by John | Jul 17, 2016 | Preservation of Purchasing Power, The Inflation Bandit

If a frog is placed in boiling water, it will jump out, but if it is placed in cold water that is slowly heated, it will not perceive the danger and will be cooked to death.

– Motto of the Inflation Bandit

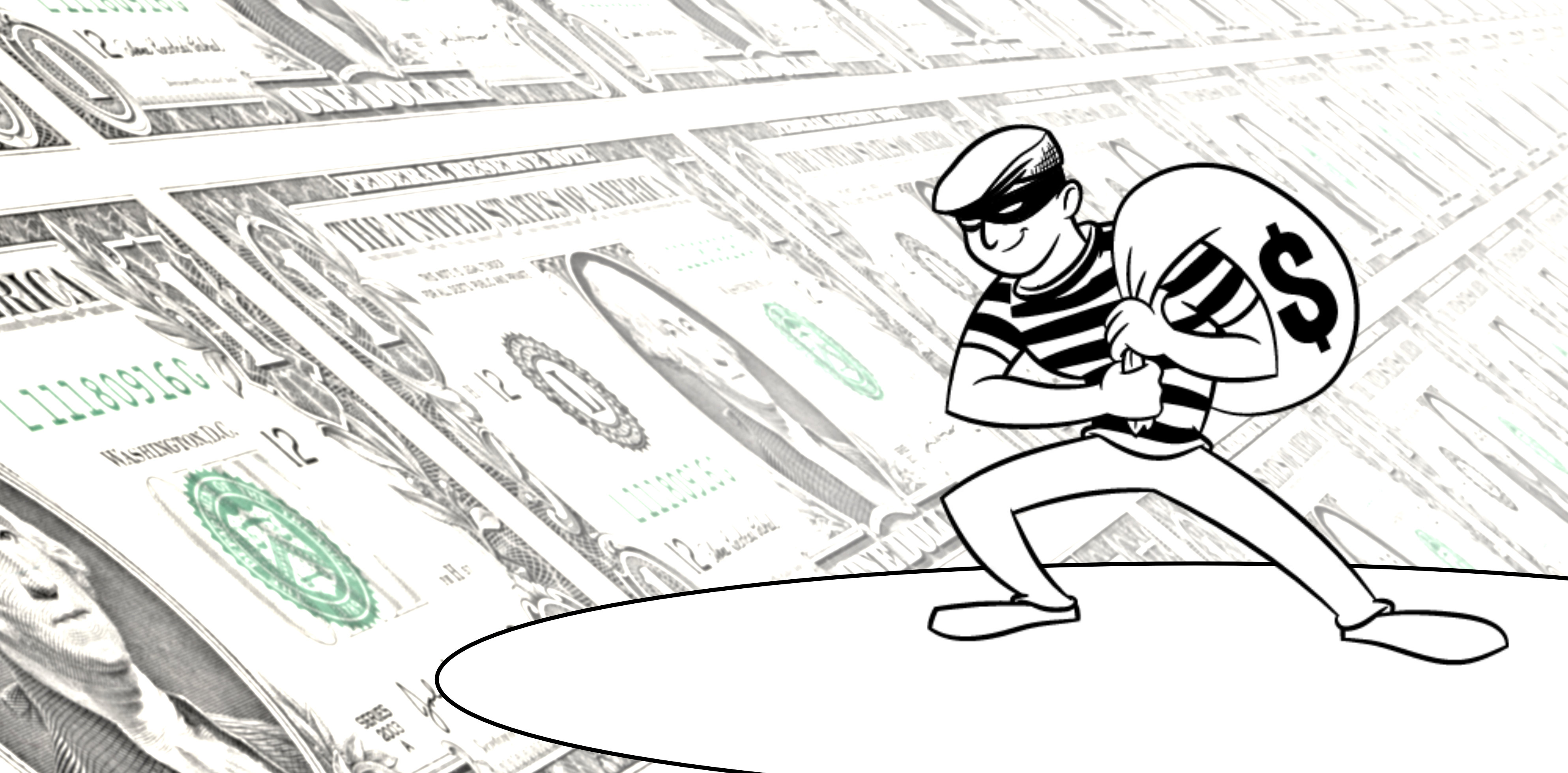

There is a thief called the Inflation Bandit. He steals YOUR money every year. The ‘Bandit has been robbing and plundering since 1913. He has never been caught and he has never been stopped.

