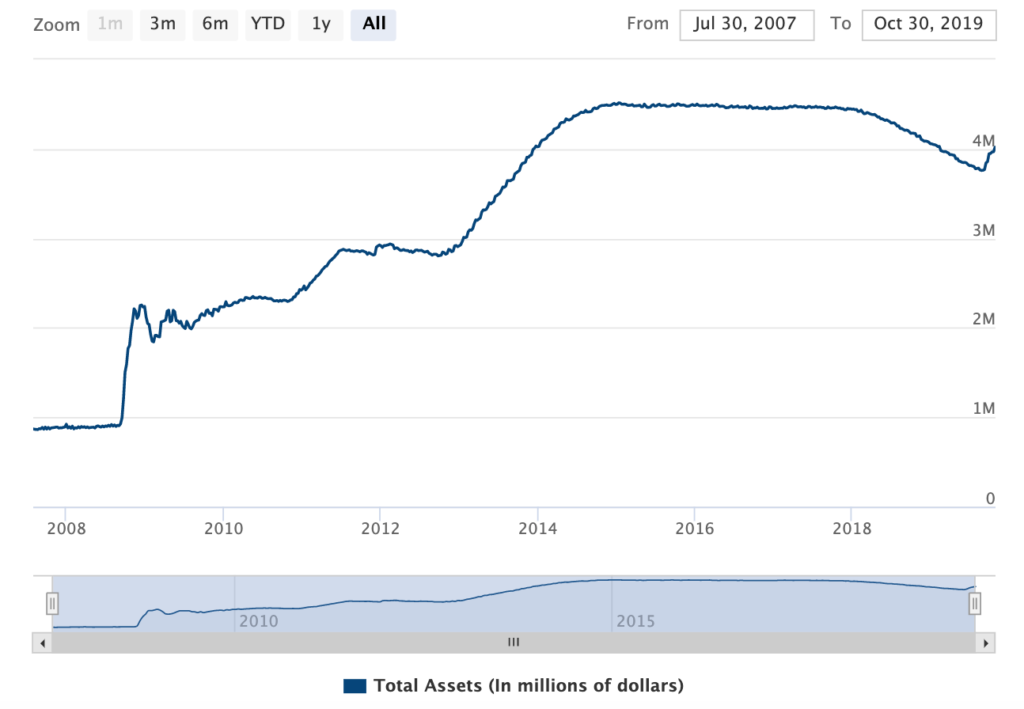

The Federal Reserve Balance sheet is back above $4 trillion for the first time since February of 2019.

This is more evidence that the US Government will monetize the national debt.

Monetizing the debt is when the government conjures money out of thin air “expanding the money supply” (in what amounts to legal counterfeiting) in order to pay the money it owes.

Monetizing the debt this puts downward pressure on the value of dollars and hence makes everything more expensive in what is described as price inflation, all else equal.

Is the Fed Monetizing the Debt?

The Federal Reserve has indicated that it would not monetize government debt.

“The Federal Reserve will not monetize the debt.” – Fed Chair Ben Bernanke

The reasoning goes that because they intend to shrink their balance sheet they aren’t just conjuring money created out of thin air.

But this is dependent on balance sheet normalization. Indeed, starting under Fed Chair Janet Yellen and accelerating under Fed Chair Jerome Powell the balance sheet had been trending down from the January 2015 high–at least until August 2015.

But as of 28 October 2019 the Fed’s balance sheet is back above $4 trillion. As humans we tend to place greater significance on large whole numbers when in fact there is nothing special about $4 trillion. But the point is that the Federal Reserve balance sheet began to tick back up starting in September of 2019.

Was the balance sheet declining from $4.5 trillion in January of 2015 down to $3.7 trillion in August of 2015 the extent of the “normalization” process?

