We are weeks if not months into various shutdowns in the United States due to the novel coronavirus. The government has already taken many moves to try to soften the economic impact of the stay at home orders, layoffs and other effects caused by attempting to slow the spread of the virus.

Interest rates have been slashed back down to zero. States who have made irresponsible choices on pensions and spending are requesting bailouts. Unemployment is spiking. Stimulus measures are being passed.

The US Economy is based on consumption and debt. Over the long term an economy can’t survive based on consumption and debt. Long term prosperity is based on producing more than you consume. The US consumes more than it produces and makes up the difference with debt. But this article isn’t intended to address that. Taken at face value, the US Economy is based on debt.

With the majority of US states in some type of lockdown. People can’t go out and spend money. Just a few of the impacts: travel, collegian and professional sports, going out to bars, dine-in restaurants, movie theaters, and amusement parks.

People can still shop online to consume and restaurants can serve via takeout and delivery. But the fact is there are major disruptions to the supply chain and people staying home are going to be spending less.

When I look at the markets. They seem to believe that either the stimulus will make up for any disruptions and/or the worst is behind us. The S&P 500 for example, fell over 35% from the peak, but has rallied back and is down just over 14% from the February 19 high of 311.59.

I do think the US government backed by the Fed will print and spend and stimulate the economy as much as they can. But the Fed can’t print masks, toilet paper, food, or goods and services.

The inevitable result will be price inflation and shortages. I don’t want to be doom and gloom. While there are real risks there is no need to panic over COVID-19. People have an amazing ability to adapt and unencumbered entrepreneurs are incredible at generating wealth and increasing standards of living for everyone.

However, there are real challenges and owning alternative assets like gold and silver could be a great way to protect wealth.

I also read a great article that compares the stagflationary episodes in past decades and what investments did well then. It isn’t a quick read but provides detailed and valuable information about What a Secular Bear Market in the 2020s Could Look Like.

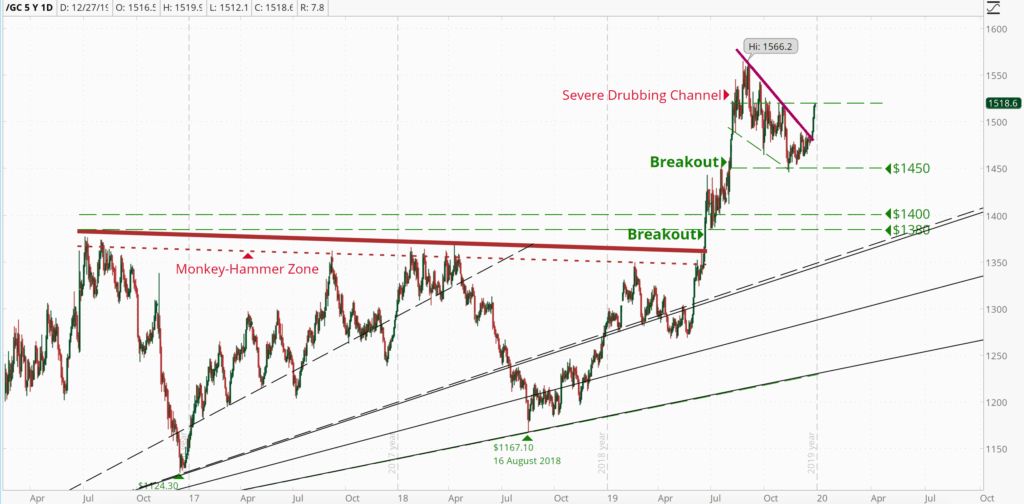

In time for Christmas gold has moved up above $1,500 and as of writing is trading north of $1,510.

I had previously written about how gold has been on the receiving end of a severe price drubbing. Not so now.

The fundamentals of gold are very strong. Gold was is a downward channel and this strong move upward could be a continuation of the gold bull market that began at the end of 2015/early 2016.

