My first article on this website was over 5 years ago, Inflation Destroys Dollars. I certainly did not have any idea that the price inflation would be triggered by the government’s response to the COVID-19 pandemic. I certainly didn’t anticipate the lockdowns and supply chain disruptions back in 2016.

I know the fiscal and monetary policy pursued by the United States and virtually all the world: money printing, onerous regulations, taxes and spending, would eventually result in significant price inflation. Government response to COVID-19 has made the situation worse and pulled the day of reckoning forward but it certainly isn’t the largest factor.

Timing is always a challenge and I was quite early.

Price inflation is here and it is happening fast enough where people notice it and are actually talking about it. Depending on who you trust and how you measure it, prices are rising at a rate of 6-10% per year now. I think what is interesting is that the government’s own numbers (the CPI-U) shows inflation at 6%. This is far beyond the 2% the Federal Reserve has been calling for.

In Inflation Destroys Dollars I write about how gold and silver are an inflation hedge. On 16 May 2016 when I wrote that article, gold was trading at $1,252 per ounce. As I write this it is currently up to $1,864.61, an increase of 48.9%. That is an annualized return of roughly 7.5%.

On 16 May 2016 Silver was trading at $17.14. It is now trading at $25.29. That is a 47.5% increase for an annualized return of approximately 7.3%.

So, if you think that inflation has been somewhere between 4% and 8% over the past five and a half year, gold and silver have on just kept up with inflation during this timeframe. Not bad but also not great. Gold and silver remain the boring reliable hedge and that is a good thing.

Value Stocks as an Inflation Hedge

Value stocks are another asset class I mentioned in Inflation Destroys Dollars. I didn’t mention specific funds. I have made some of my own individual value stock picks with some fantastic picks, but also some not so good picks.

Vanguard’s Selected Value fund (VASVX) is a mid-cap fund that could serve as a proxy for “value stocks”. It was trading at $26.41 on 16 May 2016. It is currently at $33.39. This is a return of 26.4% and an annualized return of 4.3%. Not stellar as I would not say this has kept up with inflation.

The Vanguard Value Index is a large cap value fund (VVIAX). It started this period at $32.49 and is up to $56.68. This is a return of about 74.5% and an annualized return of 10.65%.

A final example to look at, Vanguard’s Mid-Cap Index Admiral Shares Fund (VIMAX) started in this timeframe at $150.33 and is now at $320.62. That is a total percent return of 113% and an annualized return of 14.7%. Much better.

Compare those to the Vanguard 500 (VFIAX), which started this timeframe at $184.53 and is now at $432.9. The total return of this fund was 134.6% an an annualized return of 16.77%.

So while value stock fund did beat the rate of inflation and are a good hedge, they didn’t outperform your vanilla S&P 500 index fund.

Bitcoin as an Inflation Hedge

Compared to gold and silver, Cryptocurrencies, particularly Bitcoin has had all the action.

On 16 May of 2016 a Bitcoin was trading at about $454. Today Bitcoin is trading at $64,346. That is an astounding increase of 14,073% or an annualized return of about 146%.

Clearly Bitcoin has outperformed Stocks, Gold and Silver during this timeframe in an astounding way.

I own Bitcoin and I’m not anti-bitcoin. But I’m also not a Bitcoin maximalist. I think it is possible and perhaps even likely that Bitcoin will be replaced with a superior cryptocurrency that has some combination of faster transactions, higher transaction throughput, anonymity and or additional features. In my view Bitcoin in its current state is too slow and transactions are too costly for it to work as a medium of exchange for day to day transactions. These views are very unpopular with Bitcoin maximalists that ignore or downplay Bitcoin’s weaknesses.

However, Bitcoin has provided an incredible return and far outpaces inflation.

The 14,073% return is not just a result of inflation, although it is increasingly being viewed as a safe haven alternative investment.

Bitcoin has had several great tailwinds 1) It is an emergent asset class 2) It is trendy and popular and gets media attention 3) It is viewed as a Federal Reserve / dollar debasement hedge in place of gold.

Inflation Hedges

Protecting one’s wealth and purchasing power from inflation is important. Just keeping up with inflation is not ideal either, if the assets are not tax advantages, the government will tax the “gains”, and so purchasing power is eroded.