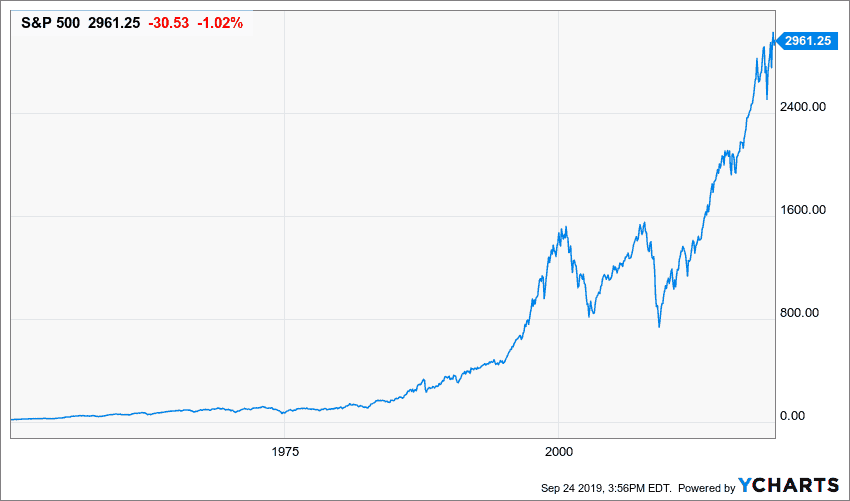

The S&P 500 is making all time highs, everything is supposed to be wonderful in the economy, and yet starting back in September the Fed’s balance sheet is growing again, quite rapidly in fact as evidenced by the steepness of the chart.

How can the Fed ever normalize if they can’t do it after 10 years of stock market growth?

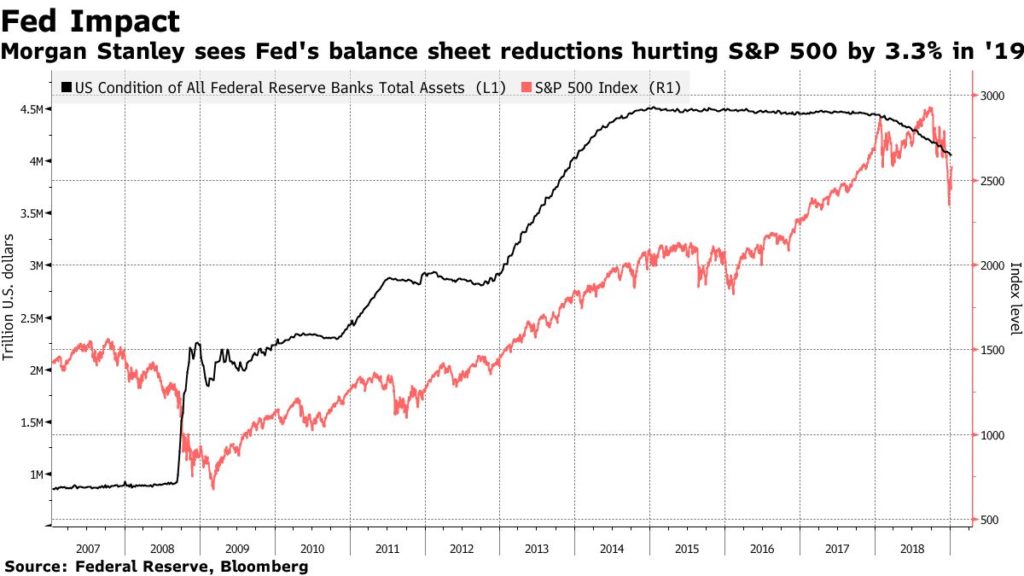

The above chart only goes through 2018. But it does show that the Fed’s balance sheet is correlated with the S&P 500. Despite the balance sheet tapering off slightly from 2016 onward through mid 2018 the S&P 500 continued to grow, until it sold off rather significantly in December.