The Inflation Bandit Stole Half Your Money Since 2000

He is a terrible scoundrel and has robbed Americans of millions and billions of dollars but he’s also clever in an evil sort of way.

He doesn’t break into banks and steal money directly–after all that would be dangerous and he’d be caught.

How the Inflation Bandit Operates

The dastardly Inflation Bandit just prints up new money that looks exactly like all the other real money and spends it.

By spending his fake money into the economy he causes prices to go up for everyone else.

So while he doesn’t take your money directly he accomplishes the same thing by stealing the purchasing power of your money.

One of the Million ways this Master Thief has stolen from you

If the Inflation Bandit finds a car he wants he prints up fake money and uses it to buy one for himself and maybe even a few for his friends.

He buys up enough cars so that there aren’t enough left on the lot for all the people with real money to buy one.

When buyers can’t get what they want they tend to get upset. They complain to the car dealer. “I want to buy one of those awesome new cars but you’re sold out! Get some more ordered from the manufacturer!”

So when the car dealer orders more cars from the manufacturer, the dealer thinks, “Hey, people really love these cars! I bet I can raise my prices when I get more. That way people who most want the cars will be able to get one and I’ll make more money.”

Plus the dealer doesn’t like it when his customer’s come in and complain because he doesn’t have cars available for them to buy.

So now the price is higher for people who still want to buy a car. Because the Inflation Bandit used his fake money to buy cars he effectively stole from people who now have to pay the higher price for a car.

Don’t blame Business

It’s really not the car dealer’s fault he sold the cars to a thief. He didn’t recognize the Inflation Bandit. The ‘Bandit wears many disguises and his fake money is indistinguishable from real money.

The Inflation Bandit doesn’t just buy cars, he buys eggs, milk, gasoline, houses, movie tickets, iPhones, computers, cable TV subscriptions. He buys everything with his fake money.

And it isn’t like once the Inflation Bandit spends his fake money it is gone. That fake money is now mixed into the economy and bids up the prices of everything else.

The Inflation Bandit gets slowed down

Back in the late 70s the Inflation Bandit got especially greedy and printed up a lot of fake money. This was causing prices to go up by over 15% per year!

The ‘Bandit got away with it for a few years but people were outraged.

The government cracked down on his efforts and by the mid 80s he was on the run and printed less of his fake money so prices rose by about 5% per year.

Not a bad take for this master thief. He was still stealing millions upon billions but people were less concerned when prices rose by 5%. After all they had been accustomed to prices rising by 15%.

The ‘Bandit learned his lesson

The Inflation Bandit knows if he prints too much fake money people will be outraged. People will demand he be stopped or at least slowed down.

So he’s gotten smarter and he’s gotten patient. He knows that as long as he doesn’t create too much of his fake money each year most people won’t notice it and people won’t be motivated to stop him.

The Inflation Bandit also knows that if people do notice the rising prices they’ll likely blame greedy businesses.

He has a good chuckle every time a business gets blamed for his crimes.

Have you heard of Price Inflation?

While the Inflation Bandit might not be a real person. Price Inflation is as real as it gets. Price Inflation is caused by fake money being spent into the economy.

Price inflation means things cost more and your money can’t buy as much. For example, in 2000, a dozen eggs cost $.96. In 2015 a dozen eggs cost $2.75. That is over a 186% increase in price over 15 years.

Source: http://www.statista.com/statistics/236852/retail-price-of-eggs-in-the-united-states/

In the egg example that is a 7% average annual inflation rate.

