

Negative margins, $.51 worth of liquid assets for every dollar of current liabilities, negative return on assets and a negative return on equity.

If you just looked at the balance sheet and didn’t know what company it was for you’d have a hard time finding anything positive to say.

This is all in spite of receiving billions in subsidies from the government.

Elon was probably onto something and it does seem likely that his company will eventually file for bankruptcy.

Tesla is an example of an overvalued stock that is ripe for crashing (even further). What are the fundamentals that justify such a high valuation of a company that destroys cash?

Why can’t genius businessman Elon Musk turn a profit despite massive government subsidies?

Tesla (TSLA) and Netflix (NFLX) are two examples of darlings that are propped up by hope and cheap money.

Investors can continue to hold stocks like this but eventually profits and fundamentals will matter again.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

{kind=link}