Let’s look at a simplified example. Say you frequently buy a widget or pay a service that costs $100 per year. Say the price goes up 5% per year due to monetary inflation. You also have a $100 investment that also goes up 5% per year. You’re still not keeping up with inflation because of taxes. If your $100 investment goes up 5% to $105, the government is going to want some taxes on that $5 gain. Say you’re on the hook for 15% capital gains taxes, the government is going to take their share and leave you with a $4.25 gain.

So you now have to come up with another $0.75 to pay for the item or service. Scale this up to include all of your expenses for the year and you see that you need to not only keep up with inflation, but exceed inflation so you have the money to pay the taxes on the gains.

In order to keep up with inflation your investment would need to be in a tax advantaged account that would lower or eliminate the tax burden owed or (again assuming a 15% gains tax) you’d need the investment to go up by about 5.9%.

This also shows how insidious inflation is. Not only is money worth less, but the government taxes the gains, even if there was no gain in terms of purchasing power.

One other thing to keep in mind, in the United States at least, realized gold and silver gains are taxed at the generally higher income tax rate rather than capital gains tax rate.

Are Gold and Silver Great Inflation Hedges Anymore

Gold and silver might not be very good inflation hedges anymore. If I owned gold or silver I wouldn’t sell unless I needed to rebalance my portfolio. I would expect these assets to at least keep pace with inflation, but unless the demand for gold and silver increases in excess of new supply, I don’t think gold and silver will beat inflation in the way needed in order to truly hedge for inflation when accounting for taxes. While it has produced a positive return in excess of inflation, it certainly hasn’t been a fantastic play over the last five and half years since I started HowIGrowMyWealth.com.

I subscribe to various financial newsletters. I still have a lot to learn. One such newsletter I subscribe to is written by person who has a lot more money and an exponentially bigger following than I do. So obviously he is doing some things right.

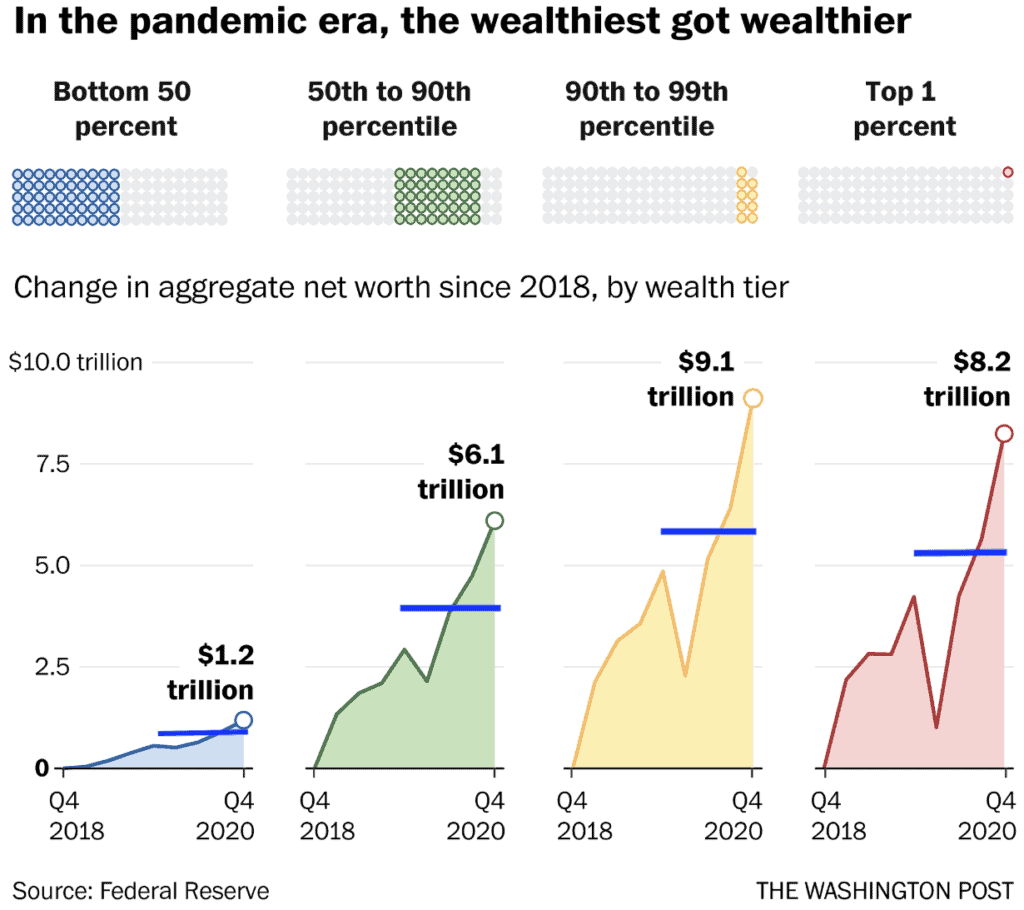

But I’m amazed by what I read recently. He posted the following image and wrote: “In other words, if there had been no pandemic, aggregate net worth for each wealth percentile would likely be around where the blue lines are today. But due to the pandemic, we’ve unexpectedly made a whole lot more.”

