Just about four years ago I wrote the first article on HowIGrowMyWealth.com “Inflation Destroys Dollars“. I wrote about how what I do to protect against price inflation and dollar devaluation. Specifically value investing and precious metals. So in retrospect, how did those investments do?

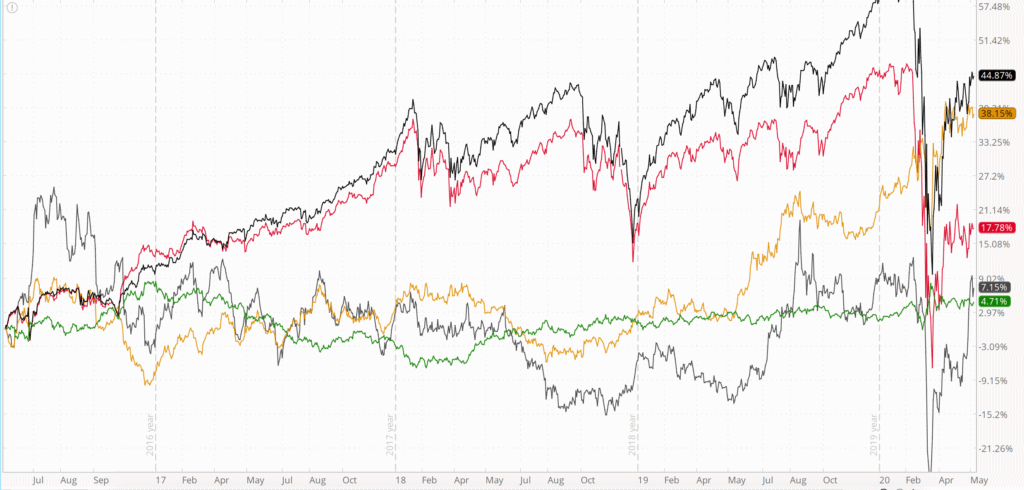

As a control we’ll add the U.S. Dollar Index ($DXY, shown in green), which compares the dollar’s strength against a basket of other currencies. To represents “stocks” I’d added the S&P 500 Index (SPX) (shown in black).

I’m using the Vanguard Large Cap Value ETF (VTV) as a proxy for value stocks (shown in red). You can see how my current and past individual value stock picks have done here. Gold futures are in yellow and silver futures in gray.

As you can see the S&P 500 has been the place to be. To be fair gold isn’t too far behind. Gold was in fact keeping pace with and surpassing S&P 500 this past April. So while gold has been a good hedge and having exposure to stocks has continue to be important.

Value stocks have lagged the S&P 500, particularly in the aftermath of the December 2018 selloff.

Silver is only slightly outpacing the dollar index, up just 7.15%. Silver has had a few failed breakout attempts, but continues to underperform. The gold/silver ratio that some precious metal bugs talk about would suggest that silver is a better value right now.

Costs continue to rise each year as the dollar loses value. But as measured by the DXY the dollar has kept its value against other currencies.

As I wrote back in November of 2016 in “I Own Too Much Gold“, you don’t want to own too much gold as a percentage of your net worth. The performance of the S&P 500 is a good reason why. If gold ever were to take off a 10-25% allocation would be more than sufficient.

We certainly haven’t see broad hyperinflation yet in the US, but my rent, food and medical costs continue to rise each year in excess of the government measured CPI. As I have for the past four years, gold and precious metals remains an important (albeit minority) portion of one’s portfolio.

If you are just starting to buy precious metals emphasizing silver over gold (while still buying both) could be a good approach.

The Coronavirus (COVID-19) outbreak has tanked stocks. The S&P 500 is down 13.6% into correction territory, falling from the high of 3,397.5 down to 2,931 as of writing this article. Other major indices have fared similarly.

What we Know about the Coronavirus

“As of March 6, 98,134 people have been confirmed to have COVID-19 (also known as the Wuhan coronavirus)…There have been 3,388 fatalities. “

As is often the case, the COVID-19 virus seems to impact the elderly more severely. As of 11 Feb, in mainland China, no deaths occurred in those age 9 or younger. The fatality rate was estimated to be higher among those age 70 and older.

