by John | Mar 24, 2018 | Preservation of Purchasing Power, Wealth Protection

The United States is in a negative interest rate environment. Bank accounts essentially pay zero interest but price inflation is at a minimum 2.2%. That is if you believe the CPI.

Source: https://www.bls.gov/news.release/cpi.t05.htm

I don’t know what the actual rate of price inflation is, however, I think it is rather closer to 5% than 2.2%.

If the CPI were calculated the same way it was in 1990 it would be 6%.

Source: http://www.shadowstats.com/

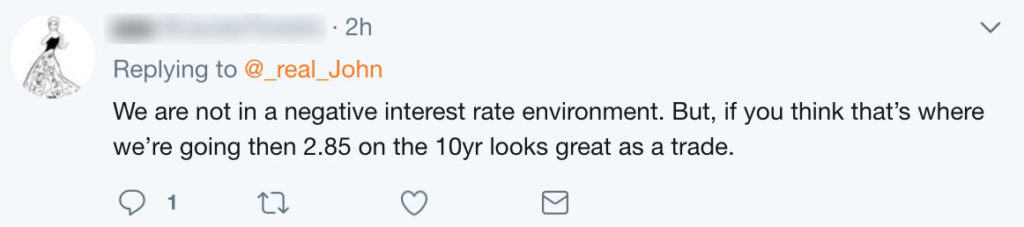

I like to save tweets like this for posterity

The tweetist above is wrong about us not being in a negative interest rate environment. Are nominal interest rates negative? Basic math tells us of course not.

Are real interest rates negative? Definitely. Real interest rates are what matter. If the rate of inflation is greater than the rate of interest paid then real interest rates are negative. This is the situation we find ourselves in.

While we are already in a negative real interest rate environment I do think there is a good chance that we will see overtly negative interest rates in the future in the US. If the Federal Reserve starts buying bonds again, the price of bonds in dollar terms will go up and yields will drop, as anyone who knows anything about bonds knows.

However, bonds are paid in dollars and if the Fed were to restart Quantitative Easing what would that eventually do to consumer prices? Would the market wake up and realize the Fed can never shrink it’s balance sheet? What would that do to the value of the dollars the bonds are claims on?

Buying the 10 year right now would be a winning trade in dollar terms if the Federal Reserve adopts negative interest rates but I think the dollar would tank.

The Fed is raising interest rates. So bond prices naturally fall as yields rise. Does it make sense to buy bonds in a tightening cycle? No.

And if you think everything is fine and you believe the CPI then you wouldn’t want to own bonds anyway since they pay a very small yield relative to the official rate of price inflation.

In my view treasuries are reward free risk and I see no point in owning them.

by John | Feb 26, 2018 | Asset Allocation, Capital Appreciation, Economic Outlook, Geopolitical Risk Protection, Liquidity, Preservation of Purchasing Power, The Economy, The Stock Market, Wealth Protection

Over the past few weeks I’ve been writing about the faulty wiring in the United States economy that will eventually result in an Economic Conflagration.

The faulty wiring that will ultimately lead to this economic firestorm includes the fact that the real economy is weak, the economy is crushed by profligate debt and that stocks are overpriced and due for a significant crash.

One of the reasons why candidates such as Bernie Sanders and Donald Trump were popular in the last United States presidential primary and general election is because people know that the real economy is weak. They know how much debt they have and they want someone to make radical changes and do something about it.

Unfortunately government has never been particularly good at creating wealth or prosperity.

Some people might choose to rely on politicians to fix things. This website is not for those people. HowIGrowMyWealth.com is for people who want to take some common sense steps to grow and protect their wealth.

Given the faulty wiring the economy it is more important than ever to grow and protect one’s wealth. It might take a while but this faulty wiring will eventually result in a fire that will burn uncontrollably.

I realize this isn’t necessarily very cheery stuff but fear not! There is plenty of room for optimism.

I’m not a doomsday “prepper” or perma-bear and I’m sure that entrepreneurs, if free to do so, will rebuild the economy and usher in greater prosperity that will not be funneled to the politically connected.

I’m also cognizant that the stock market has gone up nearly 300% since the great recession, there hasn’t been hyperinflation in consumer prices and on the surface the crisis seems to have passed long ago. I don’t have a crystal ball and being right early sometimes looks like being wrong.

