I was having coffee with some new acquittances a few weeks back and mentioned I run a blog website about personal finance. I was asked a very good question which I don’t think I answered very well!

The question was: “Where do I start?”

I’ve been saving and investing for a long time and thus far this website has often focused on alternative and more aggressive investment strategies.

I can appreciate it’s hard (and likely unwise) to jump right into advanced investing so I want to write what I think are some things to consider when just getting started in the world of personal finance.

I originally wrote this as one big article. But realized it was too much! So I broke it down into three digestible parts. Today is Part I: Stabilization

Disclaimer: I don’t give financial advice. One of the reasons I don’t give investment advice here on my website is because there are exceptions to many rules and your personal situation could merit additional considerations. What is suitable for me might not be suitable for you.

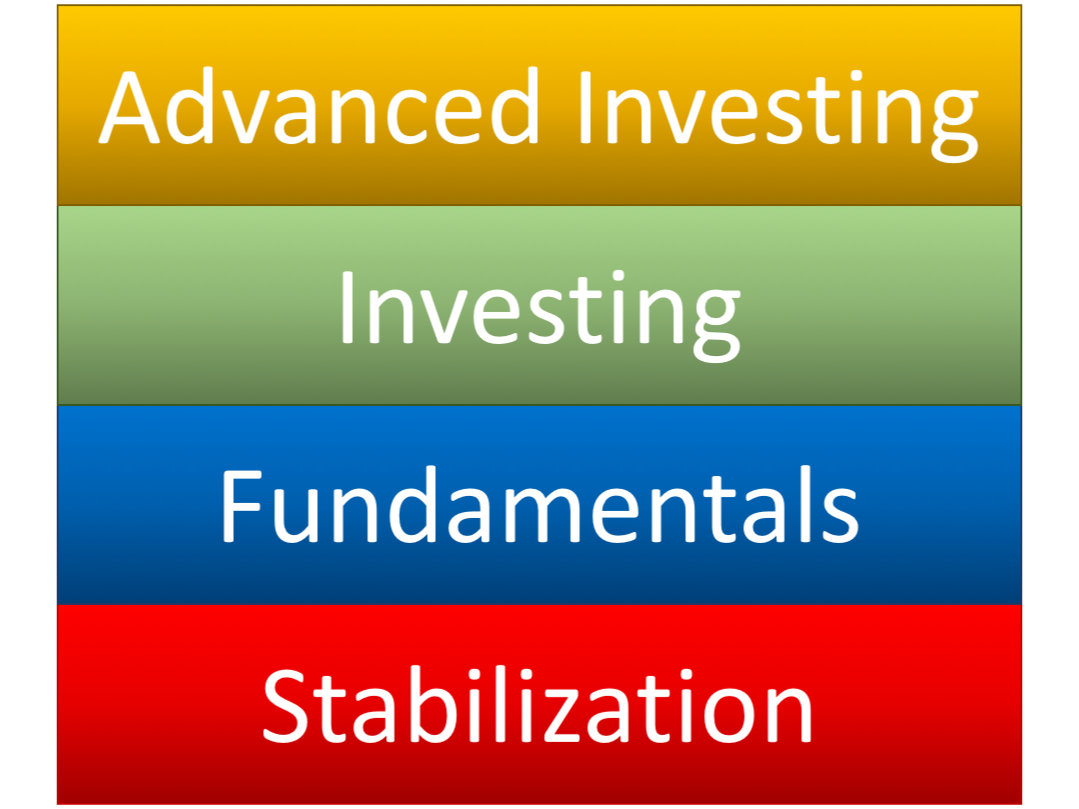

Basic Principles about Personal Finance

The Building Blocks of Personal Finance

I visualize these principles like building blocks. You have to have the lower levels in place before you can move to the upper levels.

Here are the basic principles:

– Debt for consumption is bad (Stabilization)

– You must produce and save more than you consume (Fundamentals)

– Have your money work for you (Investing and Advanced Investing)

The first level: Stabilization

In the health and medical field it is wise to make sure that a patient is stable and healthy before they try to fix some less pressing long term issue.

If an out of shape person is hemorrhaging blood due to an injury it would be absurd to focus on ways to improve their cardiovascular fitness until they are stable and healed from their injury.

The first step on the path to growing your wealth is to stabilize your financial situation.

These things don’t make you rich but they stop you from getting poorer.

One of the great financial traumas to an individual’s finances is bad debt. This bad debt must be controlled before any other steps can be taken.

Stop Adding Bad Debt!

Bad debt is when you borrow money (usually at higher interest rates) to buy something that goes down in value and produces no income.

Examples of bad debt:

– Credit card debt (if you don’t pay it off every month)

– Auto loans

– Payday and title loans

Stop racking up bad debt!

$5 per day on coffee is $150 a month and $1800 per year

Stop buying things you don’t need via debt! Downgrade or cancel your cable plan. Stop buying $10 lattes. Stop eating out as much (I’m really bad at this one!).