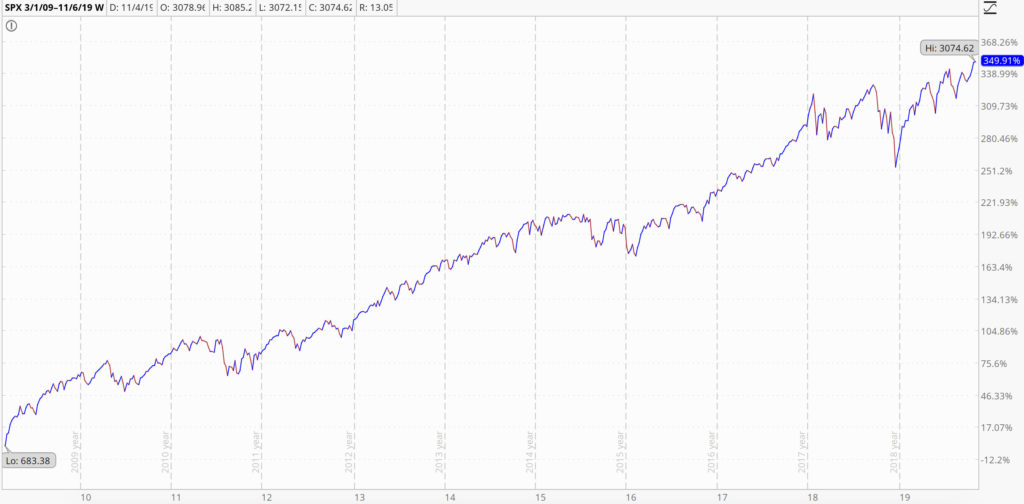

Since December the S&P 500 has rallied back and achieved new highs. All told, the S&P 500 has gone up nearly 350% since the March 2009 lows.

An intrepid investor who purchased the S&P 500 in the dark days of March 2009 would have done very well. However, I believe this artificial “growth” is really a bubble blown by the Federal Reserve.

If this “growth” has been fueled by the Fed’s monetary policy, then the Fed can’t even normalize without also tanking the markets.

Combine this with trillion dollar annual budget deficits and $23 trillion in national debt, the US simply doesn’t have any ammunition to fight the next economic downturn, at least not without seriously compromising the value of the dollar.

Source: https://usdebtclock.org/

US stocks have been the investment strategy for the past ten years. But this is the longest period of economic expansion in the history of the United States.