Despite the relative calm there is faulty wiring in the economy and sooner or later it will spark and ignite blaze that will, to quote Peter Schiff, “will make the financial crisis of 2008 look like a Sunday school picnic.”

The politicians, if they even realize that there are systemic problems in the economy, simply aren’t willing to endure the short term pain and inconvenience of ripping out the faulty wiring in order to fix the underlying problems. So they will continue to kick the can until the economic house burns down.

The bright side is that this will present an opportunity to rebuild the economy based on a strong foundation as opposed to what we have now, a phony economy based on debt, cheap money and consumption.

There will be winner and losers. I’m very optimistic about the future and I want to be counted amongst the winners.

So where am I putting my money?

My asset allocation falls into three main areas. Value stocks, gold and cash.

Value Stocks

Most people love buying things on sale and getting a great deal, expect when it comes to investing. When it comes to investing people want to buy expensive things and hope they go higher. Value investing takes that same common sense, buying things when they’re on sale and applies it to stocks and other asset classes.

The stock market as a whole is overvalued by a variety of metrics. But there are still good deals out there especially in non-US markets. I don’t doubt that value stocks will also go down in the event of a stock market crash but I think they will go down less and they will recover with more strength.

I could write entire articles on value stocks and I have. I’ve written about the value investing metrics I use when evaluating a stock and I also have my own value stock picks based on these metrics.

I share my value stock picks publicly. But I only share if I would buy them today or if I would hold or add to my positions with members of my free email newsletter. I will also let me email subscribers know when I buy or sell a stock first, before I publish that information to this website.

Gold

I don’t think you will get rich buying gold but it could prevent you from getting poor. Under relatively normal circumstances the demand for gold is fairly steady and the supply is fairly steady so for the most part the price of gold will rise with the level of inflation.

Gold is a way to save purchasing power. It’s a way to opt out of the financial system and wait for sanity to return.

If the dollar tanks loses it’s reserve currency status gold will still be valued.

I also think there has been significant effort to suppress the price of gold and depending on how much downward price manipulation there really has been, the price of gold could go up significantly from where it is right now.

If fiat currencies collapse that could very well induce a flight to the safe haven asset of gold that this influx of demand would be very bullish for gold.

Because of the absurd expansion in central bank balance sheets and artificially low interest rates I like gold presents a fantastic value at current prices.

What I write about gold applies to silver–another asset I think will do very well in a downturn. Silver has the added benefit of being an industrial metal that is more widely consumed.

Cash

Long term, like every other fiat currency, I think the dollar will go to zero. So why would I want to hold dollars?

First, I own a month or two of expenses in physical cash in a secure location in case there are capital controls. If there is a panic and people start withdrawing money from the banks the banks might in turn say, you can only withdraw $500 a week or something like that. Withdrawal limits could also be imposed if the US implements negative interest rates and people (very rationally) decide it is better to hold dollars in physical cash so they don’t have to pay interest to their bank for the privilege of loaning their money to the bank.

I reside in the United States and everything is priced in dollars so I need dollars to buy things. If I lived in the eurozone I would hold pounds or euros, if I lived in China I would hold Yuan. If I lived in the socialist paradise of Venezuela I would probably hold dollars (and try to get out).

Secondly, apart from physical cash I also hold dollars in a money market fund as a war chest. If stocks tank I expect there will be bargains to be had. I want to be buying stocks (if they are high quality free cashflow producing companies) when everyone is panicking and selling.

Now I fully expect the United States Federal Reserve to do what it has done in all other crises it has created–it will lower interest rates and buy assets to prop up the markets.

With interest rates already low once they cut rates to zero they will only be able to do things like Quantitative Easing and Negative rates. This is very bearish for the dollar and very bullish for gold.

But in the highly unlikely chance the US Federal Reserve does the right thing and lets the stock market collapse and lets the US government default on it’s debts this could be very bullish for the dollar. So holding some dollars is a hedge against deflation as well as a war chest to draw upon to buy undervalued stocks post crash.

What are some other possibilities?

While the bulk of my holdings are in cash, value stocks and precious metals I also dabble in some other alternative investments.

Cryptocurrencies

I’ve been a skeptic of cryptocurrencies for many years. I’ve also owned them for many years.

If there is a dollar crisis or collapse in the faith of central bankers then more people could turn to cryptocurrencies and could see it rise. Demand for cryptocurrencies could also rise for other reasons pushing the price upwards.

