An option is a contract that gives the buyer the right, but not the obligation, to buy or sell an underlying asset at a specific price on or before a certain date. An option, just like a stock or bond, is a security. It is also a binding contract with strictly defined terms and properties.

If that seems like a foreign language don’t worry. I’m going to break down what that means and provide an example to illustrate one way options are very useful.

If you buy a put option you have the right (but not the obligation) to sell a stock at a given price within a given timeframe. The put option seller has the obligation to buy the underlying stock from you at the given strike price, provided it is exercise before the expiration date. The seller gets a premium for providing this “insurance”.

Additionally you can buy what’s known as a call option where you have the right (but not the obligation) to buy the underlying stock at given price within a given timeframe. For the privilege of this “option” you pay a premium. On the other side of this option contract is an option seller who has the obligation to sell you the underlying stock at the strike price at any time before the contract expires if you choose to exercise the option.

Aren’t Options Risky?

I’ve been trading options for around a year now. They can enable an inexperienced trader to lose money fast. However with the right education trading options is a great way to generate active monthly income.

I’d like to use an analogy to explain the risks of trading options.

Say you know how to drive an automatic transmission car in the US. But now you’re in a hilly and busy part of Britain and you’ve got a stick shift car. You’ve never driven a manual transmission car before, you’re not familiar with the area you’re driving and you don’t know the rules of road.

It’s going to be bad. Very bad.

But if you practice driving “stick”, learn the rules of road in Britain (like driving on the left side of the road, etc), don’t take too many risks and learn the area you’ll be driving in, a manual transmission automobile is an excellent and safe way to get around Britain. There are still risks but if you’re careful they will be small and rare.

If trading stocks is like driving an automatic car in one’s home country. Trading options is like driving a manual car in a foreign land.

Trading Options Can be Profitable

Unfortunately I’ve learned this the hard way. I thought, “I’m a smart guy and I’ve been trading stocks for a long time, I’ll jump into options!” As a result I lost a lot of money.

I have been interested in options for a long time and was devoted to finding a way to make money with them.

I believe that I’ve found a trade methodology that is profitable in the long run. In fact in August, making my own option trades, I’ve brought in $120 using an account that is roughly $8,000 in size. That’s a 1.5% gain in just a couple weeks.

I link to a free option education resource that I highly recommend later in this article. I’ll also be sharing the trades I made in August in a different post.

Tell me more about Stock Options!

I’d like to contrast options to stocks, since more people are familiar with stocks.

When buying stocks you want to buy low and sell high. You might also be interested in the dividend the company pays to shareholders. With stocks the name of the game is if the stock goes up or down.

Options are a different animal. Yes, direction matters, but option pricing is also a function of the time to expiration (the given timeframe you have to exercise the option) and implied volatility.

As it pertains to stock options volatility is how much the underlying stock price moves up or down within a given timeframe. For example, a stock that goes down in price 50% and then up in price 100% over a period of two days is more volatile than a stock that goes down 10% and then up in price 20% over a period of two days all else given.

Understanding volatility and how it impacts option pricing is arguably the most important difference between trading stocks and trading options.

Purpose of Options

But why even buy options?

You can use options to speculate (using leverage) on the direction of a stock up or down. You can use options to open or close a long stock position. You can also sell options to gain a premium depending on if you think a stock will go up, down, or sideways. I think of selling options as selling insurance.

Another reason for buying options is to hedge a position. Let’s dive into the example to explain how you can use options to hedge a position.

Let’s say you own a stock you think will go down $16 in value, but you don’t want to sell it (and pay commissions and potentially have a taxable event). You could buy a put option. A put option to protect a stock position is like buying insurance against losses.

An Example

For example lets say you own 100 shares of Apple stock (AAPL). AAPL is currently trading at around $106. Lets also say you think that the September 7 Apple event is going to disappoint and that the stock is going to go down to $90 per share. (This is just an example and should not be construed as my opinion on Apple, next iPhone, or stock movement.)

Lets also say you bought AAPL when it was trading at $50 and you don’t want to sell your stock at this time and have to pay taxes on $50 per share in gains.