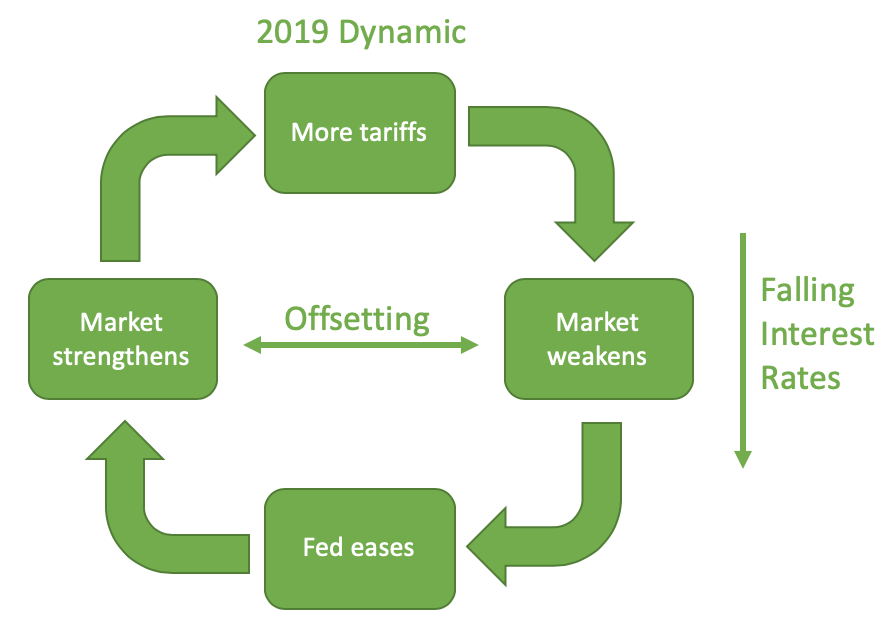

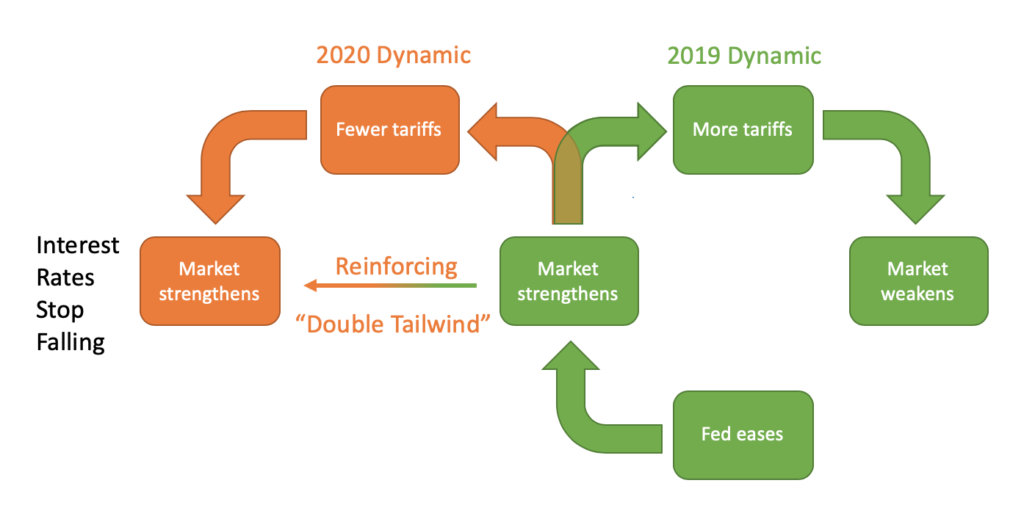

Until recently market dynamics have been something like the following: Trump threatens more tariffs, the market sells off, the fed eases and the market rallies. I wrote about this in a past article entitled Trump is Beating the Fed like a Rented Drum Set.

Recreation of a BofA Merrill Lynch Diagram

Phase I: Get Interest Rates Low

The result is interest rates at 1.5-1.75%, “This is not QE” QE, and the S&P 500 at all time highs.

Trump Playing the Trumpet in a badly Photoshopped image

I believe Trump’s prospect for reelection is tied almost entirely to how the stock market performs. So why would he threaten tariffs if they cause the market to go down?

I conjecture firstly that Trump genuinely believes in tariffs and secondly: so he gets lower rates.

But this is only Phase I: where interest rates are already low and perhaps the Fed has signaled they intend to keep lowering. On 30 October the Fed poured a little cold water on Phase I by indicating they intend to pause easing.

Low interest rates and QE is just the first tailwind.

Phase II: “Win” Trade War

I expect Phase II, the “Double Tailwind”, to occur in 2020 and be timed for the election.

Phase II is kicked off either by winning the trade war, or (more likely) simply declaring the trade war won.

The market believing there won’t be new tariffs is the second tailwind, which combined with the first forms the “Double Tailwind”.

Phase two means fewer tariffs or even a complete trade war victory

The “Double Tailwind” means the market isn’t getting freaked out by tariffs and selling off and interest rates are low.

The US stock market could go to even higher highs and secure Trump’s re-election. Trump can then use the bully pulpit of the presidency and appoint an uber-dove to ensure that rates are raised slowly or not at all.

Interest rates might very well stay where they are at. During the 30 October press conference Fed Chair Powell said, “I think we would need to see a really significant move up in inflation that’s persistent before we even consider raising rates to address inflation concerns.”

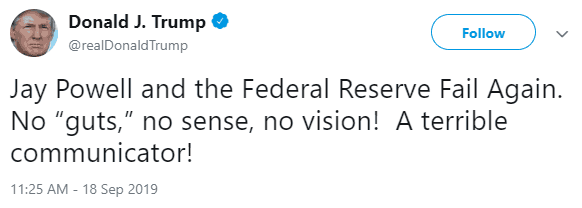

Why he appointed Jerome Powell only to throw him under the bus is beyond me, but he will probably do more to ensure he get’s a low interest rate puppet as Fed Chair for his second term.

I don’t know if Trump is planning this out in some grand ‘3D chess’ maneuver or not. But if he is, I have to admit it has a sort of Machiavellian genius to it.

Potential Problems

3D Chess – metaphor for using multiple, non-obvious levels to outmaneuver one’s opponents

Whether it is intentional or not, Trump is now responsible for blowing more air into what is now an even bigglier and uglier bubble and can join the ranks of the Presidents responsible for destroying the dollar and the US economy.

Quarter three GDP was up 1.9% beating the expected 1.6%. Employment is robust. Inflation as (not) measured is “contained”. Between that and the S&P 500 rise will the Fed be able to justify continuing to cut rates?