While I think blockchain technology is here to stay the value of any one specific cryptocurrency or token could very easily tank to nothing. Cryptocurrencies are very risky and 90% swings (both directions) happen.

You need to have an iron stomach but having between 1-5% of your liquid net work in cryptocurrencies isn’t the most outlandish idea in the world.

I would only speculate on cryptocurrencies with what you can afford to lose and I don’t considering buying cryptocurrencies investing in a technical sense since I am simply betting on the price going up.

I’ve shared with my readers my Group of Six cryptocurrencies that I’ve chosen to own and speculate on.

Options

Net I’ve actually lost money trading options. I traded options while unemployed and failed to remain dispassionate and objective. I was so focused on making money that I opened positions when the conditions were not ideal and took risks I should not have been taking.

I do believe if you are disciplined and follow the appropriate rules, you can do well trading options.

During a stock market crash volatility spikes and selling options could be a good strategy. When the VIX (a volatility index) spiked up in early February I sold a few options and those positions are doing well as volatility has dropped and the market has recovered. Markets don’t move straight up or down for very long so even if the February selloff portends drops to come, the market doesn’t drop as fast as people think in the midst of the drop.

Real Estate

Unlike all the other assets mentioned above I do not and never have owned any real estate.

Lots of people have made lots of money in real estate. I am working to learn more about this asset class and hope to own my own rental property at some point.

What I like about real estate is that it is easy to use leverage and the tax benefits are ridiculous. You can effectively pay no tax on investment property income and borrow a lot of the money you need to get started.

You of course need to know what you’re doing.

My goals for owning real estate involve owning a multi-family apartment building. The key for me is a cashflow positive property. I don’t have any interest in trying to buy and flip, although some people are very successful doing this. There are lots of ways to make money in real estate and I recommend biggerpockets.com to learn about them.

I think cashflow positive real estate will do okay in the event of a crash. If you’re in an area that has stable employment prospects those workers will always need a place to live and have the money to pay for it. Of course real estate won’t “always go up” and there are a lot of risks and headaches associated with managing property (if you don’t outsource property management).

This is part 5 of 5 of what I’ve decided to term The Economic Conflagration series where I discuss the faulty wiring pervasive the global economy:

Part 1: A Deadly Electrical Fire you Need to Know About

Part 2: The Real Economy is Weak

Part 3: Crushing Debt in the United States Limits Economic Growth

Part 4: Stocks are Overpriced and Due for a Significant Crash

Part 5: Where to Put Money when the Stock Market is Overheated

by John | Jan 22, 2018 | Geopolitical Risk Protection, Preservation of Purchasing Power, Wealth Protection

The S&P 500 is currently in the longest period EVER without a 3% correction. The unemployment rate in the US is just 4%.

Source: http://money.cnn.com/2017/11/26/investing/stocks-week-ahead-sp-500/index.html

The S&P 500 is at all time highs–far surpassing the dot-com bubble and the housing bubble.

Is this the new normal? Is Federal Reserve Chair Janet Yellen right that we won’t see another crisis in her lifetime? Is there even a need for alternative investments when the stock market continues to soar?

Yes, now more than ever.

Faulty Wiring in the Economic House

Let’s say you live in an apartment building you’ve discovered has faulty wiring. You know there is a very good chance it will catch fire and burn to the ground.

Let’s say you live in an apartment building you’ve discovered has faulty wiring. You know there is a very good chance it will catch fire and burn to the ground.

Would you continue to go about your business and just hope the apartment building doesn’t burn down?

Or would you do something about it?

Unfortunately most people, if they even know about the risks, ignore them or simply choose not to do anything about them. When the fire starts they will get cooked.

But you don’t have to be one of those people

You can choose to do something about it

We can’t know exactly when but there are plenty of good reasons to believe the US economy is going to undergo an economic firestorm in the future.

Throughout US economy there is the financial equivalent to faulty wiring that will eventually cause an economic conflagration.

You can certainly point to more but here are three of the faulty wirings in the economy:

- The real economy is weak

- Debt at the Federal, State, and Personal levels are un-repayable

- Reckless Central Bank Actions have created a massive bubble in stock and bond markets

Despite all the doom and gloom there are plenty of things you can do to ensure you’re financially safe.

Do Something About It

The wiring in the building needs to be torn out, but landlords aren’t willing to go through the pain, cost and inconvenience of rewiring. All the while the problems get worse.