The $1,450 level looks like strong support. Gold would need to break through the $1,520 and $1,545 levels to retest the six year high set 4 September of $1,566.

In what I describe as an anti-Black Friday sale, Goldmoney announced on the 29th of November a new $10 per month minimum storage fee.

This goes into effect on 1 January 2020.

Goldmoney (formerly BitGold) already had storage fees, but they were proportional. Now, smaller accounts might not make financial sense anymore.

I’ve determined that Goldmoney doesn’t make sense for me anymore.

Goldmoney Fees are Too Darn High

It is always important to understand the fees a financial services company charges, and Goldmoney has plenty. There is a 0.5% gold buy/sell fee and a $20 wire transfer fee for withdrawals (funding can be free with EFT).

Storage fees vary by location and the lowest cost locations are .01% per month (London, Hong Kong, Zurich, Singapore).

However, this new a $10 per month minimum fee is a killer. In order to pay just .01% per month, you’d need to have at least $100,000 in gold stored.

As a simple example, $10 per month fee on $120 worth of stored gold would be equal to the value of the gold stored after just one year.

Some other considerations, which in my view don’t help enough, are that Goldmoney does offset the minimum fee with commissions paid and the accounts are insured.

However, your homeowners insurance or renters insurance might cover your safe deposit box as well.

If you have a larger account, insurance is important to you, or conduct a lot of transactions, Goldmoney might make sense.

Goldmoney Doesn’t Make Sense for Smaller Accounts

I was previously an advocate of this low cost way to store physical precious metals around the world. With this new development in fees I have decided to withdraw my endorsement of Goldmoney.

Because of the smaller amount of Gold I have with Goldmoney, I’ve elected to sell all my gold in their custody. At this time I have no intention of doing business with Goldmoney again.

The insurance is an important consideration, however, a safety deposit box or other secure location is going to be much more cost effective for the small investor.

If ever there was a case study on the advantages of name recognition and first mover it is Bitcoin. There are dozens if not hundreds of altcoins technologically superior to Bitcoin, that have a market cap significantly lower than Bitcoin. Some of the major Bitcoin flaws I see are the following:

Bitcoin is slow, taking a minimum of 10 minutes per transaction but realistically at least 20 or more minutes.

Bitcoin transactions are expensive

It is energy intensive

Source: bitcoinfees.info

Let’s say you want to use Bitcoin to buy a $2 cup of coffee. You’re going to have to pay $0.36 cents, wait 10 minutes for the transaction to get picked up, and nearly all vendors require 1-2 transaction confirmations to prevent double-spending. It doesn’t work practically speaking.