Current theoretical AAPL position

Current AAPL value: $106 per share x 100 shares=$10,600

Cost: $50 per share purchase price x 100 shares=$5,000

Unrealized Gain/Loss: $5,600

If AAPL were to drop to $90

New AAPL value: $90 per share x 100 shares =$9,000

New Unrealized Gain/Loss: $4,000

So if you’re right and AAPL does drop to $90 per share you’re going to give up $1,600 in unrealized gains. (Unrealized just means you haven’t sold the stock and realized the profits yet.)

In order to hedge (or insure) your AAPL position you could go out and purchase a put option that expires on 16 September with a strike price of $106. One such option costs as of writing $1.77 and lets you sell up to 100 shares at a price of $106 for a total cost of $177 ($1.77 x 100).

So again lets say you bought the $106 strike price put option for $177 and AAPL does drop down to $90 on 8 September.

You’re gain/loss on the stock would be the same, $4,000. But you’d have the option to exercise your put option and sell AAPL at a price of $106. If you did that you’d keep your AAPL gains, less $177 paid for the put option.

So your gains would be $5,432 once you exercise the option and take into account that you paid $177 for the option.

Now the downside is that if AAPL doesn’t drop down $1.77 you are better off NOT exercising the option and you’d have paid $177 for nothing except peace of mind.

So buying a put option to protect a stock position can be thought of like homeowners insurance. You hope you don’t have to use it, but if your house catches fire and burns down you’re glad you have it.

Now I mentioned before one of the reasons for buying the option to lock in gains was so you wouldn’t have to sell the stock. Exercising the option is one choice but that still creates a taxable event.

If AAPL were to drop down to $90 the intrinsic value of the option would be at least $16 per share. Because the option contracts come in lots of 100 that option would now be worth somewhere around $1,600. In reality the option would likely be worth even more depending on the implied volatility, time decay and a lot of other complex factors beyond the scope of this article.

The point is you could sell the put option for a $1,600 profit, without ever exercising it, and never touch your stock position.

An Excellent Free Resource to help Get Started Trading Options

To learn more about options I highly recommendOptionAlpha.com. OptionAlpha.com is run buy a guy named Kirk DuPlesis. I’ve never met him in person but we’ve exchanged emails and he is a great guy.

Disclaimer: I am not compensated for recommending option education at OptionAlpha.com.

Kirk has created dozens of training videos that are available for FREE.

Not only are the videos 100%, no-catch, FREE, but watching these videos are one the best ways to learn about options and how to trade options.

The OptionAlpha website and podcast have been very valuable resources for me and I’ve paid for some of Kirk’s more advanced information, like his trade alerts and stock watchlist.

I think Kirk is giving away tons of high quality information for free because once you see how much value you get from his free materials, you’ll be very likely to buy some of his other paid services.

Again, I don’t gain anything from Kirk or OptionAlpha.com by recommending you visit his site. It is a valuable resource that I’ve taken advantage of that I want to share with my readers. I wish I had known of OptionAlpha.com to help me get started trading options. It would have saved me a lot of money and allowed me to avoid a lot of mistakes.

Options can be very risky if done incorrectly. Trading and selling options is not right for everyone. If you decide to learn more about options, get educated at places like OptionAlpha.com, paper trade for a long time, and keep your position size small.

I’ll be posting another article later in the week with the option trades I made in the later half of August to make $120 with an $8,000 account. I’m still an option trading neophyte and I don’t recommend anyone trade options without first considering your risk tolerance and investment objectives. Get educated and make your own decision.

I just want to share one of the things I’m doing to grow my wealth.

I was having coffee with some new acquittances a few weeks back and mentioned I run a blog website about personal finance. I was asked a very good question which I don’t think I answered very well!

The question was: “Where do I start?”

I’ve been saving and investing for a long time and thus far this website has often focused on alternative and more aggressive investment strategies.

I can appreciate it’s hard (and likely unwise) to jump right into advanced investing so I want to write what I think are some things to consider when just getting started in the world of personal finance.

I originally wrote this as one big article. But realized it was too much! So I broke it down into three digestible parts. Today is Part I: Stabilization

Disclaimer: I don’t give financial advice. One of the reasons I don’t give investment advice here on my website is because there are exceptions to many rules and your personal situation could merit additional considerations. What is suitable for me might not be suitable for you.