They’d much rather put on a new coat of paint and pretend like everything is fine.

But you can choose to position yourself so that when the building does burn down, you and your possessions won’t be incinerated.

Similarly, the powers that be in government are too entrenched and committed to maintaining the status quo as long as possible. They have continually demonstrated they are not going to take proactive steps to solve any of these economic problems (and after all they in large part the cause of the problems).

The government will only act when it has no other choice. In other words the government will only act once the crisis has hit and it is too late.

In the coming days I’ll be discussing these three categories of faulty economic wiring: a weak real economy, unrepayable debt and the stock and bond bubble.

Not only that I’ll be sharing actionable strategies through alternative investments to grow and protect your wealth.

It’s not about doom and gloom or prepping for the magnetic poles of the earth to reverse and cause gravity to invert.

It’s just about taking some practical steps in light of the very real and system risks present in the financial system.

by John | Jan 14, 2018 | Asset Allocation, Geopolitical Risk Protection, Preservation of Purchasing Power, Saving Money, Wealth Protection

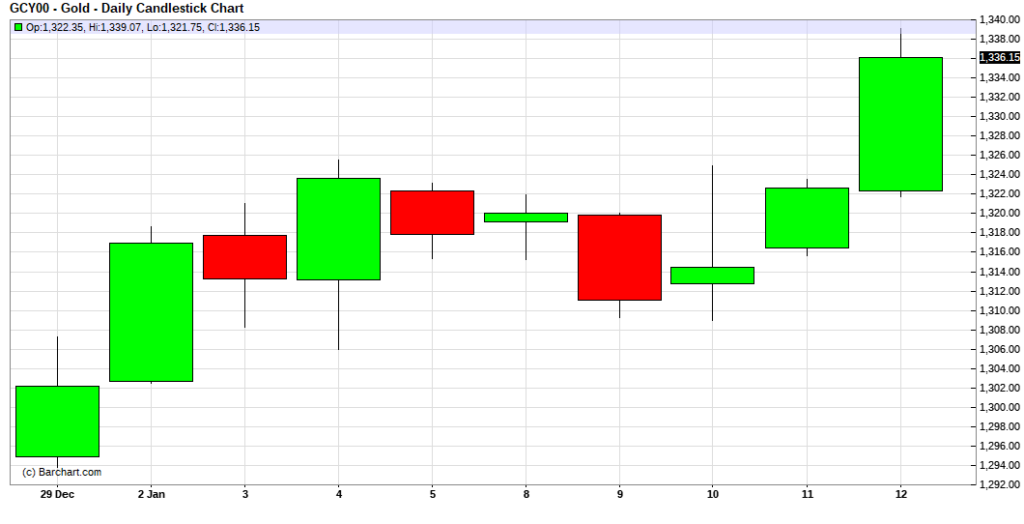

A 2.6% rise in the price of gold doesn’t seem like a lot given the tremendous volatility of cryptocurrencies like Bitcoin which can go up or down 30% in a day. Twenty eighteen has started off strong for the yellow metal. While gold has lost some if it’s shine in the eyes of many since the drop from it’s highs in 2011 it remains the standard in wealth preservation as far as I’m concerned. I am as bullish on gold today as I ever have been. Perhaps not in the medium term, but in the short and long term I think gold will be rising in USD price.