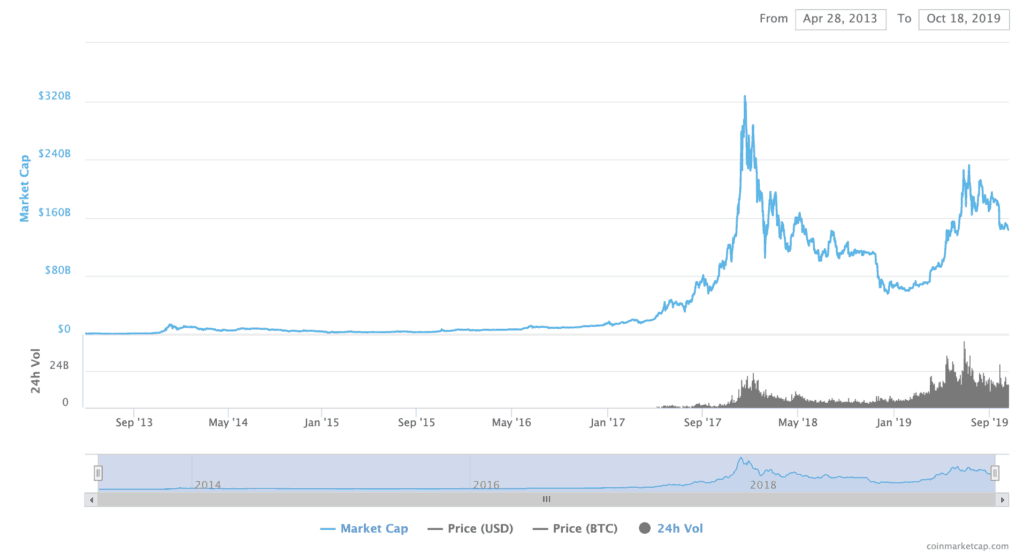

And yet the Market Capitalization of Bitcoin is over $143 billion. The next closest cryptocurrency, Ethereum, doesn’t come close, having a market cap of $18.8 billion.

The price and Market Capitalization of Bitcoin peaked in December of 2017. The market cap was as high as $327.1 billion on the 16th of December.

Bitcoin was groundbreaking and truth be told I still own some Bitcoin. But I believe that if another cryptocurrency took its place as the biggest crypto by market cap it would be a good thing. I’m calling for the death of Bitcoin.

I also think this provides an investing opportunity, or perhaps more realistically, a speculative opportunity. There are a variety of other cryptocurrencies that excel far beyond Bitcoin in a variety of ways, be it speed, security, anonymity, energy efficiency, user-friendliness, the list goes on.

I think this provides a speculative opportunity. Cryptocurrencies like EOS or other projects with real-world use cases could go up dramatically in value. There are hundreds of cryptocurrencies and a lot of them will probably be worth very little in the mid to long term.

It’s worth educating yourself on the various cryptocurrencies projects apart from Bitcoin. It might be worth investing in a few if you think they could have future promise.

Coinbase has a program that allows you to learn about various cryptocurrencies and earn free crypto at the same time. My referral link for EOS can be found here coinbase.com/earn.