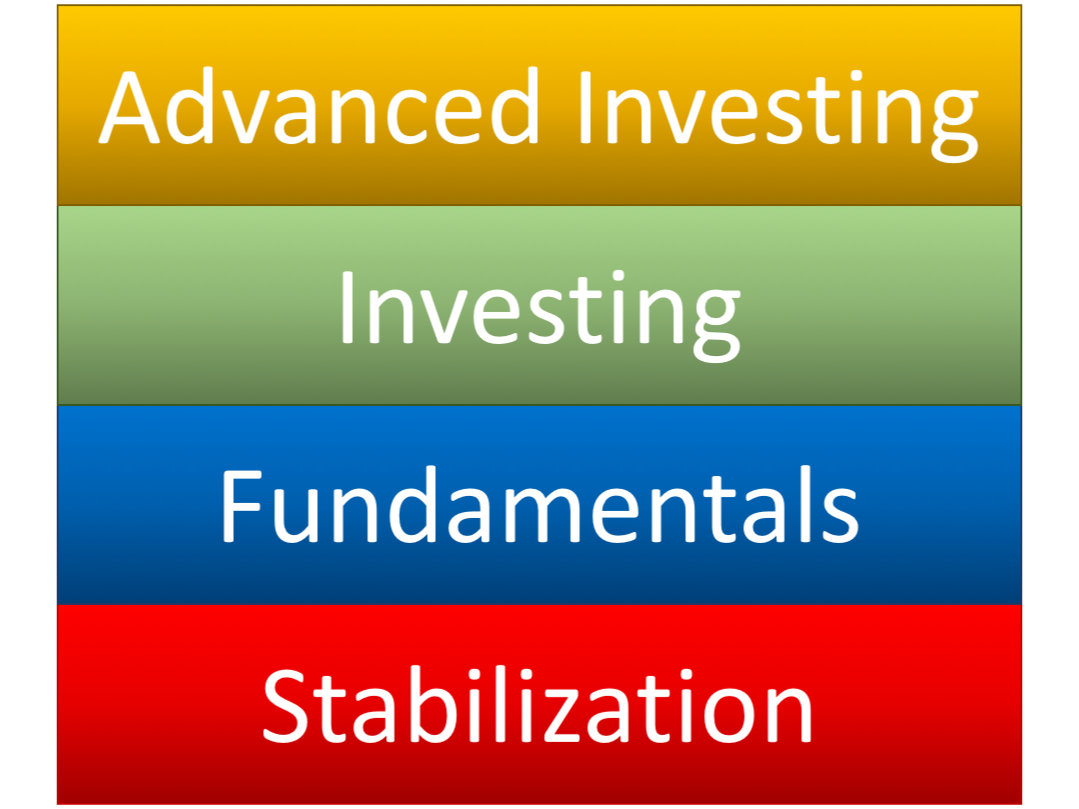

Basic Principles about Personal Finance

The Building Blocks of Personal Finance

I visualize these principles like building blocks. You have to have the lower levels in place before you can move to the upper levels.

Here are the basic principles:

– Debt for consumption is bad (Stabilization)

– You must produce and save more than you consume (Fundamentals)

– Have your money work for you (Investing and Advanced Investing)

The first level: Stabilization

In the health and medical field it is wise to make sure that a patient is stable and healthy before they try to fix some less pressing long term issue.

If an out of shape person is hemorrhaging blood due to an injury it would be absurd to focus on ways to improve their cardiovascular fitness until they are stable and healed from their injury.

The first step on the path to growing your wealth is to stabilize your financial situation.

These things don’t make you rich but they stop you from getting poorer.

One of the great financial traumas to an individual’s finances is bad debt. This bad debt must be controlled before any other steps can be taken.

Stop Adding Bad Debt!

Bad debt is when you borrow money (usually at higher interest rates) to buy something that goes down in value and produces no income.

Examples of bad debt:

– Credit card debt (if you don’t pay it off every month)

– Auto loans

– Payday and title loans

Stop racking up bad debt!

$5 per day on coffee is $150 a month and $1800 per year

Stop buying things you don’t need via debt! Downgrade or cancel your cable plan. Stop buying $10 lattes. Stop eating out as much (I’m really bad at this one!).

If you live in a swanky single apartment maybe you could bring on roommates, downsize, or some combination of both.

Don’t buy a a new car every 2 years. Buy a used car you can afford.

If it doesn’t involve clothing your naked body, providing shelter, eating, or isn’t required for your job, consider cutting it out.