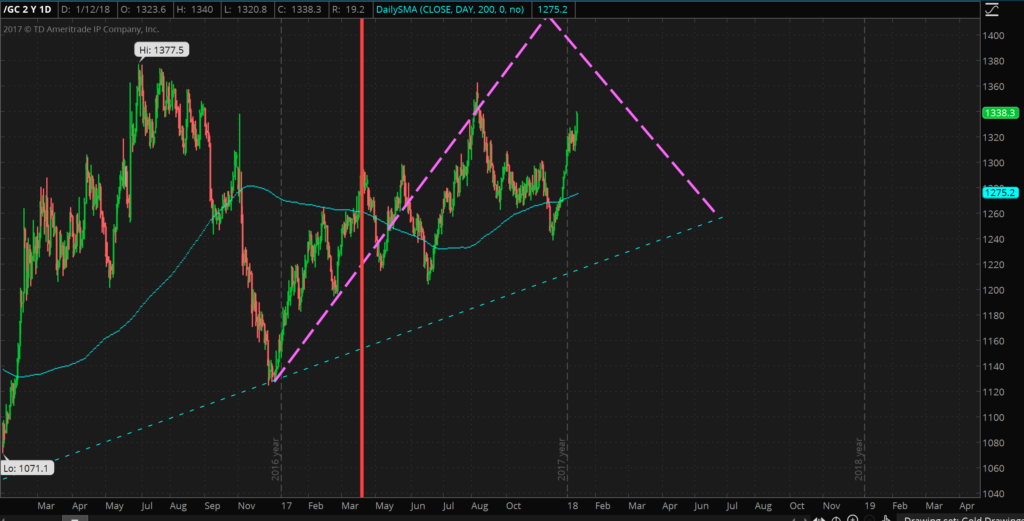

I posited back in April 2017 that 2016 was the start of a new bull market in gold and that trend has continued.

The dashed purple line indicates my prediction/guess as to the price movement of gold. This prediction was made back in the middle of April, 2017 (indicated by the vertical red line).

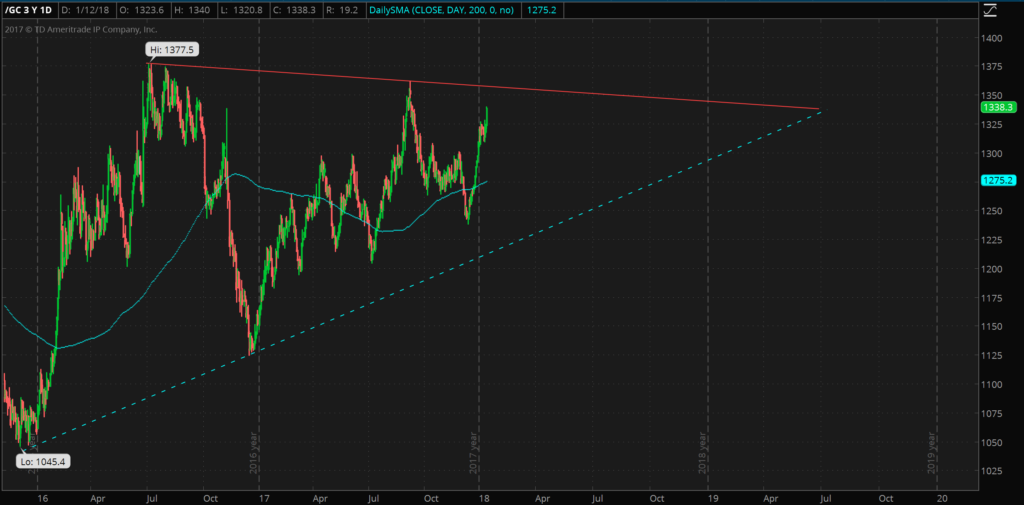

While this prediction looked fairly close up through August 2017, gold has since diverged quite a bit. Because gold hasn’t been able to take out the previous high of $1377.5 made back in July 2016, this bull market is looking fairly weak from a technical perspective, especially compared to the 2008-2011 bull market. This is why I think gold looks weak in the medium term (say 6 months to a year). In the short term gold is looking good, as previously mentioned gold is up over 2.5% this year.

But even if the technicals of gold look weak the fundamentals of gold are still extremely strong. I think there is little chance that we will see gold available at a price of 1045 USD ever again and I think gold will eventually make new highs in excess of $2,000. I do think gold is in a bull market, albeit a weak one. A US War with North Korea, a Trump impeachment, another large scale terrorist attack, or any number of other catalysts could easily send gold upwards.

While we might have to wait until 2019, it will be interesting to see if gold breaks through the resistance (solid red line) and if so if it makes a new high above 1377.5, or if it goes back to test the longer term support levels drawn in a dashed blue line. Of course it could even do both if we see a lot of volatility.

I feel confident that gold will be above $1300. Regardless I think holding between 10%-25% of one’s assets in physical precious metals is a wise move. Go closer to 10% if you have faith in the US.gov and legacy financial system and closer towards 25% if you are a little more bearish on the US governments ability to handle the national debt, pension, social security and medicare funding crises. Of course all of these precious metal allocation percentages are just opinions and don’t take into account your age, goals and risk tolerance. If I had a lot of money in cashflow positive real estate or a successful and recession resistant business then I probably wouldn’t put as much into gold.