Since the year 2000 I believe price inflation causes your money to be worth 5% less per year on average. This means when you try to buy things from food to gas and yes even electronics like iPhones and computers you’re paying 5% more each year than you otherwise would have.

Source: http://www.shadowstats.com/alternate_data/inflation-charts

Another Way to Understand Price Inflation

Lets say you lost a $100 bill in your couch on New Year’s Eve in 1999 and you found it on Christmas of 2015.

With an average inflation rate of 5% that $100 bill in 2015 now has the purchasing power of about $46 in 2000.

You would be able to buy less than half as much stuff! That means you’ve lost over half your purchasing power!

Don’t get Slowly Boiled Alive!

Imagine if you woke up one morning and someone had stolen half of your money. If you’re like me you’d be outraged. You’d call the police and demand justice.

But because inflation causes money to lose value relatively slowly over time it’s harder to notice.

People have had half their dollar’s value stolen over the past fifteen years and few people complain about it.

Like the proverbial frog in water, if the water is heated slowly enough, it will not jump out and be boiled alive.

Most people don’t think much about inflation and they don’t care. But if you buy things using dollars you’re being robbed blind by the Inflation Bandit.

There are ways to protect yourself from inflation thievery but you first have to realize you’re being boiled.

If you’d like to hear about the ways I put the beatdown on the Inflation Bandit click here.

by John | Jun 16, 2016 | Capital Appreciation, Passive Income, Preservation of Purchasing Power, Real Estate

Buying Rental Property and Real Estate has helped create many a millionaire. Robert Kiyosaki, Barbara Corcoran, and even Donald Trump amassed fortunes via Real Estate.

Buying rental property is an investment that hits on three out of five of my Investment Goal Categories: Capital Appreciation, Preservation of Purchasing Power and Passive Monthly Income.

At it’s most basic level, investing in rental property consists of buying a property and then renting it out to gain monthly income.

I don’t directly own any rental property at this time but it is an area I’m investigating and learning more about.

Buying Rental Property has Five Great Benefits

1) Passive Monthly Income (Cashflow)

2) Equity Build-Up

3) Leverage Utilization

4) Very Favorable Tax Benefits (in the US)

5) Appreciation

Let’s explore the five benefits of buying rental property.

Passive Monthly Income

In many areas it’s feasible to purchase a rental property that generates positive cashflow each month. Even after making a monthly mortgage payment, taxes, fees and maintenance expenses, a good rental property can be have net positive cashflow from the rent payments of the tenants.

In many areas it’s feasible to purchase a rental property that generates positive cashflow each month. Even after making a monthly mortgage payment, taxes, fees and maintenance expenses, a good rental property can be have net positive cashflow from the rent payments of the tenants.

This meets one of my investment goal categories of passive monthly income.

Equity Build-up

Many banks will loan qualified persons enough money to purchase a rental property but typically require a 20-30% down payment. By renting the property you can use the rental income to pay the mortgage and continue to build equity in the property until you own it outright.

With equity in a property you have the option to choose between selling the property, taking a loan out on the property and re-mortgage it, or simply hold onto the property and continue to enjoy the monthly income.

Leverage Utilization

By taking out a loan to buy a positive cashflow rental property you are leveraging the capital you have to make more money. For example by using $16,000 for a down payment you could purchase an $80,000 property and rent it for $600 per month. Lets say after making the mortgage payments, paying property taxes, and other expenses, you are bringing in $150 per month in cashflow. At the end of the year that $150 monthly income would be $1,800 from a $16,000 investment, or over an 11% return. And that doesn’t even include the increase in equity.

Because of the use of leverage, price inflation actually reduces the cost of the remaining loan balance over time. This combined with the universal human need (and hence demand) for shelter even when the economy is not performing well makes buying rental property a great investment for preserving purchasing power.