Another problem is when you get high on heroin you have to deal with the crash. You can’t take the heroin away and keep the high. In fact you have to keep taking more heroin to get a similar high.

Low interest rates are monetary heroin. So if interest rates don’t continue to fall then the market will fall. This most recent “insurance” rate cut may have been the last. If so there is a whole year between now the election in which even the Double Tailwind can fade, bringing the economic ship to a halt. Timing the trade war “victory” correctly before the election will be essential.

The uninitiated often think of the United States as a free market economy. It is in some specific ways but it is a far cry from a laissez-faire free market system. The main reason why the United States isn’t a free market is because of the Federal Reserve System, which controls money and how much it is worth. Money which is on one side of every single transaction that occurs in the economy.

Another reason the United States is not a free market is because of the myriad of taxes, rules and regulations prescribing how virtually all aspects of economic activity must be conducted.

Conventional foolishness states that deregulation causes the 2008-2009 financial crisis. However there were 115 agencies regulating the U.S. financial sector. As Tom Woods says, “Your friends think things would improve if there were 116.”

Monday the 28th of October was another example of how distant the US stock market is from a free-market and how the US economy is very much controlled, manipulated and centrally planned. Trump primed the trading algorithms this morning by stating he, “Expects A Good Day In Market Today”.

The S&P 500 then opened at a new all-time record high as a result. Meanwhile the Federal Reserve, the biggest currency manipulator in the history of the world, is expected to cut rates from an extremely low 1.75-2% to an even more extremely low 1.5-1.75%.

A free market economy is not driven to all time highs by the words of one man or a small group of bankers.

But a larger question remains: if everything is so great, why the rate cuts and “This is not QE” Quantitative Easing?

One factor driving the market is the trade war. When China and the US talk and say nice things to each other the market rallies. When they say mean things or refuse to talk the market sells off. The Federal Reserve is perhaps trying to give some support to the markets when China and the US seem like they can’t play nice.

But I believe the main reason is because the market is expecting it. The Fed isn’t data dependent. The Fed is market dependent. The odds of a rate cut are really just a voting machine to tell the Fed what to do.

I’m sure it doesn’t help the US Fed to be “independent” when Trump pounds on the oval office desk demanding more rate cuts and QE. The irony is that Trump is now just as guilty as Clinton, Bush, and Obama in blowing a big, “fat, ugly bubble.” Trump, if reelected, will be lucky if he can pull an Obama and exist stage left before it blows up during his tenure.

If the US were a free market interest rates wouldn’t be set by a small cabal of unelected, semi-private, pseudo-governmental bankers. It would be set by the supply and demand of lenders and borrowers.

The central banks, who artificially lower interest rates and inflate asset bubbles, fuel greed and cause recessions and crashes. Meanwhile, free markets get blamed and the plutocrats call for more regulations that simply reduce competition from smaller players who can’t afford an army of attorneys to both comply with the new rules and look for and find the loopholes. Regulations also raise costs for consumers.

Meanwhile the regulations wouldn’t have prevented the crisis anyway.

This can’t end well but who knows when it will end.

Stocks go up when China and Trump say or do something nice to each other and then stocks fall when they leave meetings early, don’t meet, or say something mean.

It is a tiresome game that has been going on for some time. It seems like China and Trump are fundamentally at odds with each other and any real trade agreement is impossible.

I think the best thing Trump could do (if I was his campaign adviser) is declare victory, focus on and inflate some arbitrary thing he got from the trade war and then promise no more tariffs.

The United States benefits much more than China from trade between the two countries. China loans money to the US then the US buys cheap goods from China with said money. China gets pieces of paper (or the electronic equivalent) saying the US will pay them back. It is the ultimate vendor financing.

The Fed Caves to Trump

Despite low unemployment numbers, “contained” inflation the stock market near all time highs and all the other supposed reasons why the economy is the best ever, the “independent” United States Federal Reserve cut rates last week. The Fed funds rate is now back down to 1.75-2.00% because of….reasons?

This was all but assured as far as the market was concerned.

The market has been going up, up, up for the past ten years. The Fed is cutting rates when the economy is supposed to be doing well, when the next downturn hits, what is the Federal Reserve going to do?

Between the trade wars and the federal reserve, can we please stop pretending that the United States is a free market economy? Please?