By comparison, in the 1918 “Spanish Flu” epidemic the case fatality rate was estimated to be 2-3%.

I think it is valuable to keep this in perspective by comparing it the the standard influenza virus or “flu”. So far in the 2019-2020 flu season in the United States, there have been between 32 to 45 million flu illnesses and 18,000-46,000 flu deaths. By my calculation this would be a case fatality rate between 0.04%-0.14%.

The case-fatality rate is the number of confirmed cases divided by the number of confirmed deaths.

Of course there will likely be many more people who have or had COVID-19 that were never confirmed cases. A healthy person with flu-like symptoms might never go to the doctor and get tested and recover on their own. It is also possible there are people who have had COVID-19 that never showed symptoms and they would not count towards the number of people who have been infected.

In my opinion the number of confirmed deaths of Coronavirus is likely to be more accurate than the number of people infected. If someone dies of flu-like symptoms they were probably hospitalized before they died and were tested.

The point is there are a lot of unknowns. The stock market doesn’t like unknowns. At this point we don’t know if COVID-19 will become an epidemic or not.

What this Means for Your Wealth

I confirm from personal experience that making financial (or any other decisions) from a position of fear, panic or anxiety will almost never result in a good outcome.

While it can be easy to invest heavily in stocks or other higher risk assets when times are good, a 13% correction is a good reminder of the importance of diversification into a variety of non-correlated asset classes.

Even though gold has under performed stocks since the 2008-2009 financial crisis, the yellow metal has done well in the face of the Coronavirus panic.

Psychologically I think it is easier to keep calm and not panic when some assets are going up, as opposed to when all your holdings are dropping in value.

I have actually been underweight US stocks, missing out on some gains over the past 10 years, and will attempt to use this selloff to carefully and slowly build more equity exposure, cognoscente that stocks could always fall lower, particularly as the US enters election season and the uncertainly and volatility that could produce.

While I think that gold probably will go higher, with it trading at a six plus year high, it could be a good time for some profit taking for those over-allocated.

Gold reclaimed the $1,500 level just a couple months ago over Christmas. Now the yellow metal has topped $1,600 and is trading north of $1,610. Gold also reached this level earlier this year on January 8. However, long term Gold has not been at this level since March of 2013.

With a US stock market that is 11 years in a bull market, profligate government spending, artificially low interest rates and geopolitical uncertainty in Iran and China, gold will likely remain a safe haven place to park capital.

However, for those over allocated gold, this is also an opportunity for some profit taking.