That is very “unexpected” for someone like me that believes hard work, innovation, capital investment and fiscal discipline are what produce wealth.

What has happened since March of 2020? Many businesses have closed, some permanently, the government has “printed” money and spent it, people have been paid to stay home and not work, and countless people have passed away. I would never have expected shutting down large portions of the economy, printing and spending money would result in wealth creation.

Now I don’t doubt that the upper income brackets have increased their wealth in real terms. However, I can’t believe that in real terms wealth in the United States has increased. Why? Because the dollar buys much less than it did pre-pandemic. Commodity prices have gone up, housing prices have gone up, and food prices have gone up. The wealthy, even accounting for multi-million dollar mansions, private jets, and the finest organic vegan food cooked by a private chef, still don’t pay as much on food, housing as transportation as the poor when viewed as a percentage of their whole net worth.

At best this wealth effect is pulling forward future returns. But I suspect, that given the rising prices, most people are worse off as a result of the pandemic. But it is amazing the attitude it shows. At no point in that newsletter did the author question why closing large portions of the economy, printing and spending money was a recipe for wealth building.

After all, staying home and collecting a check is a lot easier than going to work to produce goods and services. So why bother encouraging businesses or workers.

The tax and spend philosophy, the universal basic income philosophy, the rejection of the basic principle of economic scarcity are consistent with the belief that a government can pay people not to work, run deficients and print in order to create prosperity. It’s all part and parcel with the United States rapidly shifting away from free market enterprise and towards collectivism and state control. This hasn’t worked in the past but maybe this time is different?

I wrote a little bit about the mechanics of shorting stock and naked shorting of stock. Some version of what I described in Scenario C happened to a hedge fund called Melvin Capital. Melvin Capital was heavily short GameStop (GME). The price rose rapidly and it sounds like they didn’t have enough money to close their position. According to the New York Post, “Hedge funds Point72 Asset Management and Citadel gave a $2.75 billion capital infusion to Melvin Capital earlier in the week, enabling it to close out that position with a large loss.”

Remember that name: Citadel. Citadel is a huge client of the trading platform Robinhood. Robinhood sells trading information to Citadel.

The retail traders on Robinhood trade for free. On platforms like Google, Facebook and Twitter where you get something for free you are the product.

Citadel is Robinhood’s customer. Without clients like Citadel Robinhood doesn’t make any money. So there is motive for Robinhood to want to keep Citadel happy.

Was there any hanky-panky between Citadel and Robinhood? Did Citadel tell Robinhood to halt trading so a hedge fund they sank billions into could close their positions? I don’t know. I don’t have evidence that this happened. But the motive is definitely there. Motive by itself isn’t sufficient though.

Should someone look into what happened? Don’t worry: Treasury Secretary Janet Yellen is on it! She is the first female Treasury Secretary and she is on the case.

Treasury Secretary Janet Yellen

Former Fed Chair and now Treasury Secretary Janet Yellen did very well for herself while between jobs. She has made at least $7.2 million in speaking fees. This number includes some $800,000 paid to her by Citadel. The same Citadel who is a huge client of Robinhood and bailed out Melvin Capital.

But guess what, despite what I think is a clear conflict of interest. Treasury Secretary Janet Yellen will be presiding over a regulatory hearing regarding the GameStop saga. So what are the chances that the Hedge Funds come out the loser in all this? I don’t think they are very good.

I don’t think regulations help that much anyway. Many do more harm than good. But let’s say you believe we need strong financial regulation. How is that supposed to happen when the regulators are getting millions from the people they are supposed to be regulating?

If anything happens, I suspect some of the more prominent “redditors” will be accused of something and trotted out as the scapegoats and the hedge funds will get away free. Even though the hedge funds were the ones who lost money due to them having poor risk management and being incredibly short a stock.

I’m not an attorney but from an ethical perspective I don’t see how the redditors buying the stock did anything wrong in seeing hedge funds were over-short a stock and taking advantage of what Melvin Capital were doing.