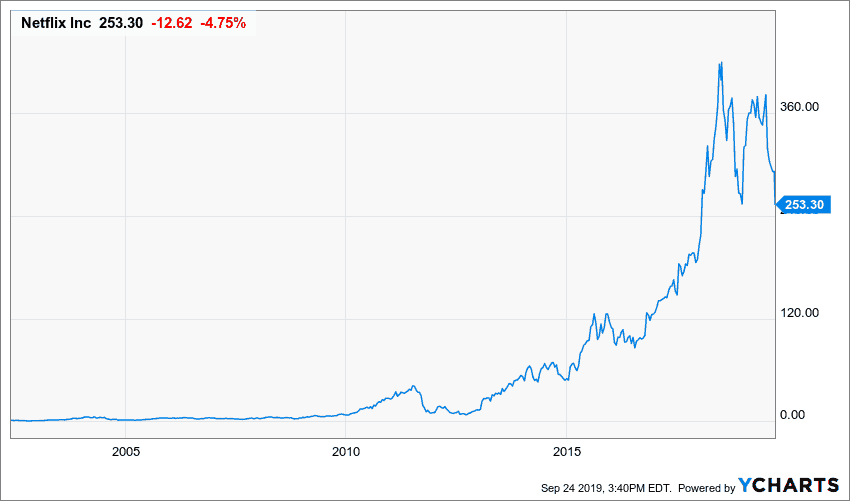

Netflix Tanks

Netflix (NFLX) has been getting pounded.

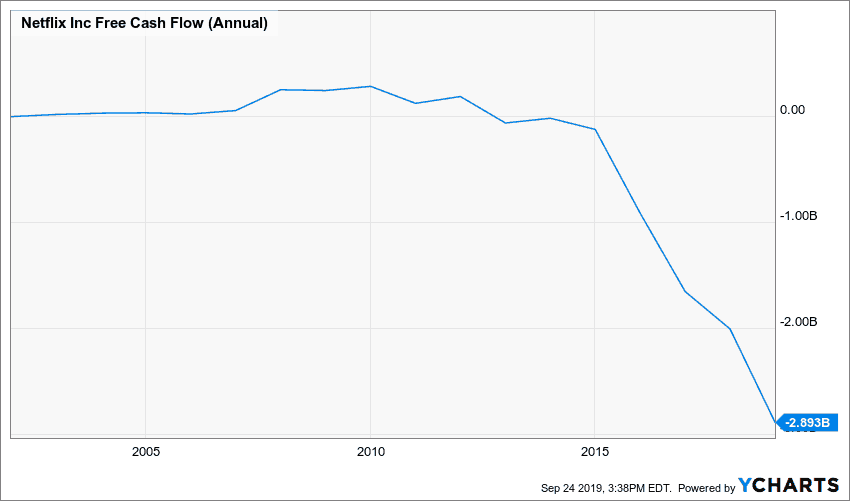

Netflix doesn’t make money. Since 2011 they have lost money each year and they have to keep borrowing more money just to keep making content.

One of my key metrics in evaluation stock is free cash flow. It’s like earnings only harder for accountants to monkey with. Netflix has not had positive free cash flow since 2011.

Looking back three years free cash flow at Netflix was a negative $1.66 billion in in 2016, negative $2.01 billion in free cash flow in 2017, negative $2.89 billion in free cash flow in 2018 and are on track to lose over $3 billion this year.

Netflix is a classic example of great product, lousy business. It looks like the market is finally waking up to the fact that Netflix is not a good investment.

With more competition from the likes of Apple and Disney, I don’t expect this show to have a happy ending for Netflix.

What is John Doing?

I’m well positioned for what the market has been doing. Of course I missed out on some of the meteoric rise over the past 10 years, but it is good to finally see my positioning pay off.

I’ve been raising cash all year and sitting on gold holdings. I am in the market some, but I’m certainly overweight cash. I did start shorting Netflix when it was about $325.

I still like gold (and silver), gold stocks and value-oriented international stocks. I still think it’s important to be invested in the US some, but not a lot.

I think Netflix is still overvalued even after the large selloff and I think it will go down to the $150 range (or lower) over the coming couple of years. I only short with money I can afford to lose because it is risky and tough.