Tax Benefits

I’m not a CPA or tax advisor, but I understand that when it comes to investment properties, mortgage interest, depreciation of the property, and other expenses that go into maintaining the property are tax deductible. Often times the 11% profit can be made tax free because of all the deductions the tax code (at least in the US) provides to real estate investors.

Appreciation

Partly due to price inflation, partly due to an increasing population and demand for housing, real estate prices tend to rise. So it is possible to grow wealth because the value of the property has gone up. While this is more on the speculative side of the housing and real estate market, appreciation can be a very nice bonus.

This meets one of my investment goals of capital appreciation as well as preservation of purchasing power.

What has stopped me from Buying Rental Property in the past?

- Capital I need money for a down payment. Most of my savings go into stocks and I want to buy a rental property with new money. So I’m going to start earmarking money for buying rental property. While it might be possible to buy a property with zero down I think this is reckless and irresponsible. It’s a good way to find yourself underwater on your mortgage. By making a 20% down payment you can weather a 20% drop in the value of the property and still be even in terms of equity. Plus if the property is cashflow positive, even if you are not making money via appreciation, you can still make money via cashflow and equity building.

- Knowing how to make an offer I would like to better learn how to coordinate having a loan pre-approved with making the offer. With real estate you have to be able to move quickly. In some markets if you go eat lunch to think it over the property will be sold by the time you get back.

- Maintenance Costs and Expenses If you know purchase price of a property and how much you can rent it for (by looking at similar properties being advertised in the same area) and what your costs are going to be you can determine if a property will be profitable (or not). However, I find the most difficult part to research is estimating maintenance costs. The hot water heater breaks, furnace needs repair, a crazy tenant tears up the place, etc. As someone who has been a renter all his life I don’t have a good sense of how much I need to budget for maintenance costs for a rental property. These costs are a huge factor in the profit and loss calculations.

There are five great reasons why real estate investing is a superb way to build and grow wealth. I’ll be sharing my progress in the coming months as I continue to learn more about real estate investing.

by John | May 19, 2016 | Capital Appreciation, Geopolitical Risk Protection, Liquidity, Passive Income, Preservation of Purchasing Power

Inflation has reduced the purchasing power of dollars by over 90%. Holding dollars is a sure way to lose value.

You need diverse and high quality investments to protect your purchasing power from the ravages of dollar debasement caused by inflation.

No one likes going to the store to find that a box of cereal is smaller and costs the same price or the same item now costs more.

Inflation is caused when private banks and the Federal Reserve increase the money supply. A larger money supply means there are more dollars in circulation.

This increase in dollars chasing the same amount of goods and services in the economy leads to rising prices or what’s properly called price inflation.

It is common to simply refer to rising prices as “inflation”.

I take steps to protect my Wealth from inflation

You can’t do anything about rising prices, but you can take steps that grow your wealth so that when you need to buy something you have more dollars (or Euros, or Yen) with which to pay the higher prices.

This is what is known preserving purchasing power and is a key concept.

I’m going to talk about two investments that help me meet my investment goals.

At the end of this article you’ll have an opportunity to subscribe to my Newsletter.

Newsletter subscribers receive details on the actionable ways I’ve chosen to protect myself from inflation that you can start doing today even if you only have a few dollars to invest.

These investments are not suitable for everyone and it might not be right for you, but the investment you’ll learn about immediately just by signing up below is an investment to which I’ve personally allocated several hundred dollars.

Let’s jump into two investments that help protect wealth from inflation.

Investments to Fight Price Inflation

Value Investing

8 March 2017 Note: I have further refined my value investing metrics in my article Better Metrics for Value Investing.

Believe it or not, there are certain stocks that trade below their book value.

Investopedia tells us that book value is “the total value of the company’s assets that shareholders would theoretically receive if a company were liquidated.”

So, if a stock is trading at a book value of .5, that means if you could buy all the shares then liquidate the company, you would make 50% per share. Now I’m not planning on buying all the shares of a company and liquidating it, but by purchasing quality stocks below book value there is built in downside protection.