If you live in a swanky single apartment maybe you could bring on roommates, downsize, or some combination of both.

Don’t buy a a new car every 2 years. Buy a used car you can afford.

If it doesn’t involve clothing your naked body, providing shelter, eating, or isn’t required for your job, consider cutting it out.

Yeah, this is no fun, but it pays off in the longer term.

If you don’t address your bad debt, its like having an uncontrollable bleed and wanting to start training for a marathon. You must stop the bleeding and get stabilized before you can start training for a race.

Next up Part II: Fundamentals

In Part II I discuss the importance of a budget and setting goals. Not only will this help you get and stay out of the stabilization level, but will help you save more than you spend and prepare you for level III: Investing.

Today I read an interview MarketWatch did with Robert Kiyosaki: “‘Rich Dad’ author Robert Kiyosaki: If you’re investing for the long term, ‘you’re crazy’”

I’ve never read Robert Kiyosaki’s Rich Dad Poor Dad but I have read Unfair Advantage. From what I understand from speaking with folks who have read Rich Dad Poor Dad the principles in Unfair Advantage are very similar.

Robert Kiyosaki

I learned from reading his book. I didn’t learn a lot about specifics actions I could take but I did learn about mindset and principles of the wealthy.

For specifics he pushes his paid training classes and seminars pretty hard. I went to one of his “free” real estate seminars and it is sales heavy and content light.

I’ve never been to a paid Rich Dad seminar but I hope they have a lot more actionable content than the free one I attended.

Based on my exposure to the teachings of Robert Kiyosaki I will say that I agree with what he is saying. I just think he overcharges for training and actionable information.

[mc4wp_form id=”4538″]

Summary of Kiyosaki’s Interview

In the MarketWatch article above he says a few things:

Money isn’t money because it isn’t backed by gold

The rich don’t work for money they work for assets

He is predicting a 2016 market collapse

Describes himself as a “gold bug” and views gold not as an investment but an insurance policy and hedge

He states who he’ll vote for with the caveat the president doesn’t make any difference at this time

You know what, I agree with all of that, with the exception of calling 2016 as the year of the crash. It could be but I don’t know when stocks will crash and when they do I believe the Fed will step in and prop up prices.