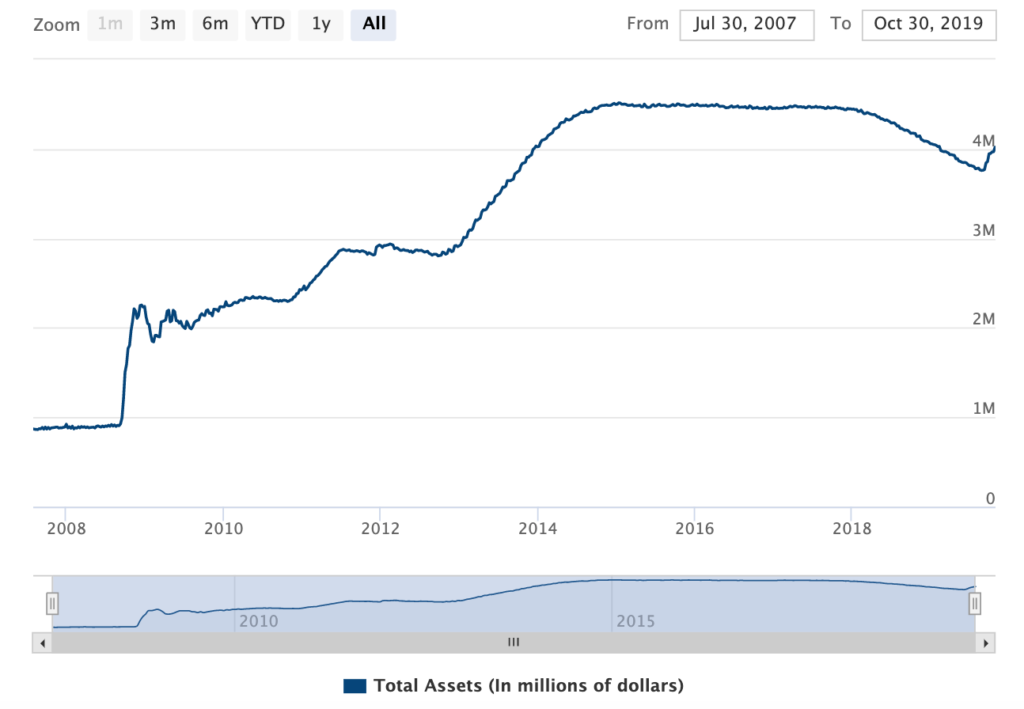

The Federal Reserve Balance sheet is back above $4 trillion for the first time since February of 2019.

This is more evidence that the US Government will monetize the national debt.

Monetizing the debt is when the government conjures money out of thin air “expanding the money supply” (in what amounts to legal counterfeiting) in order to pay the money it owes.

Monetizing the debt this puts downward pressure on the value of dollars and hence makes everything more expensive in what is described as price inflation, all else equal.

Is the Fed Monetizing the Debt?

The Federal Reserve has indicated that it would not monetize government debt.

“The Federal Reserve will not monetize the debt.” – Fed Chair Ben Bernanke

The reasoning goes that because they intend to shrink their balance sheet they aren’t just conjuring money created out of thin air.

But this is dependent on balance sheet normalization. Indeed, starting under Fed Chair Janet Yellen and accelerating under Fed Chair Jerome Powell the balance sheet had been trending down from the January 2015 high–at least until August 2015.

But as of 28 October 2019 the Fed’s balance sheet is back above $4 trillion. As humans we tend to place greater significance on large whole numbers when in fact there is nothing special about $4 trillion. But the point is that the Federal Reserve balance sheet began to tick back up starting in September of 2019.

Was the balance sheet declining from $4.5 trillion in January of 2015 down to $3.7 trillion in August of 2015 the extent of the “normalization” process?

The S&P 500 is making all time highs, everything is supposed to be wonderful in the economy, and yet starting back in September the Fed’s balance sheet is growing again, quite rapidly in fact as evidenced by the steepness of the chart.

How can the Fed ever normalize if they can’t do it after 10 years of stock market growth?