So what is the Lesson Here?

This is just one example of how the foxes are guarding the hen house.

Going back to the GameStop drama: some people probably made money buying GME but as of writing this it is back under $55. I suspect most redditors lost money on GME. GME peaked at around $483. I’d like to know how many people knew to buy GME at say $20 or less and then decided to sell at $400 or even $300.

Maybe some of the folks who lost money on the GME trade believe it was worth it just for the chance to stick it to a hedge fund. As for myself I’m not in favor of cutting off my nose to spite my face.

It is really hard to bet against the house at their own game and win. The hedge funds are too powerful and they pay the regulators’ speaking fees. Even the folks in the “big short” of 2008-2009 were gutsy insiders.

That is one of the reasons why I like a 10-20% allocation to physical gold and silver. Despite manipulation in the futures markets for these commodities, you are still opting out of the tradition financial system.

I was wrong in my prediction regarding the 2020 election season. I thought it was most likely the red team would retain the senate with Biden in the oval office or what I called “Scenario 3”. I wrote “Scenario 4” was second most likely and that is what happened: Biden in the White House with the blue folks in control of the Senate.

My understanding of the Senate also lacked nuance. While the blue team does have a simple majority in the Senate thanks to 50 members plus Vice President Harris breaking ties, only certain legislation can be passed without a 60 Senator majority. With a simple 51 vote majority the Senate is (somewhat) limited in what legislation it can pass to what is authorized in the budget reconciliation process.

My very superficial understanding of the reconciliation process is that it must pertain to spending and revenue and can only be used once per year. It could be used to raise or lower taxes (for the blues it would be raise) and who knows what other tomfoolery.

Taxing and Spending

But even with the blue group being somewhat limited by the reconciliation process, I can guarantee new taxes and more spending. Perhaps Wall street either likes the tax and spend approach, or the market had already priced in a Biden-Harris Administration, or perhaps it is simply the removal of the election uncertainty for the next two years, combined with vaccine optimism, regardless of how the election turned out.

In any case the S&P 500 is up nearly 9% since November 5th.

Wall Street does seem to love spending, and doesn’t seem to care about the national debt. So while I wouldn’t expect the stock market to crash because of Biden’s tax and spend approach, I do think the economy would fare better under low taxes and fiscal discipline.

Perhaps Trump will say the stock market is magically back in a big, fat, ugly bubble again now that he isn’t in power. I think the stock market has been in a bubble for a while. However, the ability of the powers that be to keep the bubble inflated has far surpassed what I believed possible.

Debt

Even though the blue team is known for spending, their tax hikes don’t cover the bill. To be fair red team doesn’t have many fiscal conservatives either. The national debt goes up regardless of who is in power.

I predicted back in January of 2017 that the US nation debt would go to $40 trillion under Trump. However, under the Trump administration, the debt only went from about $19.9 trillion to about $27.7 trillion. Granted I thought Trump would win reelection at the time I made that prediction and he would have 8 years to run up the debt by over $20 trillion.

Unless Trump runs for office again and wins, my $40 trillion prediction was wrong. However, I think the national debt will go to $40 trillion by the end of 2024.

I think over the next four years it will go from $27.7 trillion to over $40 trillion. It would mean about $3 trillion per year. In 2020 the national debt increased by $4.2 trillion. I’m sure Biden will be looking for a big spending package in 2021 to get his administration started off with a bang.

Government spending financed by debt reduces the value of dollars, so more dollars are required for later stimulus in order to have the same effect. For example in 2008, when the banks were being bailed out the debt went up by about $1 trillion. Then the next year the debt went up by $1.8 trillion.

Granted 2020 had COVID-19 and lockdown crisis, but that hasn’t gone away. In 2018 and 2019, with the economy supposedly humming along and no large-scale military engagements, the debt still increased by over $1.2 trillion each year.

My $40 trillion prediction is based on the national debt going up by $4-5 trillion in 2021, followed by $2.5 trillion per year after that.

This is one reason why interest rates can’t rise. The treasury issues debt at a variety of maturity rates. But as interest rates rise, that means the government has to pay out more money on the debt. The treasury is already paying about $393 billion per year in interest at current rates.

In June of 2007 the yield on a 10 year treasury was 5%. In the wake of the 2008 financial crisis it has steadily fallen. While still stupidly low, the 10 year treasury yield has been rising. In July of 2020 it was as low as about 0.5%. Since then the yield has risen to about 1%. As I said before it is still stupid low, in contrast the 10 year treasury yield was 15% in the early 1980s.