There are other criteria as well, and stocks that meet the criteria are value stocks:

- Price to book less than 1.5

- Price to earnings less than 15

- Return on equity greater than 8% on average per year

- Dividend Yield

Value investing is how folks like Warren Buffet became billionaires.

When I allocate capital, I do so to areas that meet one or more of my Five Investment Goal Categories.

Value Stocks hit on all Five Investment Goal Categories. Value stocks serve to preserve purchasing power, provide capital appreciation, can create monthly income via dividends, foreign value stocks help hedge against geopolitical risk, and stocks tend to be among the most liquid assets.

One such stock I purchased back in October 2015 is Sberbank of Russia, ticker SBER on the London Stock Exchange. I have a offshore brokerage account (which is perfectly legal) that allows me to trade a variety of foreign stocks directly on foreign exchanges.

SBER has a price to book of 1.2, a price to earnings of 13.8, a return on equity of 9.53%% and a modest yield of .4%.

Source: MorningStar.com and TDAmeritrade.com

I purchased 100 shares of SBER at 4.772 USD, my brokerage firm charges me a $40 commission for both buy and sell. Sberbank is currently trading at $7.556 so I’m sitting on an unrealized 58.34% profit.

Not all of my trades go this way of course. I have $10,240 cost basis in my international brokerage account, and my account value is currently around $8,950. So I have both unrealized gains and losses that currently net out to unrealized losses. However, for value stocks, my time horizon is in the 2-3 year range and I’m very confident that in that time I’ll be in the black.

I’ll be devoting future videos and posts to value investing, which I feel is very important.

Precious Metals

The second investment I’ll touch on today are Precious Metals.

In my culture we have a saying, “Gold is the money of kings, silver is the money of gentlemen, barter is the money of peasants – but debt is the money of slaves.” Okay, that is actually a quote by Norm Franz from his book Money & Wealth in the New Millennium: A Prophetic Guide to the New World Economic Order but I’ve adopted it.

Gold took a serious pummeling since the latter half of 2011 through 2015. But despite that correction Gold has been up over 15% in 2016 and is up over 240% over the last 25 years. Yes, 240%.

Gold can’t be printed out of thing air and has been used as money throughout human history.

Gold also hits on four of the five criteria to varying degrees. Gold has a 5,000 year history of preserve purchasing power, it is unrivaled in this category.

If gold is undervalued, as I believe it is right now, it could provide capital appreciation (in purchasing power terms, not just dollar terms). Gold is a superb hedge against geopolitical risk, and while physical gold bullion is not liquid at this time compared to fiat cash, it is more liquid than say real estate or a business.

Despite large gains, I believe that Gold is still a great value and will go even higher and so I have chosen to invest a portion of my savings in physical gold.

I began purchasing physical gold and silver in December of 2012 and as a result I’m underwater on some of my positions. I’ve continued to make purchases throughout this time and overall I need gold to rally back to $1,400 to break even, and silver back to $24 to break even.

I would have preferred to have bought gold at the lows of $1,040, but as yet I don’t have a crystal ball that allows me to perfectly time the bottom of markets and I firmly believe that based on the fundamentals gold will make new highs in excess of $2,000.

When it comes to gold I firmly believe that it is better to be early to party than late. If the dollar goes down dramatically in value in a crisis situation there simply might not be any physical gold available for sale.

I also own multi-hundred dollars worth of gold through a relatively new and innovative way to purchase and store physical gold with very little up front investment. The benefit of this new way of owning physical gold is that it is very liquid as well.

Inflation is a destructive force, but with the right investments I’m able to position myself to continue to grow my wealth in spite of rising prices. I’ve discussed two assets I own: value stocks and precious metals that could be helpful as you make your own investment decisions.

There is exclusive information I ONLY share with subscribers of the HowIGrowMyWealth email Newsletter. Sign up using the form above!