But if my income came from stocks and my job I would want to have 10-25% of my assets in precious metals and I would want to have some money in foreign stocks. I don’t think betting on the dollar is wise, it hasn’t been since 1913 and I think the dollar will only continue to weaken and at an accelerated pace.

While there is no substitute for physical precious metals like gold and silver held in a secure location one controls I think Goldmoney is a fast, easy and secure way to own physical precious metals. When you sign up for a Goldmoney holding account be sure to use my referral code: howigrowmywealth. A Goldmoney holding account allows you to store physical gold throughout the world in secure jurisdictions like Singapore and Switzerland. I personally own over $1,000 worth of gold through Goldmoney.

by John | Oct 28, 2017 | Preservation of Purchasing Power, Wealth Protection

The other day I was watching an excellent and classic Japanese film: The Hidden Fortress. This picture stars the inimitable Toshiro Mifune and is directed by Akira Kurosawa. It is about a defeated Samurai clan attempting to smuggle gold across enemy territory to restore the clan’s domain.

I also recently read a Clive Cussler novel: Inca Gold, a mildly diverting story which mixes historical events with legend and fiction. Inca Gold is about a race to discover a hidden cache of gold in South America. While both works are obviously fiction they serve as a reminder of the historical fact that gold has been valued across cultures and across time. One might even say gold is timeless.

Here are a few examples of gold in cultures throughout the world.

A 6,000 year old Gold Pendant

A gold pendant crafted over 6,000 years ago. Photo: via The Daily Mail

The oldest known gold treasure trove is in a Necropolis (burial site, literally “city of the dead”) near the city of Varna in what is now Bulgaria where thousands of gold pieces have been discovered.

One item in the hoard includes a 2 gram 24 karat gold pendant was found thought to date back to 4,300 BC. It is the oldest known gold jewelry.

Other Varna Necropolis gold includes necklaces, bracelets, earrings, a tiara and a gold hammer-scepter.

Source: http://archaeologyinbulgaria.com/2015/10/15/bulgaria-showcases-worlds-oldest-gold-varna-chalcolithic-necropolis-treasure-in-european-parliament-in-brussels/

Each of these bracelets weights upwards of 110 grams. These timeless bracelets look like they could have been forged yesterday. (Varna Regional Museum of History)

Source: https://www.smithsonianmag.com/travel/varna-bulgaria-gold-graves-social-hierarchy-prehistoric-archaelogy-smithsonian-journeys-travel-quarterly-180958733/

The Varna Necropolis was rediscovered in 1972. Only about 30% of the site has been excavated. Although I wonder that it might be better to leave the graves, the remains, and the artifacts undisturbed.

Source: http://archaeologyinbulgaria.com/2015/11/20/bulgarias-varna-to-make-site-of-worlds-oldest-gold-varna-chalcolithic-necropolis-accessible-for-tourists/

The 3,300 year Old Gold Death Mask of Tutankhamun

Golden Mask of Tutankhamun in the Egyptian Museum

Tutankhamun was an Egyptian Pharoh (colloquially referred to as “King Tut”). He is famous because his tomb, located in the Valley of the Kings, was found largely intact in 1922. It had been robbed twice in antiquity and resealed. But despite this his tomb is still one of the greatest archaeological finds. The tomb of Tutankhamun contained a veritable trove of artifacts including the iconic solid gold funerary mask pictured to the left.

Source: https://en.wikipedia.org/wiki/KV62

Some of the Egyptian pyramidia were said to have been coated in gold leaf or electrum.

Source: https://en.wikipedia.org/wiki/Pyramidion

Earliest known Gold Coins over 2,500 years old

Early 6th century BC Lydian electrum coin weighing about 4.7 grams

According to greek historian Herodotus the Lydians (a people located in modern day Turkey) were the first to use gold and silver coins somewhere between 700 BC and 550 BC.

At least some of these coins were made from a naturally occurring alloy of gold and silver called electrum and stamped with a lion’s head.

Source: https://en.wikipedia.org/wiki/Lydia#First_coinage

Roman Gold Coins dating back 2,050 years

Aureus of Octavian, c. 30 BC.

The roman aureus dates back to the first century BC. Although minted prior to Julius Caesar, Caesar standardized the aureus at a weight of approximately 8 grams of 99% pure gold.

But the history of the aureus, like virtually all government issued money, is one of devaluation.

By the reign of Constantine Solidus, the aureus contained just 4.55 grams of gold.