However, the market is addicted to low interest rates. If the 10 year yield continues to rise and gets to 3 or 4% I think that would be devastating for stocks. As mentioned above it would also dramatically increase amount the treasury would need to pay in interest. For example at 0.5%, $2 trillion would cost $10 billion, but at 3% it jumps up to $60 billion. But it isn’t just the new debt, as older debt expires and the borrower gets paid back, the treasury issues new debt to pay for it, which must be issued at the new rates.

I’m sure the Federal Reserve will step in and drive the yield back down before that happens. The Washington elite definitely don’t want a stock market crash to happen when the blue team is in control of the government.

Warfare

I think the Biden-Harris administration is much more likely to increase hostilities in the world. Despite all his faults, and alienating allies of the United States, Trump didn’t start any major military engagements in the world. I believe Biden-Harris will follow the Bush II and Obama approaches to foreign policy.

More war is good news for “defense” contractors, but less positive for everyone else. The loss of human life in war is the most tragic element and the most important reason to avoid military action except as a last resort. A distant second reason for avoiding war is that bombs, drones and aircraft carriers are expensive and contribute to the national debt. Surely the military action, as it always is, will be dressed up flowery rhetoric to make it seems necessary, noble and courageous.

Wealth Management

I think a 10-20% allocation to precious metals is as important now as it ever was. Gold has been down and sideways since the new high was made in August of 2020. It seems to have support at around $1,790 per troy ounce. I think this is consolidation prior to the next leg up.

Stocks only seem to go up. Valuation and fundamentals don’t seem to matter.

While I always have some exposure to the stock market, I’ve missed out on the some of the gains of the last 8-9 years since I’ve been underweight US stocks. I’ve been waiting for a buying opportunity. I was considering buying in around March of 2020, but I expected the markets to go lower.

I was wrong.

The powers that be are able to maintain the stock market prices far beyond what makes sense to me. I’m planning on averaging into various mutual funds over time. Perhaps my capitulation is a sign that the top is near!

Despite all the challenges from higher taxes, more regulations, debt and lockdowns, there are still productive businesses out there. While I think Biden/Harris and their allies on the blue team will make things worse, there are still plenty of reasons to be optimistic. Being in a “bunker mode” for the past 8 years has cause me to miss out on a significant stock market rise. At some point I think the dollar will crash and maybe stocks will go down too, but that is what the precious metals are for.

I try to avoid being political on this site or at least be apolitical. For example I did not endorse either United States presidential candidate. However, government and politics has so permeated nearly every aspect of our lives in the United States it is impossible to discuss finances and the economy without being at least somewhat political.

Voting outcomes in key swing states are left unknown. But there are a limited number of outcomes with respect to who controls the government. If one party controls the house, senate and presidency, that party (or team) has the opportunity to make sweeping changes to the legal and regulatory framework of the country, with some check on what they can do enforced by the judicial branch/supreme court.

The current balance of power in the United States house of representatives is 232 blues to 197 reds with one libertarian and five vacancies.

Although the results are not finalized we know the blue team will retain control of the house of representatives with something like 227 members (218 are required for a party to control the house). Net the red team will have picked up some seats. Some of the elections are still in counting limbo but those numbers will not change by more than 2-3 seats. So until the next election cycle in 2022 the blue team is guaranteed to continue to control the house.

The current United States senate party division breaks down at 53 red, 45 blue, and 2 independents aligned with the blue team. In other words effectively 53 red 47 blue.

Current senate race results show 48 red and 47 blue. Current forecast predict a 49-49 split with one toss up and one runoff. 51 seats are required to have control of the senate. In the event a vote in the senate is tied, the vice president is the deciding vote. So if the senate does come down to be a 50-50 split, whichever party controls the White House will also control the senate.

Of course there is also the presidency which is up for grabs. I’m inclined to believe that Biden will be declared the next president, regardless of who was actually elected because I think the blues are probably better at “counting” votes. But Trump could still win. Either way this leaves just a few possible scenarios for control of the government.

Remember, if the senate is 50-50 splite, which is possible, control of the senate would go with the team with people in the White House.

Scenario 1: Trump Presidency with Red Team Control of the Senate

In this case there will continue to be a lot of gridlock. There will be a small(er) stimulus bill and some legislation but for the most part not a lot will change. This is the scenario we’ve been in for the past 2 years. Trump could still pull off a victory if he wins Georgia and then if lawsuits could uncover enough voter fraud to turn the right combination of Michigan, Wisconsin and Pennsylvania back to him. It isn’t looking good for Trump but it is also possible that Arizona or Nevada, if they ever finish counting votes, could go to Trump.