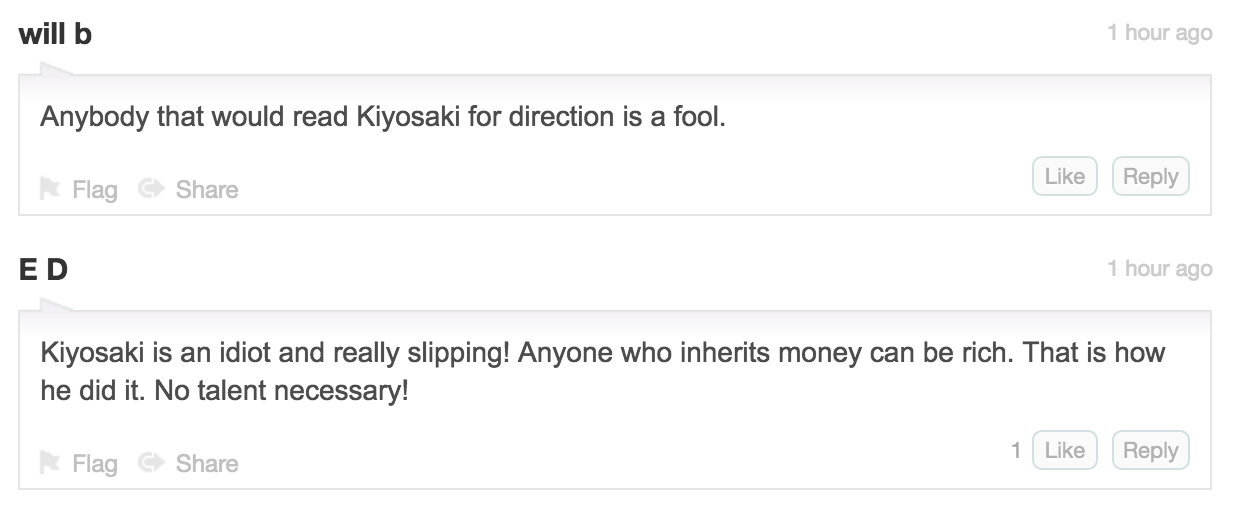

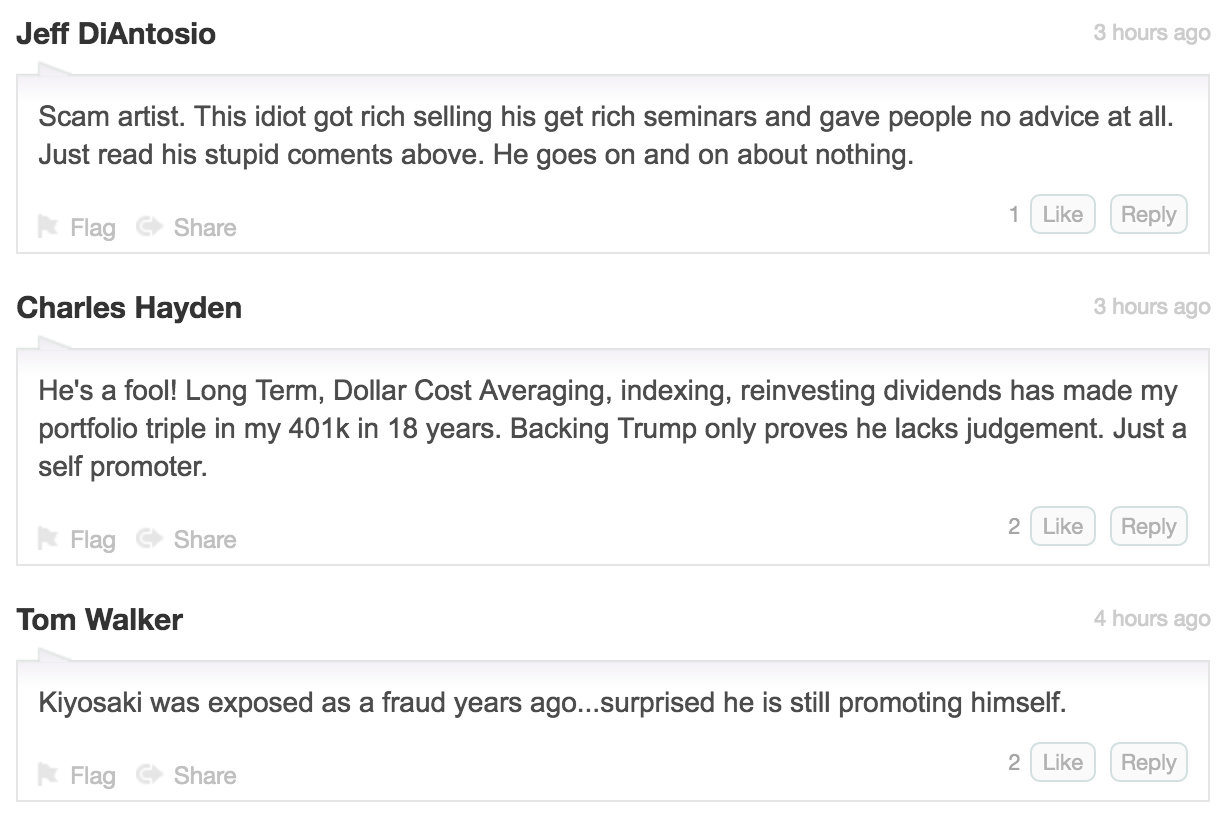

Kiyosaki in Comment Pillory

But what I’m surprised by is the comments below the article. They weren’t all negative, but it seemed like most of the ones I read were.

Not a lot of substance besides name calling. I think the comments could provide some insights into how some retail investors think. They don’t want anyone raining on the stock rally parade.

These quotes are from people who, in my opinion, don’t understand the stock market or the economy.

Why I think Kiyosaki is Right

The Federal Reserve’s unprecedented action in propping up assets has created a huge bubble. The bubble is bigger than the dot com bubble in 2000 and the housing crisis of 2008.

Even if you think that the $4 trillion fed balance sheet is no big deal, there are other metrics that indicate the S&P 500 is overvalued. On average the P/E ratio of the S&P 500 has been around 15. It’s currently up to 25. Not exactly a bargain.

Source: http://www.multpl.com/

Gold is a hedge against Federal Reserve and central bank insanity. I don’t think gold should be the sole asset in one’s portfolio but could very well have an important place depending on your risk tolerance and other factors impacting suitability.

Gold (dark red) has outperformed each of the 3 main US indices by nearly 300% since 2000

I also know several people personally who have done very well investing in real estate. I think real estate is a great way to grow wealth with lot’s of tax benefits.

In the article Kiyosaki also discusses one practical strategy for buying a stock, first buying an option, as well as the importance of buying stocks at a great discount. Buying companies for less than their book value is classic Benjamin Graham.

I can appreciate if people don’t like Kiyosaki’s sales tactics as I don’t particularly care for them either. But I would like it if people could discuss ideas without immediately resorting to name calling.

If you think stocks are fairly valued based on fundamental factors, why?

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

If an out of shape person is hemorrhaging blood due to an injury it would be absurd to focus on ways to improve their cardiovascular fitness until they are stable and healed from their injury.

If an out of shape person is hemorrhaging blood due to an injury it would be absurd to focus on ways to improve their cardiovascular fitness until they are stable and healed from their injury.