Shorting is harder than going long because you have to get both the direction and timing correct. If you’re long you only have to get the direction right (although timing is nice here too).

I don’t recommend shorting Netflix or any other stock.

I’m not worrying. Economic downturns don’t happen immediately. They are gradual, the market springs back even in the midst of selloffs. Take some prudent steps to diversify outside of mainstream investments and don’t worry about it. Build up an emergency fund, live within your means and live your life.

The major US indices were down today, each about 3%, likely triggered by the inversion of treasury yields as well as cynicism regarding a US-China trade deal.

The yield on the 10-year treasury note fell below the yield of the 2 year treasury note for the first time since May 2007.

Does this one article title sum up the US stock market? Source: barchart.com

Normally if you are loaning money for 10 years, you demand a rate of return greater than if you’re loaning money for 2 years. In other words, longer term debt should pay more interest than shorter term debt. When this isn’t true, it’s called inversion.

The fact that the yield on the 10-year was less than the 2 year (ie inverted) is a bad sign that historically indicates an incoming recession.

What do negative yields mean?

The way the government responds during a recession is to lower interest rates and spend money. This is the conventional, Keynesian approach, often referred to as monetary stimulus.

Unfortunately, this only makes the problem worse, but the government doesn’t realize that and it will be what they do in the next downturn.

Interest rates are already low, and so there isn’t a lot of room to cut before hitting 0%.

Rational people have positive time preference, meaning that they would rather have $1 now than $1 ten years from now. If you’re going to loan a stranger $1, you’re going to want interest, partly because there is a risk they won’t pay you back and partly because rational, normal people have a positive time preference.

What would negative time preference look like? A person with a negative time preference would rather have $.90 ten years from now rather than $1 now.

You can’t find real people who have negative time preference.

However, former Fed Chair Alan Greenspan, famous for inflating the 2000 stock market bubble and thus causing the subsequent crash doesn’t think negative yields are a problem.

“There is no barrier for U.S. Treasury yields going below zero. Zero has no meaning, beside being a certain level.”

He and many other supposed technocrats don’t have a problem with negative yields on debt. That combined with the lack of room to maneuver means that if there is a stock market correction or crash, once the Fed cuts rates to zero and restarting quantitative easing and asset purchases, negative rates are not far behind.

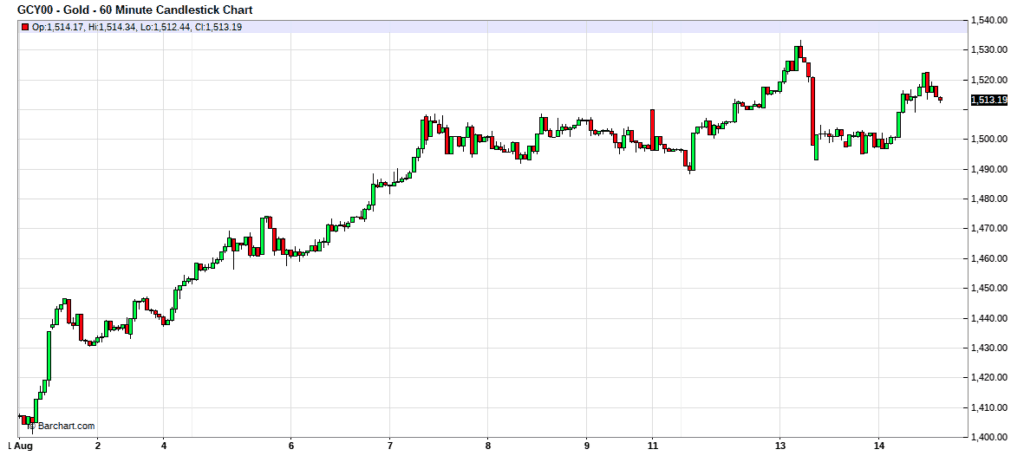

Gold should do well in this environment.

Gold has been bouncing around between $1,490s and $1,510, with a brief breakout attempt on the 13th in which the spot price of gold went as high as $1,530 before retesting supporting at the $1,490s. The yellow metal is up over 17% on the year.

I think we’ll see $1,600 per ounce gold this year, and it could go even higher before 2020 arrives.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.