Scenario 2: Trump Presidency with Blue Team Control of the Senate

I think this would result in even more gridlock. Congress would not have enough votes to override presidential vetos because that requires a 2/3 vote in both houses. So there would be a lot of back and forth of the blue controlled congress blaming and vilifying Trump and vice versa.

Scenario 3: Biden Presidency with Red Team Control of the Senate

In this scenario Biden is president (at least ceremonially) and Harris is VP. The red team would need to have at least 51 seats. I think this is the most likely scenario but it is by no means certain. Even though at this time I think Biden will be declared president (or if you’re feeling romantic elected) Trump could still pull off some type of upset.

In the senate, to get to 51, the red team would need to win Alaska (seems likely), and one of the Georgia seats (which also seems likely). Then, they would need to win the Georgia run-off on January 5 of 2021, which seems possible.

Note: Explanation of the Georgia run-off can be found here.

North Carolina is being called as a tossup or advantage red team (depending on the source), the red team candidate is currently in the lead by over 96,000 votes with 97% reporting.

If NC does go to the red team candidate and both Georgia seats do as well the red team could get to a 52-48 majority in the Senate.

I think there would be moderate gridlock because Biden was a senator for many, many years and has relationships with the senators and I think the red team senators are much more likely to compromise and go along with the blues. Not only that, but the blues would only need one or maybe two reds to come over to their side and then Vice President Harris could vote to break ties.

Scenario 4: Biden Presidency with Blue Team Control of the Senate

I think this is the second most likely scenario. Again we’re assuming a Biden/Harris administration. Biden would be president but I’m not sure who would be the de facto president in this case.

Blue team would need to win Arizona (seems likely), North Carolina (which is listed as leaning that way). These two would get them to 49, then they’d need to win the Georgia seat (which is listed as a toss-up, although the red is up by over 90,000 votes). This would get them to 50, plus Vice President Harris gets 51. They could also win the Georgia run off election which would get them to 51 even without Harris.

In this scenario the blue team would have the power to implement lots of changes. They could implement the green new deal, raise taxes, increase regulations, expand the affordable care act, provide medicare for all, restrict gun ownership and anything else really. They would probably be limited only by their fear of voter backlash in the next congressional election cycle.

A blue government might be limited in some instances by the supposedly conservative Supreme Court (which is 5-4, since Roberts tends to side with the liberal Justices). However, they could try to implement their plan to stack the supreme court and appoint as many new justices as needed to prevent having their laws struck down as unconstitutional. I don’t know enough about this to have an opinion if they would be successful or not.

What it all might mean

If what I estimate to be the most likely scenario does indeed come to pass the US will face a Biden presidency with a blue controlled house and red controlled senate.

The president has a lot of control over foreign policy. Doubtless the US will be cozier with China and Iran and markets don’t seem to like trade wars, so that would be positive for stocks. However, when there were trade wars, the Federal Reserve has stepped in to be accommodative and the markets love stimulus.

Although purportedly neutral, the president appoints the head of the Federal Reserve and in my opinion (despite protestations of neutrality) the Federal Reserve will do what the president wants for the most part.

While bad for the economy, artificially set rates are great for presidents because they goose asset prices and the stock market is used as a proxy for how the economy is doing.

I doubt there will be a stock market crash, as fiscal stimulus will be used to prop up asset prices. I do expect deficits to continue to grow unchecked and I think gold and the right foreign stocks will do well.

Worst Case Scenario

With a Biden presidency and blue team ruled congress a lot of socialist policies will be implemented. Higher taxes, a stricter COVID-19 response, wealth redistribution and increased government regulation. I think this will be negative for the economy with the middle and lower classes hurting the most. Alternative energy companies and select industries would do well in the US, but gold and foreign stocks would also benefit.

Depending on where you get your news you might think the fossil fuel industry is going the way of the dinosaur. This combined with other factors have made investments in oil and gas companies like Exxon Mobil (XOM) and Royal Dutch Shell (RDSB) unpopular.

I’m long XOM and RDSB and I think these companies are undervalued and will produce solid returns over the next 10-20 years.

Why would I invest in these companies when oil and gas industry are dying?