Yeah, this is no fun, but it pays off in the longer term.

If you don’t address your bad debt, its like having an uncontrollable bleed and wanting to start training for a marathon. You must stop the bleeding and get stabilized before you can start training for a race.

Next up Part II: Fundamentals

In Part II I discuss the importance of a budget and setting goals. Not only will this help you get and stay out of the stabilization level, but will help you save more than you spend and prepare you for level III: Investing.

Today I read an interview MarketWatch did with Robert Kiyosaki: “‘Rich Dad’ author Robert Kiyosaki: If you’re investing for the long term, ‘you’re crazy’”

I’ve never read Robert Kiyosaki’s Rich Dad Poor Dad but I have read Unfair Advantage. From what I understand from speaking with folks who have read Rich Dad Poor Dad the principles in Unfair Advantage are very similar.

Robert Kiyosaki

I learned from reading his book. I didn’t learn a lot about specifics actions I could take but I did learn about mindset and principles of the wealthy.

For specifics he pushes his paid training classes and seminars pretty hard. I went to one of his “free” real estate seminars and it is sales heavy and content light.

I’ve never been to a paid Rich Dad seminar but I hope they have a lot more actionable content than the free one I attended.

Based on my exposure to the teachings of Robert Kiyosaki I will say that I agree with what he is saying. I just think he overcharges for training and actionable information.

[mc4wp_form id=”4538″]

Summary of Kiyosaki’s Interview

In the MarketWatch article above he says a few things:

Money isn’t money because it isn’t backed by gold

The rich don’t work for money they work for assets

He is predicting a 2016 market collapse

Describes himself as a “gold bug” and views gold not as an investment but an insurance policy and hedge

He states who he’ll vote for with the caveat the president doesn’t make any difference at this time

You know what, I agree with all of that, with the exception of calling 2016 as the year of the crash. It could be but I don’t know when stocks will crash and when they do I believe the Fed will step in and prop up prices.

Kiyosaki in Comment Pillory

But what I’m surprised by is the comments below the article. They weren’t all negative, but it seemed like most of the ones I read were.

Not a lot of substance besides name calling. I think the comments could provide some insights into how some retail investors think. They don’t want anyone raining on the stock rally parade.

These quotes are from people who, in my opinion, don’t understand the stock market or the economy.

Why I think Kiyosaki is Right

The Federal Reserve’s unprecedented action in propping up assets has created a huge bubble. The bubble is bigger than the dot com bubble in 2000 and the housing crisis of 2008.

Even if you think that the $4 trillion fed balance sheet is no big deal, there are other metrics that indicate the S&P 500 is overvalued. On average the P/E ratio of the S&P 500 has been around 15. It’s currently up to 25. Not exactly a bargain.

Source: http://www.multpl.com/

Gold is a hedge against Federal Reserve and central bank insanity. I don’t think gold should be the sole asset in one’s portfolio but could very well have an important place depending on your risk tolerance and other factors impacting suitability.

Gold (dark red) has outperformed each of the 3 main US indices by nearly 300% since 2000

I also know several people personally who have done very well investing in real estate. I think real estate is a great way to grow wealth with lot’s of tax benefits.

In the article Kiyosaki also discusses one practical strategy for buying a stock, first buying an option, as well as the importance of buying stocks at a great discount. Buying companies for less than their book value is classic Benjamin Graham.

I can appreciate if people don’t like Kiyosaki’s sales tactics as I don’t particularly care for them either. But I would like it if people could discuss ideas without immediately resorting to name calling.

If you think stocks are fairly valued based on fundamental factors, why?

The United States dollar has the privilege of being a widely used currency even outside the US. However, over a hundred years of failed policy, bad laws, and poor decisions have primed the downfall of the US dollar.

The World Reserve Currency

The US dollar is often referred to as the “world reserve currency”. For example, if a company in Canada were to buy something from China, it would not be uncommon for the exchange to be priced in dollars.

Oil is priced in dollars and despite efforts to move to renewable energy the world economy is (and will continue to be for some time) very reliant on fossil fuels.

This dollar dominance has given the United States a great advantage.

The global demand for dollars has helped keep the value of greenbacks up despite unprecedented US central bank manipulation in the form of trillions of new dollars being created.

Normally the creation of new dollars (inflation) would cause a great deal of upward pressure on consumer prices once these newly created dollars find their way into the real economy.