The latin word for gold is aurum and is the genesis of the periodic table symbol of gold: Au. A derivative of the aurum can also be found in the first name of gold-loving James Bond villain Auric Goldfinger.

Source: https://en.wikipedia.org/wiki/Aureus

Inca and Pre-Columbian Gold

The Inca Empire had considerable gold and silver. However, between 1532-1572 Spanish conquistadors systematically plundered, stole and extorted this wealth as they destroyed the Inca Empire. The cups, necklaces and other gold items crafted by the Incas was melted down, cast into bars and shipped back to Spain.

Inca Gold Cup, Picture from National Geographic

A large trove of Inca gold does remain, at least in a legend. Like many others the legend of the lost Inca gold begins in historical fact.

In 1533 the war of succession between two Inca princes had ended. The younger prince Atahualpa defeated his half-brother Huáscar to become Sapa Inca (emperor). Emperor Atahualpa met with Spanish conquistador Francisco Pizarro. Despite being vastly outnumbered Pizarro and his 150 some troops were able to capture the Inca ruler.

Commander Pizarro agreed to release Atahualpa in return for a roomful of gold. This gold was indeed delivered, but Pizarro reneged on the deal and after a show trial had Atahualpa garroted. At this point the line between history and legend blurs.

Legend purports Pizarro had the Inca leader put to death before the last and largest part of the ransom had been delivered. Upon learning their Emperor was killed, the Incas buried the remaining gold in a secret mountain cave. This cave has never been discovered.

Source: https://en.wikipedia.org/wiki/Spanish_conquest_of_the_Inca_Empire

Source: https://www.nationalgeographic.com/archaeology-and-history/archaeology/lost-inca-gold/

Chavín Gold Crown 1200-300 BC

There were of course many other pre-Columbian civilizations apart from the Incas. One is the Chavín culture–an extinct civilization that was located in what is now the northern Andean highlands of Peru. Their achievements included advances in metallurgy, as evidenced by the gold crown shown to the right which could be over 3,000 years old.

Source: https://en.wikipedia.org/wiki/Chav%C3%ADn_culture

Gold Coins of Feudal Japan

The koban (小判) was a Japanese oval gold coin in Edo period (1603–1868) feudal Japan. Shown here is the Keichō-period koban containing 16.5 grams of gold.

Shogun Tokugawa Ieyasu established a metallic monetary system in 1601 which would last until 1867.

Source: https://en.wikipedia.org/wiki/Tokugawa_coinage

One of the units in the Tokugawa monetary system was the koban (小判) which means oval. When first introduced it contained 1 ryō of gold or about 16.5 grams and was considered to be a rough equivalent to four koku (石) of rice.

Source: https://en.wikipedia.org/wiki/Ry%C5%8D

One koku of rice was originally defined as the amount of rice needed to feed one person for one year. This original definition of a koku of rice would weigh about 150 kilograms (330 pounds). Thus one koban would be worth around 4 years of sustenance.

Source: https://en.wikipedia.org/wiki/Koku

Although in reality the amount of rice that could be obtained, even with a Keichō-period koban certainly would have fluctuated based on the size of the rice harvest, demand and various other factors, it still serves as an insight into the value of the koban when first introduced.

Like all nearly all governmental systems of money, it was steadily devalued as shown visually with the decreasing size of the koban over the years.

Koban debasement

Gold is Timeless

Gold has been valued across the ages and across cultures. In the spirit of modern hubris commentators have declared gold a barbarous relic and a pet rock. Some folks might concede that gold was once useful, but now that we have computers and electricity and bitcoin we don’t need gold. It takes a unique pride or perhaps outright ignorance to make such a pronouncement about an element that has been valued for millennia.

by John | Aug 30, 2017 | Capital Appreciation, Currencies, Geopolitical Risk Protection, Preservation of Purchasing Power

Whatever vestigial link between US dollars and gold ended after Bretton Woods was terminated on 15 August 1971. The classic gold standard was abolished long before in 1933 when the despotic executive order of United States President Franklin D. Roosevelt that made it illegal for citizens in the land of the free to own gold.

There are periodic calls to return to a gold standard as a way to reign in government spending. The return to a pre-1933 gold standard would be a huge step in the right direction.

A true gold standard uses gold as money. A true gold standard in the US would redefine dollars as a quantity of gold. A true gold standard is NOT saying that gold is worth $35 per ounce as was the case in Bretton Woods.