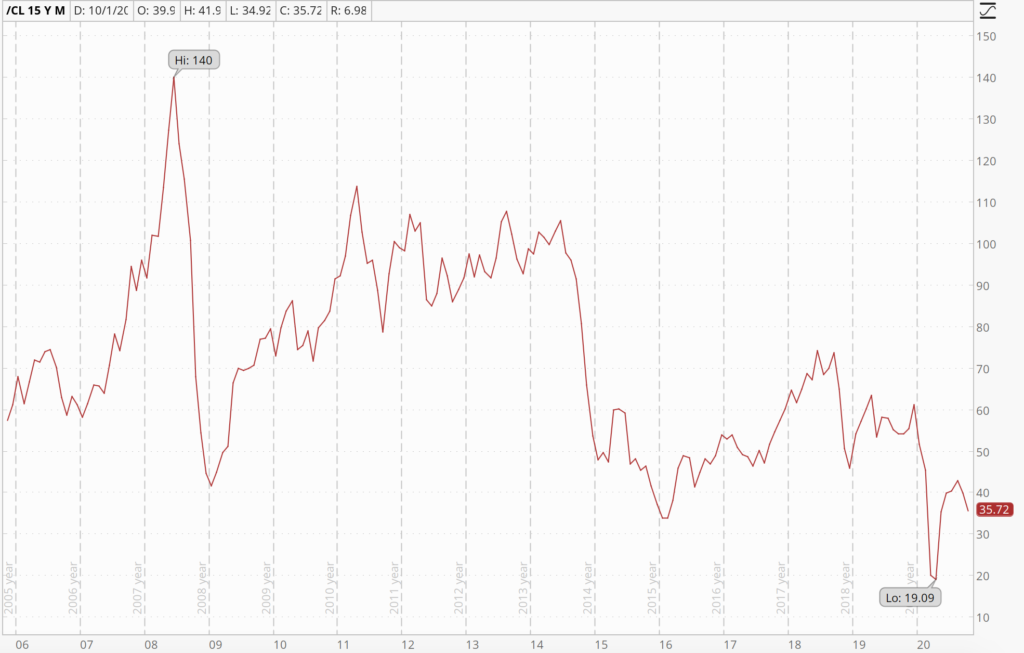

The fact of the matter they aren’t dying. The demand for oil and gas is increasing. You might not guess that from the price of oil and natural gas.

Natural Gas prices have cratered over the last 10 years Oil prices have also trended down from the 2007 high of 140

The reason for these price declines is because the supply of oil and gas is so robust. The reason I know that is because as prices are falling, consumption of oil and gas continues to increase. When supply increases faster than demand prices will fall.