But because of the global demand for US dollars and US government debt these newly created dollars are exported throughout the world lessening the impact of inflation.

The Dollar Doesn’t have the Fundamentals it once did

There are a variety of historical reasons why the United States dollar was made the “world reserve currency”.

The 5,000 foot view is that at the end of World War II the United States had the most productive and largest economy in the world and US dollars were backed by gold.

I would venture to say that none of these reasons apply anymore.

The United States defaulted when President Richard Nixon took the gold backing from the dollar.

The United States effectively defaulted when it went off the gold standard in 1971 in what is known as the “Nixon Shock”.

Depending on what metrics you look at China has surpassed the United States as the largest economy in the world.

Dollars are not a good store of value and the US banking system is a pain to deal with. As an example, French bank BNP Paribas was fined $9 billion for violating US laws regarding who they could do business with.

There is Nothing Exceptional about the US Dollar

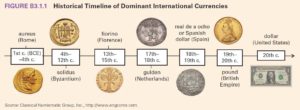

In history there are other examples of dominant countries with the privilege of internationally recognized currencies.

Dating back to first century Rome and the aureus, the solidus of the Byzantine empire, the Spanish dollar backed by the mighty Spanish fleet, the dominance of the British pound in the 19th and 20th centuries, and now the US dollar in the 20th century. Each of these powerful empires rose and fell and with it went their currencies.

The Days of the Global US Dollar are Numbered

The days of the US dollar as a world reserve currency are limited.

The United States was once a business friendly environment that allowed entrepreneurs to thrive and bring unheard of prosperity. The United States of today has a labor force participation rate at multi-decade lows, a lack of manufacturing, stifling regulations, the highest corporate tax rate in the world and a hopelessly manipulated fiat currency.

Countries are Already Looking for Alternatives to US dollars

German economist Ernst Wolff has talked about how smaller countries already tried to break from US dollar hegemony with lethal results.

Saddam Hussein of Iraq wanted to sell his oil for euros. Muammar Gaddafi of Libya wanted to introduce a gold backed currency. These men ended up dead.

Russia and China and other “BRICS” nations would benefit from moving away from dollars. They have already moved to trade more in the ruble and yuan rather than the US dollar. No doubt China and Russia would love to see the downfall of the US dollar.

It’s also possible, although this is just my own speculation, that China is positioning its national currency, the Yuan, as the replacement to dollars as the world reserve currency.

China’s documented actions, like importing and mining metric tons of gold and lobbying for and inclusion in the International Monetary Fund’s (IMF) basket of currencies, support this belief.

Because the dollar is a fiat currency it’s value is dependent on the strength of the United States economy, the political stability of the country, and the military power of the US armed forces. All of these factors are in decline.

As flawed a metric as it is, it’s worth noting that US average annual GDP growth has been on a downward trajectory for some time.

This election has surpassed the last presidential election in divisiveness. The level of political discourse seldom gets above name calling and personality. Discussing ideas and principles is an afterthought. Corruption and cronyism are rampant.

The United States military is a bloated mess. The US spends more on defense than the next seven combined. Despite this the military is bogged down in failed projects like the F-35 and hopeless engagements in the middle east.

The process of US decline has been ongoing. The downfall of the US dollar is not because of one particular event, but the cumulation of many bad policies and decisions.

One can look at a variety of events, the creation of the Federal Reserve in 1913, the Federal income tax, growing national debt, the post World War II perpetual warfare state, the Nixon Shock of 1971, the Iraq war fiasco, Federal Reserve actions in 2000 and 2008. Historians will debate what went wrong.

Don’t expect the fall of the US economic might to happen overnight. It’s been an ongoing process where one bad decision leads to another.

As the United States’ economy continues to decline, as the US government debt continues to grow unabated and as the US Federal Reserve continues to debase the dollar, more and more countries will move away from US dollars.

As this happens it will cause increased price inflation in the United States and the impact of US Federal Reserve recklessness will be more keenly felt.

It could be that 10, 20 or 50 years from now people look around and realize the United States is no longer the superpower it once was.

How I Protect Myself from the Downfall of the US Dollar

The downfall of the US dollar informs some of the investing decisions I make. I’m investing in physical gold, gold mining stocks, and quality foreign stocks trading at a discount. I’m also dabbling in blockchain investments, despite the added risk in that arena.