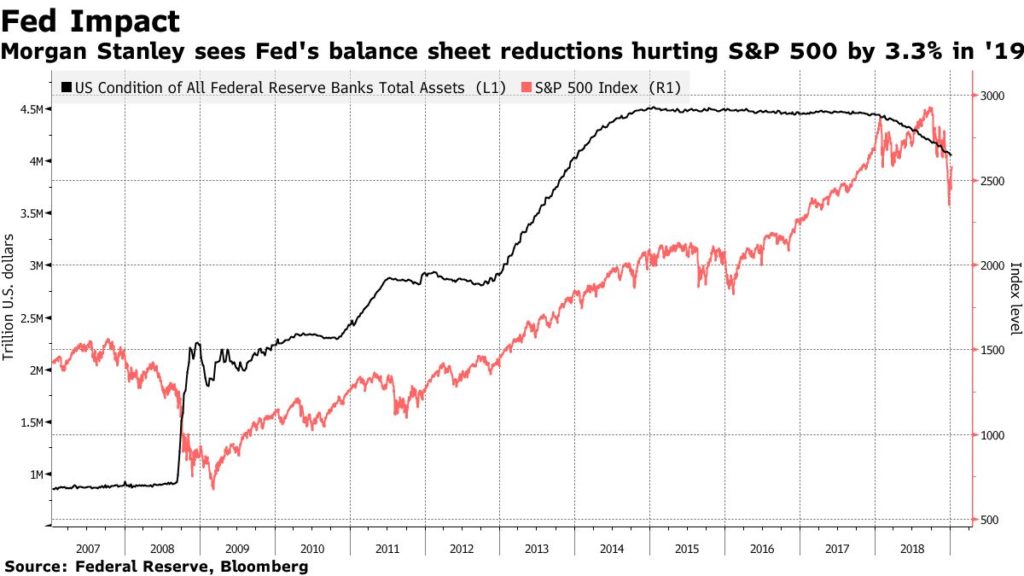

The above chart only goes through 2018. But it does show that the Fed’s balance sheet is correlated with the S&P 500. Despite the balance sheet tapering off slightly from 2016 onward through mid 2018 the S&P 500 continued to grow, until it sold off rather significantly in December.

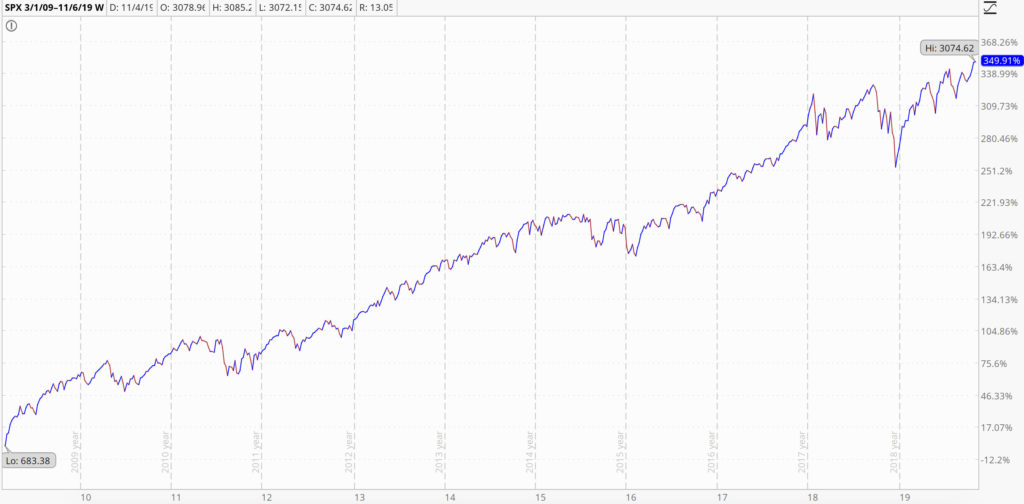

Since December the S&P 500 has rallied back and achieved new highs. All told, the S&P 500 has gone up nearly 350% since the March 2009 lows.

An intrepid investor who purchased the S&P 500 in the dark days of March 2009 would have done very well. However, I believe this artificial “growth” is really a bubble blown by the Federal Reserve.

If this “growth” has been fueled by the Fed’s monetary policy, then the Fed can’t even normalize without also tanking the markets.

Combine this with trillion dollar annual budget deficits and $23 trillion in national debt, the US simply doesn’t have any ammunition to fight the next economic downturn, at least not without seriously compromising the value of the dollar.

Source: https://usdebtclock.org/

US stocks have been the investment strategy for the past ten years. But this is the longest period of economic expansion in the history of the United States.

The uninitiated often think of the United States as a free market economy. It is in some specific ways but it is a far cry from a laissez-faire free market system. The main reason why the United States isn’t a free market is because of the Federal Reserve System, which controls money and how much it is worth. Money which is on one side of every single transaction that occurs in the economy.

Another reason the United States is not a free market is because of the myriad of taxes, rules and regulations prescribing how virtually all aspects of economic activity must be conducted.

Conventional foolishness states that deregulation causes the 2008-2009 financial crisis. However there were 115 agencies regulating the U.S. financial sector. As Tom Woods says, “Your friends think things would improve if there were 116.”

Monday the 28th of October was another example of how distant the US stock market is from a free-market and how the US economy is very much controlled, manipulated and centrally planned. Trump primed the trading algorithms this morning by stating he, “Expects A Good Day In Market Today”.

The S&P 500 then opened at a new all-time record high as a result. Meanwhile the Federal Reserve, the biggest currency manipulator in the history of the world, is expected to cut rates from an extremely low 1.75-2% to an even more extremely low 1.5-1.75%.