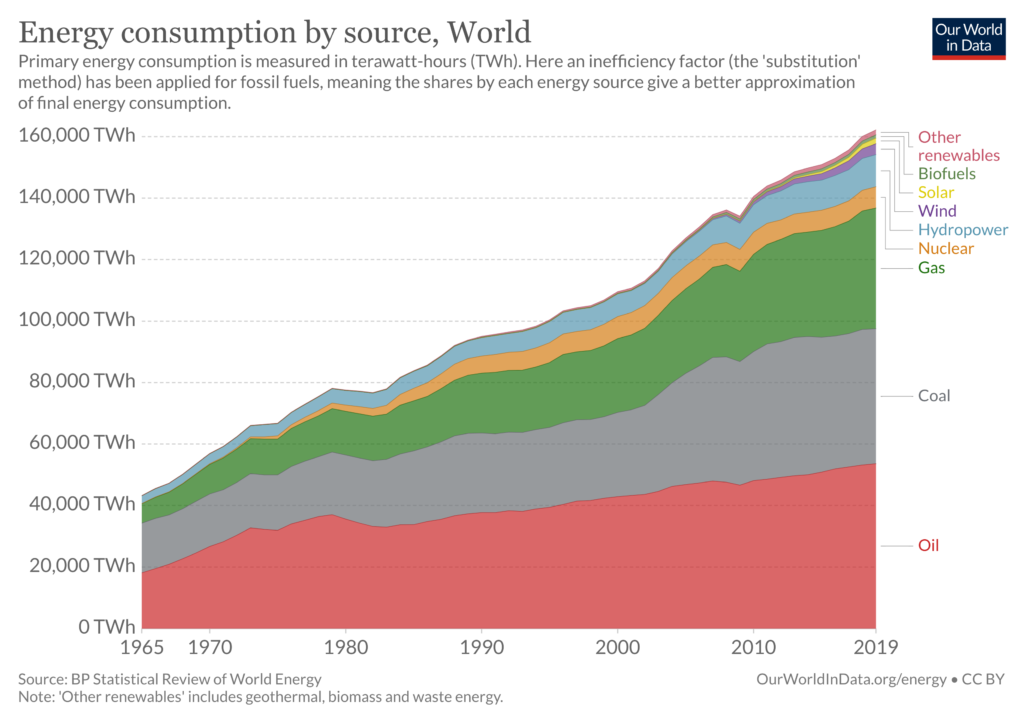

It is important thing to understand the world continues to consume more and more energy. 2009 was an exception to that rule and 2020 will be as well but the long term trends over the past 10 years and going back as far as I have data is that energy consumption keeps going up. Oil and gas consumption keeps going up as well on an absolute basis.

But the lockdown induced economic slowdown of 2020 will not last forever. Eventually the world will learn to live with the virus and the demand for energy will continue the long term trend of growth.

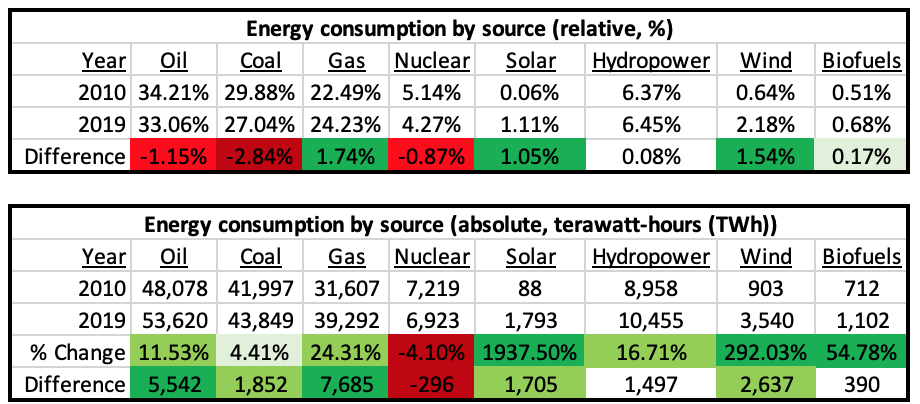

So what technology will be used to meet that demand? The trend has been an increase in energy coming from solar and wind. But they remain niche players on the global scene. As of 2019 Solar accounts for 1.11% of global energy consumption and wind accounts for 2.18%. These small industries have indeed been growing dramatically. The amount of terawatt-hours (TWh) of energy provided by solar went up 1,937.5% and wind went up by 292%.

On an absolute basis since 2010 the largest source of growth has actually been natural gas. Gas also had the largest increase on a relative basis, growing from 22.49% of energy consumption to 24.23%. However, coal and oil still remain the largest sources of energy and while they are shrinking on a relative basis they are both still growing on an absolute basis.

Date Source: https://ourworldindata.org/grapher/energy-consumption-by-source-and-region?stackMode=absolute&time=earliest..latest

The biggest loser since 2010 has actually been nuclear power. Nuclear has declined on both an absolute and relative basis. Nuclear provided 5.14% of global energy as of 2010 and has dropped down to 4.27%. On an absolute basis it has dropped from providing 7,219 TWh of energy and as of 2019 is down to 6,923 TWh. But even though nuclear energy consumption is declining, nuclear still provides more energy than solar and wind combined.

I think these trends will continue over the next 10 years. Solar and wind will continue to grow on a relative and absolute basis. But I think the relative growth they pick up will largely be from coal and perhaps in small part from nuclear unless the attitude towards nuclear technology changes. I believe natural gas will continue to grow on a relative and absolute basis. I further believe oil will continue to increase on an absolute basis but may stay relatively flat to downward on a relative basis. Coal will continue to decline on a relative basis and might even start to decline on an absolute basis as well.

Wind and solar are definitely in more of a growth mode, as you can see from those huge numbers, than the oil industry. But gas is also in growth mode. I do like alternative energy companies like Next Era Energy (NEE). While NEE is in the wind and solar space they also provide power using natural gas and nuclear. I’m looking for a buying opportunity and looking for value in the alternative energy sector as well.

But that doesn’t change the fact that oil and gas stocks are trading at steep discounts and oil and gas consumption is still in an uptrend. As billion hypocrite Warren Buffet once said be “fearful when others are greedy, and greedy when others are fearful.”

There is a lot of fear in the oil and gas industry so it might be time to be greedy.

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.