“It’s tough to make predictions, especially about the future.” – Yogi Berra

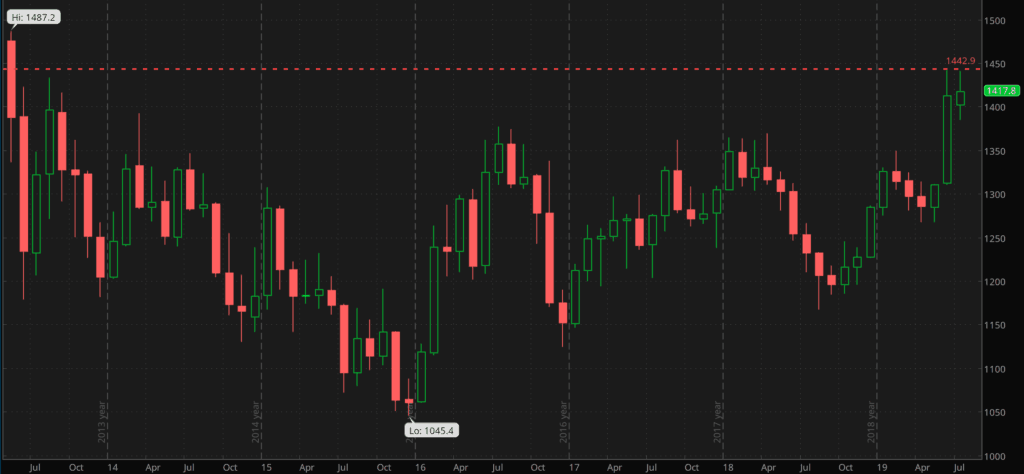

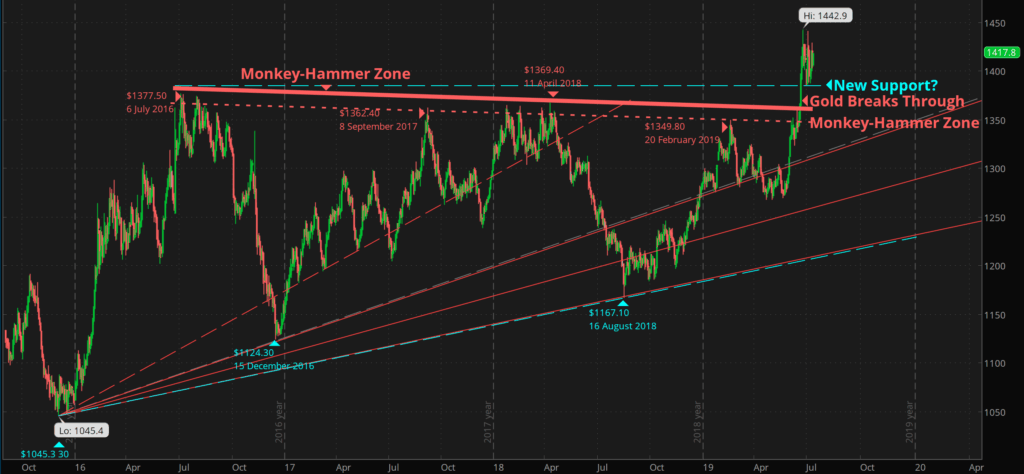

I must say I’m pleasantly surprised. Over a month ago I wrote how gold was entering the monkey-hammer zone. This zone was the price level of $1,350-$1,360, where over the past five years, whenever gold gets to around that range, it gets beaten back down.

Not so in June of 2019. Gold has punched through the monkey-hammer zone and made a new multi-year high of over $1,440. In fact gold hasn’t traded that high since May of 2013.

I had written the following: “I would be pleasantly surprised if gold could breech $1,360 and remain there or higher but if not I think it’s likely to drop down to the $1,230-$1,240 range.”

Turns out the external catalysts gold needed to punch through the monkey-hammer zone was potential war with Iran, trade war with China and the end of the US Federal Reserve’s tightening cycle and the European Central Bank cutting interest rates.

Gold traverses the monkey-hammer zone and new support level of $1,384 forming

The US Federal Reserve

The US Fed has strongly suggested they will cut rates in July.

The fact that the US Federal Reserve is cutting rates with low unemployment and all time highs in stocks is an indicator that gold could go much, much higher.

There isn’t much room to cut rates before hitting 0, and effective interest rates are already near zero if you simply look at the government statistics. The fed-funds rate is 2.25-2.50% and the official CPI as of July being 1.6% means the effective interest rate is just 0.65%-0.9%.

This is simply using the government numbers.

I think the actual rate of inflation is higher than 1.6%. The largest expense I have is rent. I renewed my lease this month and it was 3.5% higher.

Let’s say the rate of price inflation is actually 2.5%. Rates are already effectively zero or even slightly negative.

If the Fed is cutting rates now, when things are good, what are they going to do if things go bad?

The narrative since 2009, with record low interest rates, has been buy stocks. However, price inflation, at least as the government measures it, has been contained. If inflation were to really take off, gold should do well.

I also think stocks could continue to do well in this environment. I think it is possible that stocks keep going up as the more people lose confidence in the dollar. However, if there is a scenario in which gold will really shine, it is in an stagflationary environment the Fed has been creating for the past decade.

Gold in 2019

I didn’t know when gold was going to break out, I just knew it would eventually because of the weak fundamentals of the fiat and debt based global economy.

I actually thought gold would get monkey-hammered back down this go-around, just like is has the past half dozen or so times before over the last five years.

As I’ve stated before, I believe the gold market bottomed in December of 2015 at a price of $1,045. It has been consolidating over the past four years and now, with this breakout above $1,400, could be starting a new and stronger leg of the bull market that began in late 2015.

Of course external catalysts such as a full on war with Iran could cause gold to move higher quickly.