A free market economy is not driven to all time highs by the words of one man or a small group of bankers.

But a larger question remains: if everything is so great, why the rate cuts and “This is not QE” Quantitative Easing?

One factor driving the market is the trade war. When China and the US talk and say nice things to each other the market rallies. When they say mean things or refuse to talk the market sells off. The Federal Reserve is perhaps trying to give some support to the markets when China and the US seem like they can’t play nice.

But I believe the main reason is because the market is expecting it. The Fed isn’t data dependent. The Fed is market dependent. The odds of a rate cut are really just a voting machine to tell the Fed what to do.

I’m sure it doesn’t help the US Fed to be “independent” when Trump pounds on the oval office desk demanding more rate cuts and QE. The irony is that Trump is now just as guilty as Clinton, Bush, and Obama in blowing a big, “fat, ugly bubble.” Trump, if reelected, will be lucky if he can pull an Obama and exist stage left before it blows up during his tenure.

If the US were a free market interest rates wouldn’t be set by a small cabal of unelected, semi-private, pseudo-governmental bankers. It would be set by the supply and demand of lenders and borrowers.

The central banks, who artificially lower interest rates and inflate asset bubbles, fuel greed and cause recessions and crashes. Meanwhile, free markets get blamed and the plutocrats call for more regulations that simply reduce competition from smaller players who can’t afford an army of attorneys to both comply with the new rules and look for and find the loopholes. Regulations also raise costs for consumers.

Meanwhile the regulations wouldn’t have prevented the crisis anyway.

This can’t end well but who knows when it will end.

I previously wrote an article, “I Own Too Much Gold” and I’ve gotten several replies on twitter such as, “Impossible” and “No Such Thing”.

I strongly suspect (although I can’t prove it) these folks didn’t read the article. But in case they did and still aren’t convinced here are five reasons why you don’t want to own too much gold as a percentage of your asset allocation:

Reason 1: Lack of Tax Benefits

In the US, gains on physical gold are taxed as ordinary income, which could be a lot higher for you than the capital gains rate.

Even if you were an uber-gold bull and thought it was going to $100,000 per ounce would you really want to pay all your taxes on those gains as ordinary income?

Why not invest in some gold mining stocks (which would certainly go up as well if gold skyrocketed) and pay the capital gains tax rate? Why not hold some of those gold mining stocks in a Roth IRA so you pay zero capital gains taxes?

Reason 2: Diversification

Sometimes less is more

It’s important to be diversified in non-correlated assets. If I owned no gold, it would be important to own some, as gold tends to be less correlated with stocks and bonds. However, for the same reasons why you don’t want to be all in one asset class, you don’t want have too much of your assets tied up in gold.

If all you own is gold you don’t own any silver! Some speculate that silver will go up in value even higher than gold. If that’s the case you’ll want to diversity your precious metal holdings into the gray metal as well.

Reason 3: Liquidity

If you’re like most people, you need to buy food, clothing, energy, and the staples of living. You want to have some money in a more liquid format so you can pay for these things. If all your money was in gold, how are you going to pay your taxes or buy food?

Reason 4: No Cash Flow

If you invest in a business or a rental property or a dividend paying stock, there is cash-flow. If you own shares of a company, that company has employees trying to grow the business and increase shareholder value. Gold doesn’t do anything of those things. This is okay, gold doesn’t need to do those things (which come with their own set of risks), but if all your money is in gold then you are by definition missing out on opportunities to invest in cash-flow producing assets.

Reason 5: Charity

Wealth is a good servant but a terrible master. Ultimately you can’t take your gold with you and one of the great perks of having extra money (or wealth) is giving it away to those in need!

Do you want to gift your gold to a charity and have them have to deal with selling it?

If you keep some money in local currency it is easier to donate to a good cause. My favorite charitable organization is Children of Hope and Faith they help feed, clothe and educate orphans in Tanzania. I know the founder and board members personally and I know they have very low overhead which means it is efficient and there is more money going to the kids who need it. You can’t get any better than that!

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish.AcceptRejectRead More

Cookie Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.