One of the easiest and in many respects best ways to buy and store physical gold is by opening up a Goldmoney personal account. To learn more about this opportunity and sign up for account, click here.

I get excited about the prospect of a gold backed debit card from that is not prepaid. I call this type of card a “point of sale gold backed debit card”.

Saving and Spending Gold

I believe that gold is going much higher in the coming years and that dollars will continue to lose value. Saving in gold makes a lot of sense.

Goldmoney is an excellent way to buy physical gold online and store it at locations around the world.

The whole point of saving is to have money to purchase goods and services in the future.

I don’t know any retailers that accept gold as payment. If I want to spend gold I have to convert it to dollars. That’s where the debit card comes in.

Prepaid versus Point of Sale

Prepaid gold backed debit card: Gold is sold for dollars in advance, dollars are spent Point of Sale gold backed debit card: Dollars are spent, gold is sold to cover sale and pay vendor in dollars

Point of Sale Gold Backed Debit Card

I was over on the “social medes” and asked Goldmoney co-founder Roy Sebag about this.

Roy says that this type of point of sale gold backed debit card should be available in 60 days, which would be early October.

Prepaid Debit Card

Goldmoney (formerly BitGold) currently offers a prepaid gold backed debit card. What this means is a person with gold in a Goldmoney personal account could sell all or a portion of his gold, the proceeds from the sale fund the prepaid card (denominated in USD, GBP, or EUR), the card arrives in the mail and then the debit card can be used to buy things just like any other debit card.

The card can be reloaded or auto-loaded by selling additional gold to load the card with dollars (or EUR or GBP).

If price inflation picks up even more this could be an invaluable tool.

Point of Sale Gold Backed Debit Card

What I am even more exited about is a gold backed debit card that sells gold at the point of sale.

The critical difference between a prepaid gold backed debit card and a point of sale gold backed debit card is convenience.

I could get a prepaid card from Goldmoney and then load it right before each purchase by selling just enough gold to cover the purchase.

I could also load it with a set amount of dollars but at that point the card is really just dollars–it’s no longer really gold backed.

For example, if I were to load a prepaid card with $500 and gold goes up 5% I would miss out on those gains. True, it would work in the opposite as well and protect from losses, but I anticipate a rise in the USD price of gold.

If the card is not prepaid Goldmoney does the math for me. When I make a purchase with my point of sale gold backed debit card, my savings remain 100% in gold until the charge comes across and only then is enough gold sold to cover the purchase.

I wouldn’t have to anticipate how many dollars I was going to spend and sell gold to cover it in advance. I could simply make the purchase and the gold would be sold to cover it.

Again, the difference is subtle but in practice I think a point of sale gold backed card provides the maximum convenience and gold exposure.

If you’d like to setup an account where you can save and spend gold, check out Goldmoney.com and get free gold when you setup and fund an account using this link: Goldmoney.com/r/1HWLl0.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

If an out of shape person is hemorrhaging blood due to an injury it would be absurd to focus on ways to improve their cardiovascular fitness until they are stable and healed from their injury.

If an out of shape person is hemorrhaging blood due to an injury it would be absurd to focus on ways to improve their cardiovascular fitness until they are stable and healed from their injury.

There are a variety of historical reasons why the United States dollar was made the “world reserve currency”.

There are a variety of historical reasons why the United States dollar was made the “world reserve currency”.

In history there are other examples of dominant countries with the privilege of internationally recognized currencies.

In history there are other examples of dominant countries with the privilege of internationally recognized currencies. Russia and China and other “BRICS” nations would benefit from moving away from dollars. They have already moved to trade more in the ruble and yuan rather than the US dollar. No doubt China and Russia would love to see the downfall of the US dollar.

Russia and China and other “BRICS” nations would benefit from moving away from dollars. They have already moved to trade more in the ruble and yuan rather than the US dollar. No doubt China and Russia would love to see the downfall of the US dollar.

The downfall of the US dollar informs some of the investing decisions I make. I’m investing in physical gold, gold mining stocks, and quality foreign stocks trading at a discount. I’m also dabbling in blockchain investments, despite the

The downfall of the US dollar informs some of the investing decisions I make. I’m investing in physical gold, gold mining stocks, and quality foreign stocks trading at a discount. I’m also dabbling in blockchain investments, despite the