You have to go back pretty far to find any level of price resistance. Around where gold is trading $1,420-$1,430 is one level of potential resistance, the other being around the mid-$1,500s.

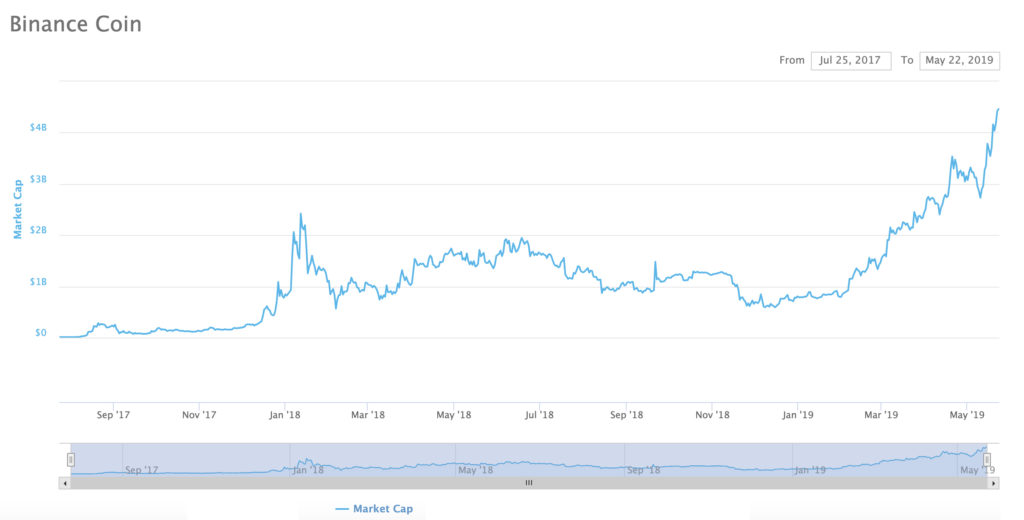

Binance.com is one of the largest cryptocurrency exchanges by volume. Binance launched its blockchain Binance Coin (BNB) back in July of 2017. It seems to be going well for the platform as BNB is already the 7th largest cryptocurrency by market capitalization.

[poll id=”6″]

With a Market Cap of nearly $4.5 billion, BNB is the 7th largest

As you may have already guessed, the name “Binance” is a combination of Binary and Finance.

HODL (Hold on for Dear Life)

Sometime back in 2013 the term “hodl” was introduced. One story I heard about the etymology of the word was it was a misspelling of “hold” and then became a sort of acronym meaning “Hold On for Dear Life”. Which is in reference to the violent downswings (and upswings) cryptocurrencies can experience and that one should hold (or “hodl”) through these periods.

HODLing BNB

BNB coin started out as a way to pay for trading fees. Binance would reduce the trading fees, if they were paid in BNB. I actually owned some BNB fairly early on (as in a couple years ago) simply for this reason.

I wish I’d hodl’d my BNB! Although I had no way of knowing it would go up 27,334% percent.

You better hodl fast (Master & Commander anyone?)

I’m of the old-fashioned belief that a cryptocurrency needs to have some sort of non-speculative use. The value of bitcoin can’t just be (long term) a speculative vehicle. Things eventually return to their non-monetary use value.

That is one of the reasons I like BNB: it has quite a variety of non-speculative uses such as: reducing trading fees on Binance (currently up to 25%) and for posting as collateral for loans. There are many other uses listed on binance.com.

Source: https://www.binance.com/en/use-bnb

I heard (although I can’t cite this) that BNB is going to be used for a distributed exchange at some point.

Imagine Reducing the Currency Supply!

Another reason to like BNB is that they are planning on burning up to 50% of the supply (the exact opposite of price inflation!). So that eventually there will only be 100 million BNB in circulation.

So if you want to speculate on cryptocurrencies, you might want to buy some BNB. But if you do, you better hodl fast.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.