This is explained in fantastic detail by Mises Institute Senior Fellow Joseph T. Salerno in his lecture Gold Standards: True and False.

A Return to the Gold Standard in the US?

It sounds click-baity to me too, but Jim Rickards is predicting $10,000 gold as the result of a currency reboot. The link above is to a sales page (which I get zero benefit from and considered not linking to) that explains in his own words why Rickards thinks Trump will return the US to a “gold standard”.

James G. Rickards is a New York Times bestselling author who appears on networks like RT, CNBC and Bloomberg. He’s testified in front of congress, he’s done some consulting on currency for the CIA and Pentagon. So there are some reasons to listen to what he says and at least evaluate his rationale and his arguments.

If I can quickly summarize his argument it’s that the US is deeply in debt, debt has crushed the middle class, a gold standard is one of the keys to “Making America Great Again” and so President Trump going to move the US back onto a gold standard. Rickards also claims he has some inside information that gives him additional reason to believe a return to such a gold standard is likely.

I agree the US is deeply in debt. I also agree the economy is broken and stacked against the middle class in favor of the super-wealthy. I also agree that a return to a classic gold standard similar to what existed pre-1933 would help America.

There is also some evidence that Trump is receptive to the gold standard.

Would Trump Support a Gold Standard?

Trump has stated to GQ: “Bringing back the gold standard would be very hard to do, but boy would it be wonderful. We’d have a standard on which to base our money.” In the same montage of questions he also stated that Justin Bieber shouldn’t be deported and that he’s not a fan of Man Buns.

Trump has also tweeted this:

Although “gold” here could simply mean wealth.

As far as I can tell Donald Trump is not a systematic thinker. He doesn’t have a set of principles with which he evaluates problems and situations. I think Trump’s “philosophy” is basically “I’m a smart guy with good business sense. So I’m going to use my gut and my experience to make ad hoc judgments about what to do.”

Although he probably wouldn’t use the term ad hoc.

So could Trump be in favor of a gold standard? Who knows? Even if he was in some way at some point in the past who knows what he would decide today. Just look at his 180 turn on the war in Afghanistan as one example of his fickleness.

Where does Rickards get $10,000?

Rickards uses a fairly basic calculation based on what he thinks the world money supply will be, how much gold there is and a 40% backing to get $10,000 gold.

Rickards writes that the US government would keep the price at this level by simply conducting some “open market operations” in gold:

The Federal Reserve will be a gold buyer if the price hits $9,950 per ounce or less and a gold seller if the price hits $10,050 per ounce or higher

And this is really the rub. Such a price peg is not a return to a true gold standard. It would not change the US government’s fiat monetary system in any meaningful way.

Dollar to Gold Price Pegs are not a True Gold Standard

The plan Rickards describes is essentially the same as a bill that was proposed in 2013. Mises Institute fellow Joseph T. Salerno explains how such a fake gold standard would not help at all. A true gold standard defines dollars (or other currency) as a certain weight of gold. For example, the definition of a dollar used to be 1/20th of an ounce of gold (roughly). A $20 bill was not the money per se but a claim to one ounce of gold.

The “gold standard” Rickards speaks of is simply fixing the price of gold in dollars.

I Would Like Gold at $10,000

All else equal I would like gold at $10,000. Sure, if I wanted to add to my holdings it would be cost prohibitive, but since I already own some gold a price increase to $10,000 via Federal Reserve open market operations would be of benefit to me.

However, if the dollar collapsed and a loaf of bread costs $10,000 I’m probably not better off. After all no sane person would want to be a millionaire in Zimbabwean dollars in 2008.

This fake gold standard Rickards is predicting certainly wouldn’t help the US economy at large. As I mentioned above, it would not be any significant change to the fiat monetary system. A price peg of gold in terms of dollars is NOT a gold standard. If anything I think it would be horrible optics for the US government and shake the world’s confidence in the dollar. It would effectively be a revaluation down of the dollar, at least relative to gold, and the Fed’s balance would very likely have to massively expand in order to bid gold up to $10,000.

A Return to the Gold Standard Seems Unlikely

A return of the United States to a true gold standard seems very unlikely. A fake gold standard as described by Rickards is more likely than a return to a true gold standard–but still a long shot. I do believe gold is a fantastic long term investment but I also believe it will take the market waking up to the problems of the global financial system and not an act of government.